Download as pptx, pdf, or txt

You might also like

- LM03 Analyzing Balance Sheets IFT NotesDocument11 pagesLM03 Analyzing Balance Sheets IFT NotesClaptrapjackNo ratings yet

- THERMO KING TK 61377-18-MM TKV500 and TKV600 Maintenance Manual Rev. A 01-19Document108 pagesTHERMO KING TK 61377-18-MM TKV500 and TKV600 Maintenance Manual Rev. A 01-19Vincent Marmande100% (1)

- Session 2Document27 pagesSession 2I don't knowNo ratings yet

- CH 05Document59 pagesCH 05نوف حميدNo ratings yet

- Balace SheetDocument9 pagesBalace Sheetkundusangeeta2No ratings yet

- SSLIDES - VATEL - LSLIDES - Chap 4Document36 pagesSSLIDES - VATEL - LSLIDES - Chap 4uyenthanhtran2312No ratings yet

- Golis University: Faculty of Business and Economics Chapter Six Balance SheetDocument22 pagesGolis University: Faculty of Business and Economics Chapter Six Balance Sheetsaed cabdiNo ratings yet

- Presentation On Corporate Finance: By: Sunita SasankanDocument21 pagesPresentation On Corporate Finance: By: Sunita SasankanLauren MontoyaNo ratings yet

- Chapter 2 WileyDocument29 pagesChapter 2 Wileyp876468No ratings yet

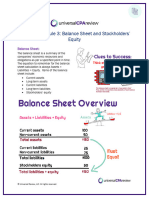

- Chapter 1 Module 3: Balance Sheet and Stockholders' EquityDocument6 pagesChapter 1 Module 3: Balance Sheet and Stockholders' Equityhmaz.roid91No ratings yet

- Lecture 01Document50 pagesLecture 01Anon sonNo ratings yet

- CPA - FR - Module 1 - The Role and Importance of Financial ReportingDocument11 pagesCPA - FR - Module 1 - The Role and Importance of Financial ReportingqueendillyNo ratings yet

- Chapter 13Document79 pagesChapter 13m.garagan16No ratings yet

- Balance SheetDocument25 pagesBalance SheetDHANUSHA BALAKRISHNANNo ratings yet

- IntroductionDocument19 pagesIntroductionFabiolaNo ratings yet

- Chapter 2 2020 StudentDocument43 pagesChapter 2 2020 StudentHương NguyễnNo ratings yet

- Commercial AccountingDocument16 pagesCommercial AccountingAaditya Pandey AmritNo ratings yet

- CH 5Document58 pagesCH 5marwan2004acctNo ratings yet

- FA Part-2 BS 45-1Document131 pagesFA Part-2 BS 45-1Phạm Duy Long Đinh100% (1)

- Fabm2 1Document17 pagesFabm2 1Jacel GadonNo ratings yet

- Chapter 2 - Financial Statements & The Annual Report: Objectives of Financial ReportingDocument6 pagesChapter 2 - Financial Statements & The Annual Report: Objectives of Financial ReportingHareem Zoya WarsiNo ratings yet

- Accounting - Instructor-1Document154 pagesAccounting - Instructor-1karimhisham100% (1)

- Tutorial A40 Kis Aktuaria/Materi TGL 15 A40Document40 pagesTutorial A40 Kis Aktuaria/Materi TGL 15 A40nirmalazintaNo ratings yet

- 1 ACTX01 SFP Partial Joy Division ADocument48 pages1 ACTX01 SFP Partial Joy Division ACece Shewna OrbinoNo ratings yet

- 5 Balance Sheet and Statement of Cash Flows SystemsDocument22 pages5 Balance Sheet and Statement of Cash Flows SystemsMurugan RèÿésNo ratings yet

- Bab 5 Analisis Laporan KeuanganDocument54 pagesBab 5 Analisis Laporan KeuanganBenedict MihoyoNo ratings yet

