Auditing Chapter (1) First Part 2023

Auditing Chapter (1) First Part 2023

You might also like

- Question 1 - Expository EssayDocument3 pagesQuestion 1 - Expository EssayMahinNo ratings yet

- Auditing International Approach NotesDocument29 pagesAuditing International Approach NotesRayz100% (1)

- Arens Auditing16e SM 01Document14 pagesArens Auditing16e SM 01Ji RenNo ratings yet

- Factory Studio User GuideDocument218 pagesFactory Studio User GuideTulio Silva100% (1)

- Chapter - 1THE DEMAND FOR AUDIT AND OTHER ASSURANCE SERVICESDocument46 pagesChapter - 1THE DEMAND FOR AUDIT AND OTHER ASSURANCE SERVICESDina AlfawalNo ratings yet

- (Objective 1-1) : Ayu Safitri (1902113029) Auditing 1 Review Question CH 1, Page 18Document3 pages(Objective 1-1) : Ayu Safitri (1902113029) Auditing 1 Review Question CH 1, Page 18Ayu SafitriNo ratings yet

- Audit UNIT 1Document9 pagesAudit UNIT 1Nigussie BerhanuNo ratings yet

- Auditing: Module 1overview of Auditing and Pre-Engagement ActivitiesDocument22 pagesAuditing: Module 1overview of Auditing and Pre-Engagement ActivitiesElla Jane Buenaventura JimenezNo ratings yet

- 1 AuditDocument9 pages1 Auditahmed sheblNo ratings yet

- Chapter 03 - Answer PDFDocument8 pagesChapter 03 - Answer PDFjhienellNo ratings yet

- Sheet AnswerDocument8 pagesSheet Answeramir rabieNo ratings yet

- Auditing I CH I-3Document64 pagesAuditing I CH I-3mercyteshite5No ratings yet

- CH 1Document34 pagesCH 1Ram KumarNo ratings yet

- Auditing Theory Cabrera 2010 Chap 2Document8 pagesAuditing Theory Cabrera 2010 Chap 2Squishy potatoNo ratings yet

- Auditing Ch1 by MekaDocument7 pagesAuditing Ch1 by MekaEbsa AbdiNo ratings yet

- Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions ManualDocument16 pagesAuditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manualterrysmithnoejaxfwbz100% (14)

- Chapter 02 Overview of AuditingDocument26 pagesChapter 02 Overview of AuditingRichard de LeonNo ratings yet

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document12 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1WandaTifanyArantikaNo ratings yet

- Chap. 1Document2 pagesChap. 1Al Mo SaintNo ratings yet

- Chapter 1 - Assurance & Engagement (Audit Theory) 2010e - Ma. Elenita B. Cabrera - Chapter 02Document8 pagesChapter 1 - Assurance & Engagement (Audit Theory) 2010e - Ma. Elenita B. Cabrera - Chapter 02Pol AnduLanNo ratings yet

- DocumentDocument7 pagesDocumenttafadzwagutusaNo ratings yet

- Auditing Principle I - CH 1Document6 pagesAuditing Principle I - CH 1keyruebrahim44No ratings yet

- SB7e WYRNTK Ch01Document3 pagesSB7e WYRNTK Ch01Joey LinNo ratings yet

- Perform Auditing and ReportingDocument65 pagesPerform Auditing and ReportingMulugeta GebinoNo ratings yet

- Chapter 1-3 SumaaryDocument16 pagesChapter 1-3 SumaaryLovely Jane Raut CabiltoNo ratings yet

- Solution Manual For Auditing and Assurance Services 17th by ArensDocument15 pagesSolution Manual For Auditing and Assurance Services 17th by ArensMarsha Johnson100% (33)

- Matriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreDocument12 pagesMatriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreKen KiongNo ratings yet

- Auditing Principle 1 - ch1Document7 pagesAuditing Principle 1 - ch1Duguma BejigaNo ratings yet

- Audit Summary Chapter 1Document5 pagesAudit Summary Chapter 1saniastariNo ratings yet

- Unit 1: An Overview of AuditingDocument12 pagesUnit 1: An Overview of AuditingYonasNo ratings yet

- Comp. Lesson 7Document18 pagesComp. Lesson 7Ryan Prado AndayaNo ratings yet

- Auditing Principles and PracticesDocument58 pagesAuditing Principles and PracticeskainatNo ratings yet

- IPFM Chapter 1Document20 pagesIPFM Chapter 1Yitera SisayNo ratings yet

- The Demand For Audit and Other Assurance Services: Concept Checks P. 34Document15 pagesThe Demand For Audit and Other Assurance Services: Concept Checks P. 34hsingting yu100% (2)

- Chapter 1 The Demand For Audit and Other Assurance ServicesDocument40 pagesChapter 1 The Demand For Audit and Other Assurance ServicesSerina PangarifNo ratings yet

- Verifiable Form Criteria Quantifiable Information Subjective InformationDocument5 pagesVerifiable Form Criteria Quantifiable Information Subjective InformationAnonymous BwN1AVNo ratings yet

- Maseno Universit1Document9 pagesMaseno Universit1Simon MutuaNo ratings yet

- Tutorial 1Document16 pagesTutorial 1youssefasaadNo ratings yet

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document13 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1Audric AzfarNo ratings yet

- Adv. Aud All Class Short-1Document223 pagesAdv. Aud All Class Short-1Abraha Aregay100% (2)

- Full Download Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions ManualDocument36 pagesFull Download Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manualpickersgillvandapro100% (32)

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document13 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1Kristel Nuyda LobasNo ratings yet

- Solutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsDocument26 pagesSolutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsStefany Mie MosendeNo ratings yet

- Arens Auditing16e SM 01Document14 pagesArens Auditing16e SM 01Mohd KdNo ratings yet

- AUDITINGDocument13 pagesAUDITINGGrace AlolorNo ratings yet

- Chapter 1 NotesDocument8 pagesChapter 1 NotesmatthewNo ratings yet

- Chapter 1Document8 pagesChapter 1mostafakhaled333No ratings yet

- Dwnload Full Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manual PDFDocument36 pagesDwnload Full Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manual PDFbendvvduncan100% (21)

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document13 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1Monique CabreraNo ratings yet

- Audit Solution - Chapter 1Document13 pagesAudit Solution - Chapter 1Hoài NamNo ratings yet

- Chapter 7: Introduction To Financial Statement AuditDocument18 pagesChapter 7: Introduction To Financial Statement AuditkripsNo ratings yet

- IM-01 Overview of Audit and Other Assurance ServicesDocument7 pagesIM-01 Overview of Audit and Other Assurance Servicesharley_quinn11No ratings yet

- Principles of Auditing ZicaDocument431 pagesPrinciples of Auditing ZicaDixie CheeloNo ratings yet

- AUDMOD1 Overview of Auditing and Pre-EngagemeDocument26 pagesAUDMOD1 Overview of Auditing and Pre-EngagemeJohn Archie AntonioNo ratings yet

- Self - Test Answers - L1Document2 pagesSelf - Test Answers - L1qmwdb2k27kNo ratings yet

- Chapter 1audi 2015 DUDocument10 pagesChapter 1audi 2015 DUMoti BekeleNo ratings yet

- SM ch01Document13 pagesSM ch01tikaa13290No ratings yet

- Auditing Teaching MaterialDocument49 pagesAuditing Teaching MaterialGetachew JoriyeNo ratings yet

- I. Short Essay QuestionsDocument2 pagesI. Short Essay QuestionsPearl Isabelle SudarioNo ratings yet

- The Art and Science of Auditing: Principles, Practices, and InsightsFrom EverandThe Art and Science of Auditing: Principles, Practices, and InsightsNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Financial Intelligence: Mastering the Numbers for Business SuccessFrom EverandFinancial Intelligence: Mastering the Numbers for Business SuccessNo ratings yet