- Chapter 9: Balance Sheet and Statement of Cash Flows SystemsDocument21 pagesChapter 9: Balance Sheet and Statement of Cash Flows SystemsPUTTU GURU PRASAD SENGUNTHA MUDALIARNo ratings yet

- Intermediate Accounting: Non-Financial and Current LiabilitiesDocument79 pagesIntermediate Accounting: Non-Financial and Current LiabilitiesShuo LuNo ratings yet

- Thomas FAM Ch02 Student AccessibleDocument73 pagesThomas FAM Ch02 Student AccessibleNeel PeswaniNo ratings yet

- CH 05Document107 pagesCH 05Sabbir ahmedNo ratings yet

- Chapter 5Document42 pagesChapter 5Dx xDNo ratings yet

- Chapter 2 Balance SheetDocument14 pagesChapter 2 Balance SheetLuu Nhat MinhNo ratings yet

- Financial AccountingDocument46 pagesFinancial Accountingkajol.leoNo ratings yet

- Chapter 2 NLKTDocument58 pagesChapter 2 NLKTPhan Lê Anh Đào100% (1)

- CCFC 511 - Chapter 5 (Part 3)Document9 pagesCCFC 511 - Chapter 5 (Part 3)michi.berto.2020No ratings yet

- L1-Introduction To AccountingDocument67 pagesL1-Introduction To AccountingSYAMIMI ANUARNo ratings yet

- Intermediate Accounting: Conceptual Framework Underlying Financial ReportingDocument45 pagesIntermediate Accounting: Conceptual Framework Underlying Financial ReportingashleyalicerogersNo ratings yet

- Topic 5c - Audit of Shareholders' Equity and Long Term LiabilityDocument14 pagesTopic 5c - Audit of Shareholders' Equity and Long Term LiabilityLANGITBIRUNo ratings yet

- Accounting From A Global PerspectiveDocument58 pagesAccounting From A Global PerspectivezelNo ratings yet

- Internal Control Affecting Liabilities and EquityDocument2 pagesInternal Control Affecting Liabilities and EquityMagayon JovelynNo ratings yet

- Audit II 7new - 3Document15 pagesAudit II 7new - 3Muktar Xahaa100% (1)

- Financial Management: Group-2Document53 pagesFinancial Management: Group-2RISHAV NAGULENo ratings yet

- Student Notes Chap 5Document7 pagesStudent Notes Chap 5Bhoomi GoyalNo ratings yet

- Business Management & MarketingDocument16 pagesBusiness Management & MarketingKofiya WillieNo ratings yet

- Chapter2 Accounting PrincipleDocument55 pagesChapter2 Accounting PrincipleMinh Huyền Nguyễn100% (2)

- Session 5 - Financial Statement AnalysisDocument42 pagesSession 5 - Financial Statement AnalysisVaibhav JainNo ratings yet

- Lec 10Document27 pagesLec 10Ritik KumarNo ratings yet

- Fundamentals of AccountingDocument32 pagesFundamentals of AccountingJoshua Jay JesuroNo ratings yet

- CH 06Document64 pagesCH 06نوف حميدNo ratings yet

- ShobhitDocument12 pagesShobhitAshutosh GuptaNo ratings yet

- Conceptual FrameworkDocument24 pagesConceptual FrameworkShin Wei ChaiNo ratings yet

- Week 5/6 Lecture: Covers: Chapter 5 of The Textbook Up To Learning Objective 9 On Page 172Document31 pagesWeek 5/6 Lecture: Covers: Chapter 5 of The Textbook Up To Learning Objective 9 On Page 172cooljani01No ratings yet

- Balance Sheet and Statement of Cash Flows SystemsDocument21 pagesBalance Sheet and Statement of Cash Flows SystemsshubhamNo ratings yet

- Fsa - Ifim UseDocument80 pagesFsa - Ifim Usesubhrodeep chowdhuryNo ratings yet

- Introduction To AccountingDocument15 pagesIntroduction To Accountingluna dupontNo ratings yet