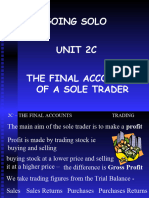

- Final Accounts - 2CDocument8 pagesFinal Accounts - 2CSaleh RaoufNo ratings yet

- 2211posting 061cab6e3d56f89 03363994Document12 pages2211posting 061cab6e3d56f89 03363994Saleh RaoufNo ratings yet

- CompaniesDocument39 pagesCompaniesSaleh RaoufNo ratings yet

- Reconciliation of CostDocument7 pagesReconciliation of CostSaleh RaoufNo ratings yet

- Auditing Chapter (1) - Second Part 2023Document10 pagesAuditing Chapter (1) - Second Part 2023Saleh RaoufNo ratings yet

- Lecture8 Cost AccountingDocument8 pagesLecture8 Cost AccountingSaleh RaoufNo ratings yet

- Lecture7 Cost AccountingDocument9 pagesLecture7 Cost AccountingSaleh RaoufNo ratings yet

- Arens Aas17 PPT 24Document53 pagesArens Aas17 PPT 24Saleh RaoufNo ratings yet

- Auditing LectureDocument13 pagesAuditing LectureSaleh RaoufNo ratings yet

- Auditing Chapter (1) - Four Part 2023Document12 pagesAuditing Chapter (1) - Four Part 2023Saleh RaoufNo ratings yet

- Auditing LectureDocument17 pagesAuditing LectureSaleh RaoufNo ratings yet

- Macabacus Fundamentals Demo - BlankDocument16 pagesMacabacus Fundamentals Demo - BlankSaleh Raouf100% (1)

- Proofing DemoDocument2 pagesProofing DemoSaleh RaoufNo ratings yet

- Auditing Chapter (1) Three Part 2023Document22 pagesAuditing Chapter (1) Three Part 2023Saleh RaoufNo ratings yet

- B Exercises: E24-1B (Post-Balance-Sheet Events) (A) (B)Document4 pagesB Exercises: E24-1B (Post-Balance-Sheet Events) (A) (B)Saleh RaoufNo ratings yet

- Auditing LectureDocument20 pagesAuditing LectureSaleh RaoufNo ratings yet

- CH 23Document8 pagesCH 23Saleh RaoufNo ratings yet

- CIB Practice Numerical Reasoning Test SolutionDocument22 pagesCIB Practice Numerical Reasoning Test SolutionSaleh RaoufNo ratings yet

- Lesson 1: Learning ObjectivesDocument7 pagesLesson 1: Learning ObjectivesSaleh RaoufNo ratings yet

- CH 20Document8 pagesCH 20Saleh RaoufNo ratings yet

- Macabacus Fundamentals Demo - BlankDocument16 pagesMacabacus Fundamentals Demo - BlankSaleh Raouf100% (1)

- CH 21Document6 pagesCH 21Saleh RaoufNo ratings yet

- CH 19Document8 pagesCH 19Saleh RaoufNo ratings yet

- CH 22Document8 pagesCH 22Saleh RaoufNo ratings yet

- CH 13Document6 pagesCH 13Saleh RaoufNo ratings yet

- CH 06Document4 pagesCH 06Saleh RaoufNo ratings yet

- CH 16Document8 pagesCH 16Saleh RaoufNo ratings yet

- CH 15Document8 pagesCH 15Saleh RaoufNo ratings yet

- CH 14Document6 pagesCH 14Saleh RaoufNo ratings yet

- CH 11Document6 pagesCH 11Saleh RaoufNo ratings yet

- 3rd Round Wise GATE Cut Off of All Round AY 2024-25 v555 - Copy (1) (1) - RemovedDocument2 pages3rd Round Wise GATE Cut Off of All Round AY 2024-25 v555 - Copy (1) (1) - RemovedAgony SinghNo ratings yet

- Drug Calculations Practice NCLEX Questions (100+Document2 pagesDrug Calculations Practice NCLEX Questions (100+obedidomNo ratings yet

- Carbon Fiber Quasi-Isotropic LaminateDocument3 pagesCarbon Fiber Quasi-Isotropic LaminateGonçalo FonsecaNo ratings yet

- Logcat 1710052670177Document13 pagesLogcat 1710052670177louishatabithaNo ratings yet

- School Improvement Through Better Grading PracticesDocument5 pagesSchool Improvement Through Better Grading PracticesMortega, John RodolfNo ratings yet

- Meaning of Home ArticleDocument19 pagesMeaning of Home Articlebrainhub50No ratings yet

- Task Complexity Affects Information Seek 104221Document35 pagesTask Complexity Affects Information Seek 104221vna297No ratings yet

- Derivative of Logarithmic and Exponential FunctionDocument3 pagesDerivative of Logarithmic and Exponential FunctionPrincessdy CocadizNo ratings yet

- A Survey On Intraday Traders - Google FormsDocument8 pagesA Survey On Intraday Traders - Google FormsAnju tpNo ratings yet

- Training - Bomb Threat ProceduresDocument4 pagesTraining - Bomb Threat ProceduresVintonNo ratings yet

- 5 Ways To Empower StudentsDocument13 pages5 Ways To Empower StudentsJesusa Franco DizonNo ratings yet

- Corporate PPT Template 20Document10 pagesCorporate PPT Template 20Mustafa RahmanNo ratings yet

- SAP S4 HANA Academy For Complete FreshersDocument15 pagesSAP S4 HANA Academy For Complete FreshersAdão da luzNo ratings yet

- Stenton Community TurbineDocument13 pagesStenton Community TurbineEttie SpencerNo ratings yet

- Passive Suppression of Nonlinear Panel Flutter Using Piezoelectric Materials With Resonant CircuitDocument12 pagesPassive Suppression of Nonlinear Panel Flutter Using Piezoelectric Materials With Resonant CircuitYonghui XUNo ratings yet

- Zoning Complaint Form 2010Document1 pageZoning Complaint Form 2010Web BinghamNo ratings yet

- Dissertation Tolga UhlmannDocument8 pagesDissertation Tolga UhlmannBestPaperWritingServiceClarksville100% (1)

- Course Outline 1. Course Code 2. Course Title 3. Pre - Requisite 4. CO - Requisite 5. Course Credit 6. Contact Hours/Semester 7. Course DescriptionDocument3 pagesCourse Outline 1. Course Code 2. Course Title 3. Pre - Requisite 4. CO - Requisite 5. Course Credit 6. Contact Hours/Semester 7. Course DescriptionFelica Delos ReyesNo ratings yet

- Research Proposal Guidelines MaldivesDocument2 pagesResearch Proposal Guidelines MaldivesmikeNo ratings yet

- Fluids Lab Experiment No:3 Fundamentals of Pressure MeasurementDocument14 pagesFluids Lab Experiment No:3 Fundamentals of Pressure MeasurementDarivan DuhokiNo ratings yet

- Li Kolar Li Et Al Research Development of Preload Technology On Angular Contact Ball Bearing of High Speed Spindle A Review (2020) PUBV 340215Document23 pagesLi Kolar Li Et Al Research Development of Preload Technology On Angular Contact Ball Bearing of High Speed Spindle A Review (2020) PUBV 340215fog900No ratings yet

- AmanDocument10 pagesAmanAmanVatsNo ratings yet

- Factors Affecting Resistance To Change MDocument35 pagesFactors Affecting Resistance To Change MRia Patterson100% (1)

- Anatomy Reviewer: Body Cavity Is Any Fluid-Filled Space in A Multicellular Organism Other Than Those of VesselsDocument3 pagesAnatomy Reviewer: Body Cavity Is Any Fluid-Filled Space in A Multicellular Organism Other Than Those of VesselsIvan LimNo ratings yet

- Hasan Abdal Past PaperDocument20 pagesHasan Abdal Past Paperlovefist402No ratings yet

- Term-2 - Grade 8 Social Science Mock Test-2Document4 pagesTerm-2 - Grade 8 Social Science Mock Test-2bhagatNo ratings yet

- Humphree Course StabilisingDocument8 pagesHumphree Course StabilisingMatNo ratings yet

- Benchtop Universal Testing MachineDocument8 pagesBenchtop Universal Testing Machineharan2000No ratings yet

Download as pptx, pdf, or txt

You might also like

- Question 1 - Expository EssayDocument3 pagesQuestion 1 - Expository EssayMahinNo ratings yet

- Auditing International Approach NotesDocument29 pagesAuditing International Approach NotesRayz100% (1)

- Arens Auditing16e SM 01Document14 pagesArens Auditing16e SM 01Ji RenNo ratings yet

- Factory Studio User GuideDocument218 pagesFactory Studio User GuideTulio Silva100% (1)

- Chapter - 1THE DEMAND FOR AUDIT AND OTHER ASSURANCE SERVICESDocument46 pagesChapter - 1THE DEMAND FOR AUDIT AND OTHER ASSURANCE SERVICESDina AlfawalNo ratings yet

- (Objective 1-1) : Ayu Safitri (1902113029) Auditing 1 Review Question CH 1, Page 18Document3 pages(Objective 1-1) : Ayu Safitri (1902113029) Auditing 1 Review Question CH 1, Page 18Ayu SafitriNo ratings yet

- Audit UNIT 1Document9 pagesAudit UNIT 1Nigussie BerhanuNo ratings yet

- Auditing: Module 1overview of Auditing and Pre-Engagement ActivitiesDocument22 pagesAuditing: Module 1overview of Auditing and Pre-Engagement ActivitiesElla Jane Buenaventura JimenezNo ratings yet

- 1 AuditDocument9 pages1 Auditahmed sheblNo ratings yet

- Chapter 03 - Answer PDFDocument8 pagesChapter 03 - Answer PDFjhienellNo ratings yet

- Sheet AnswerDocument8 pagesSheet Answeramir rabieNo ratings yet

- Auditing I CH I-3Document64 pagesAuditing I CH I-3mercyteshite5No ratings yet

- CH 1Document34 pagesCH 1Ram KumarNo ratings yet

- Auditing Theory Cabrera 2010 Chap 2Document8 pagesAuditing Theory Cabrera 2010 Chap 2Squishy potatoNo ratings yet

- Auditing Ch1 by MekaDocument7 pagesAuditing Ch1 by MekaEbsa AbdiNo ratings yet

- Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions ManualDocument16 pagesAuditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manualterrysmithnoejaxfwbz100% (14)

- Chapter 02 Overview of AuditingDocument26 pagesChapter 02 Overview of AuditingRichard de LeonNo ratings yet

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document12 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1WandaTifanyArantikaNo ratings yet

- Chap. 1Document2 pagesChap. 1Al Mo SaintNo ratings yet

- Chapter 1 - Assurance & Engagement (Audit Theory) 2010e - Ma. Elenita B. Cabrera - Chapter 02Document8 pagesChapter 1 - Assurance & Engagement (Audit Theory) 2010e - Ma. Elenita B. Cabrera - Chapter 02Pol AnduLanNo ratings yet

- DocumentDocument7 pagesDocumenttafadzwagutusaNo ratings yet

- Auditing Principle I - CH 1Document6 pagesAuditing Principle I - CH 1keyruebrahim44No ratings yet

- SB7e WYRNTK Ch01Document3 pagesSB7e WYRNTK Ch01Joey LinNo ratings yet

- Perform Auditing and ReportingDocument65 pagesPerform Auditing and ReportingMulugeta GebinoNo ratings yet

- Chapter 1-3 SumaaryDocument16 pagesChapter 1-3 SumaaryLovely Jane Raut CabiltoNo ratings yet

- Solution Manual For Auditing and Assurance Services 17th by ArensDocument15 pagesSolution Manual For Auditing and Assurance Services 17th by ArensMarsha Johnson100% (33)

- Matriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreDocument12 pagesMatriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreKen KiongNo ratings yet

- Auditing Principle 1 - ch1Document7 pagesAuditing Principle 1 - ch1Duguma BejigaNo ratings yet

- Audit Summary Chapter 1Document5 pagesAudit Summary Chapter 1saniastariNo ratings yet

- Unit 1: An Overview of AuditingDocument12 pagesUnit 1: An Overview of AuditingYonasNo ratings yet

- Comp. Lesson 7Document18 pagesComp. Lesson 7Ryan Prado AndayaNo ratings yet

- Auditing Principles and PracticesDocument58 pagesAuditing Principles and PracticeskainatNo ratings yet

- IPFM Chapter 1Document20 pagesIPFM Chapter 1Yitera SisayNo ratings yet

- The Demand For Audit and Other Assurance Services: Concept Checks P. 34Document15 pagesThe Demand For Audit and Other Assurance Services: Concept Checks P. 34hsingting yu100% (2)

- Chapter 1 The Demand For Audit and Other Assurance ServicesDocument40 pagesChapter 1 The Demand For Audit and Other Assurance ServicesSerina PangarifNo ratings yet

- Verifiable Form Criteria Quantifiable Information Subjective InformationDocument5 pagesVerifiable Form Criteria Quantifiable Information Subjective InformationAnonymous BwN1AVNo ratings yet

- Maseno Universit1Document9 pagesMaseno Universit1Simon MutuaNo ratings yet

- Tutorial 1Document16 pagesTutorial 1youssefasaadNo ratings yet

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document13 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1Audric AzfarNo ratings yet

- Adv. Aud All Class Short-1Document223 pagesAdv. Aud All Class Short-1Abraha Aregay100% (2)

- Full Download Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions ManualDocument36 pagesFull Download Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manualpickersgillvandapro100% (32)

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document13 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1Kristel Nuyda LobasNo ratings yet

- Solutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsDocument26 pagesSolutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsStefany Mie MosendeNo ratings yet

- Arens Auditing16e SM 01Document14 pagesArens Auditing16e SM 01Mohd KdNo ratings yet

- AUDITINGDocument13 pagesAUDITINGGrace AlolorNo ratings yet

- Chapter 1 NotesDocument8 pagesChapter 1 NotesmatthewNo ratings yet

- Chapter 1Document8 pagesChapter 1mostafakhaled333No ratings yet

- Dwnload Full Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manual PDFDocument36 pagesDwnload Full Auditing Assurance Services and Ethics in Australia 9th Edition Arens Solutions Manual PDFbendvvduncan100% (21)

- The Demand For Audit and Other Assurance Services: Review Questions 1-1Document13 pagesThe Demand For Audit and Other Assurance Services: Review Questions 1-1Monique CabreraNo ratings yet

- Audit Solution - Chapter 1Document13 pagesAudit Solution - Chapter 1Hoài NamNo ratings yet

- Chapter 7: Introduction To Financial Statement AuditDocument18 pagesChapter 7: Introduction To Financial Statement AuditkripsNo ratings yet

- IM-01 Overview of Audit and Other Assurance ServicesDocument7 pagesIM-01 Overview of Audit and Other Assurance Servicesharley_quinn11No ratings yet

- Principles of Auditing ZicaDocument431 pagesPrinciples of Auditing ZicaDixie CheeloNo ratings yet

- AUDMOD1 Overview of Auditing and Pre-EngagemeDocument26 pagesAUDMOD1 Overview of Auditing and Pre-EngagemeJohn Archie AntonioNo ratings yet

- Self - Test Answers - L1Document2 pagesSelf - Test Answers - L1qmwdb2k27kNo ratings yet

- Chapter 1audi 2015 DUDocument10 pagesChapter 1audi 2015 DUMoti BekeleNo ratings yet

- SM ch01Document13 pagesSM ch01tikaa13290No ratings yet

- Auditing Teaching MaterialDocument49 pagesAuditing Teaching MaterialGetachew JoriyeNo ratings yet

- I. Short Essay QuestionsDocument2 pagesI. Short Essay QuestionsPearl Isabelle SudarioNo ratings yet

- The Art and Science of Auditing: Principles, Practices, and InsightsFrom EverandThe Art and Science of Auditing: Principles, Practices, and InsightsNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Financial Intelligence: Mastering the Numbers for Business SuccessFrom EverandFinancial Intelligence: Mastering the Numbers for Business SuccessNo ratings yet

- Final Accounts - 2CDocument8 pagesFinal Accounts - 2CSaleh RaoufNo ratings yet

- 2211posting 061cab6e3d56f89 03363994Document12 pages2211posting 061cab6e3d56f89 03363994Saleh RaoufNo ratings yet

- CompaniesDocument39 pagesCompaniesSaleh RaoufNo ratings yet

- Reconciliation of CostDocument7 pagesReconciliation of CostSaleh RaoufNo ratings yet

- Auditing Chapter (1) - Second Part 2023Document10 pagesAuditing Chapter (1) - Second Part 2023Saleh RaoufNo ratings yet

- Lecture8 Cost AccountingDocument8 pagesLecture8 Cost AccountingSaleh RaoufNo ratings yet

- Lecture7 Cost AccountingDocument9 pagesLecture7 Cost AccountingSaleh RaoufNo ratings yet

- Arens Aas17 PPT 24Document53 pagesArens Aas17 PPT 24Saleh RaoufNo ratings yet

- Auditing LectureDocument13 pagesAuditing LectureSaleh RaoufNo ratings yet

- Auditing Chapter (1) - Four Part 2023Document12 pagesAuditing Chapter (1) - Four Part 2023Saleh RaoufNo ratings yet

- Auditing LectureDocument17 pagesAuditing LectureSaleh RaoufNo ratings yet

- Macabacus Fundamentals Demo - BlankDocument16 pagesMacabacus Fundamentals Demo - BlankSaleh Raouf100% (1)

- Proofing DemoDocument2 pagesProofing DemoSaleh RaoufNo ratings yet

- Auditing Chapter (1) Three Part 2023Document22 pagesAuditing Chapter (1) Three Part 2023Saleh RaoufNo ratings yet

- B Exercises: E24-1B (Post-Balance-Sheet Events) (A) (B)Document4 pagesB Exercises: E24-1B (Post-Balance-Sheet Events) (A) (B)Saleh RaoufNo ratings yet

- Auditing LectureDocument20 pagesAuditing LectureSaleh RaoufNo ratings yet

- CH 23Document8 pagesCH 23Saleh RaoufNo ratings yet

- CIB Practice Numerical Reasoning Test SolutionDocument22 pagesCIB Practice Numerical Reasoning Test SolutionSaleh RaoufNo ratings yet

- Lesson 1: Learning ObjectivesDocument7 pagesLesson 1: Learning ObjectivesSaleh RaoufNo ratings yet

- CH 20Document8 pagesCH 20Saleh RaoufNo ratings yet

- Macabacus Fundamentals Demo - BlankDocument16 pagesMacabacus Fundamentals Demo - BlankSaleh Raouf100% (1)

- CH 21Document6 pagesCH 21Saleh RaoufNo ratings yet

- CH 19Document8 pagesCH 19Saleh RaoufNo ratings yet

- CH 22Document8 pagesCH 22Saleh RaoufNo ratings yet

- CH 13Document6 pagesCH 13Saleh RaoufNo ratings yet

- CH 06Document4 pagesCH 06Saleh RaoufNo ratings yet

- CH 16Document8 pagesCH 16Saleh RaoufNo ratings yet

- CH 15Document8 pagesCH 15Saleh RaoufNo ratings yet

- CH 14Document6 pagesCH 14Saleh RaoufNo ratings yet

- CH 11Document6 pagesCH 11Saleh RaoufNo ratings yet

- 3rd Round Wise GATE Cut Off of All Round AY 2024-25 v555 - Copy (1) (1) - RemovedDocument2 pages3rd Round Wise GATE Cut Off of All Round AY 2024-25 v555 - Copy (1) (1) - RemovedAgony SinghNo ratings yet

- Drug Calculations Practice NCLEX Questions (100+Document2 pagesDrug Calculations Practice NCLEX Questions (100+obedidomNo ratings yet

- Carbon Fiber Quasi-Isotropic LaminateDocument3 pagesCarbon Fiber Quasi-Isotropic LaminateGonçalo FonsecaNo ratings yet

- Logcat 1710052670177Document13 pagesLogcat 1710052670177louishatabithaNo ratings yet

- School Improvement Through Better Grading PracticesDocument5 pagesSchool Improvement Through Better Grading PracticesMortega, John RodolfNo ratings yet

- Meaning of Home ArticleDocument19 pagesMeaning of Home Articlebrainhub50No ratings yet

- Task Complexity Affects Information Seek 104221Document35 pagesTask Complexity Affects Information Seek 104221vna297No ratings yet

- Derivative of Logarithmic and Exponential FunctionDocument3 pagesDerivative of Logarithmic and Exponential FunctionPrincessdy CocadizNo ratings yet

- A Survey On Intraday Traders - Google FormsDocument8 pagesA Survey On Intraday Traders - Google FormsAnju tpNo ratings yet

- Training - Bomb Threat ProceduresDocument4 pagesTraining - Bomb Threat ProceduresVintonNo ratings yet

- 5 Ways To Empower StudentsDocument13 pages5 Ways To Empower StudentsJesusa Franco DizonNo ratings yet

- Corporate PPT Template 20Document10 pagesCorporate PPT Template 20Mustafa RahmanNo ratings yet

- SAP S4 HANA Academy For Complete FreshersDocument15 pagesSAP S4 HANA Academy For Complete FreshersAdão da luzNo ratings yet

- Stenton Community TurbineDocument13 pagesStenton Community TurbineEttie SpencerNo ratings yet

- Passive Suppression of Nonlinear Panel Flutter Using Piezoelectric Materials With Resonant CircuitDocument12 pagesPassive Suppression of Nonlinear Panel Flutter Using Piezoelectric Materials With Resonant CircuitYonghui XUNo ratings yet

- Zoning Complaint Form 2010Document1 pageZoning Complaint Form 2010Web BinghamNo ratings yet

- Dissertation Tolga UhlmannDocument8 pagesDissertation Tolga UhlmannBestPaperWritingServiceClarksville100% (1)

- Course Outline 1. Course Code 2. Course Title 3. Pre - Requisite 4. CO - Requisite 5. Course Credit 6. Contact Hours/Semester 7. Course DescriptionDocument3 pagesCourse Outline 1. Course Code 2. Course Title 3. Pre - Requisite 4. CO - Requisite 5. Course Credit 6. Contact Hours/Semester 7. Course DescriptionFelica Delos ReyesNo ratings yet

- Research Proposal Guidelines MaldivesDocument2 pagesResearch Proposal Guidelines MaldivesmikeNo ratings yet

- Fluids Lab Experiment No:3 Fundamentals of Pressure MeasurementDocument14 pagesFluids Lab Experiment No:3 Fundamentals of Pressure MeasurementDarivan DuhokiNo ratings yet

- Li Kolar Li Et Al Research Development of Preload Technology On Angular Contact Ball Bearing of High Speed Spindle A Review (2020) PUBV 340215Document23 pagesLi Kolar Li Et Al Research Development of Preload Technology On Angular Contact Ball Bearing of High Speed Spindle A Review (2020) PUBV 340215fog900No ratings yet

- AmanDocument10 pagesAmanAmanVatsNo ratings yet

- Factors Affecting Resistance To Change MDocument35 pagesFactors Affecting Resistance To Change MRia Patterson100% (1)

- Anatomy Reviewer: Body Cavity Is Any Fluid-Filled Space in A Multicellular Organism Other Than Those of VesselsDocument3 pagesAnatomy Reviewer: Body Cavity Is Any Fluid-Filled Space in A Multicellular Organism Other Than Those of VesselsIvan LimNo ratings yet

- Hasan Abdal Past PaperDocument20 pagesHasan Abdal Past Paperlovefist402No ratings yet

- Term-2 - Grade 8 Social Science Mock Test-2Document4 pagesTerm-2 - Grade 8 Social Science Mock Test-2bhagatNo ratings yet

- Humphree Course StabilisingDocument8 pagesHumphree Course StabilisingMatNo ratings yet

- Benchtop Universal Testing MachineDocument8 pagesBenchtop Universal Testing Machineharan2000No ratings yet