- 07 - TA - Liabilities and EquityDocument30 pages07 - TA - Liabilities and EquitySalma HauraNo ratings yet

- Lecture 1Document38 pagesLecture 1crystate17No ratings yet

- Syllabus Summary Course: Financial Statement Analysis and Valuation (F-401)Document8 pagesSyllabus Summary Course: Financial Statement Analysis and Valuation (F-401)Md Ohidur RahmanNo ratings yet

- Chapter 2 - Understanding The Balance SheetDocument54 pagesChapter 2 - Understanding The Balance SheetNguyễn Yến NhiNo ratings yet

- Cultural Variations and Social Differences (Ethnicity)Document19 pagesCultural Variations and Social Differences (Ethnicity)Jomar TeofiloNo ratings yet

- Training - BAtteriesDocument9 pagesTraining - BAtteriesWilly DuranNo ratings yet

- Gr10 Ch13.4 TBDocument5 pagesGr10 Ch13.4 TBnr46jpdxbpNo ratings yet

- Qualitative Research NotesDocument8 pagesQualitative Research NotesAnanta SinhaNo ratings yet

- Gestational Diabetes Diet - What To Eat For A Healthy Pregnancy PDFDocument9 pagesGestational Diabetes Diet - What To Eat For A Healthy Pregnancy PDFJibin John JacksonNo ratings yet

- Push Button Typical WiringDocument12 pagesPush Button Typical Wiringstrob1974No ratings yet

- Tle 6 Lesson 3Document8 pagesTle 6 Lesson 3Mayaman UsmanNo ratings yet

- Database SecurityDocument19 pagesDatabase SecurityVinay VenkatramanNo ratings yet

- Hypertensive Patients Knowledge, Self-Care ManagementDocument10 pagesHypertensive Patients Knowledge, Self-Care ManagementLilian ArthoNo ratings yet

- Modern Business Statistics With Microsoft Office Excel 4Th Edition Anderson Solutions Manual Full Chapter PDFDocument47 pagesModern Business Statistics With Microsoft Office Excel 4Th Edition Anderson Solutions Manual Full Chapter PDFjerryholdengewmqtspaj100% (11)

- Market SegmentationDocument30 pagesMarket Segmentationmldc2011No ratings yet

- Belzona 5111 Product Data SheetDocument2 pagesBelzona 5111 Product Data SheetPeter RhoadsNo ratings yet

- 1850 Firstphasepgmedicaldegreediplomacollegewiseallotments201920Document59 pages1850 Firstphasepgmedicaldegreediplomacollegewiseallotments201920krishnaNo ratings yet

- 1) What Is Budgetary Control?Document6 pages1) What Is Budgetary Control?abhiayushNo ratings yet

- Judicial Review CSGDocument13 pagesJudicial Review CSGSushmaNo ratings yet

- SHRM PerspectivesDocument14 pagesSHRM PerspectivesNoman Ul Haq Siddiqui100% (2)

- Cara Membaca Analisis Gas Darah Arteri (AGDA)Document27 pagesCara Membaca Analisis Gas Darah Arteri (AGDA)Martin Susanto, MD67% (3)

- Zero Acceptance Number Sampling Plan 57 372 DemoDocument5 pagesZero Acceptance Number Sampling Plan 57 372 DemoBALAJINo ratings yet

- The Truth About The Truth MovementDocument68 pagesThe Truth About The Truth MovementgordoneastNo ratings yet

- Owner Manual - Avh-A205bt - Avh-A105dvd RC AseanDocument140 pagesOwner Manual - Avh-A205bt - Avh-A105dvd RC AseanalejandrohukNo ratings yet

- Maths Specimen Paper 1 2014 2017Document16 pagesMaths Specimen Paper 1 2014 2017Ly Shan100% (1)

- GloverDocument272 pagesGlovermidialaoropesaNo ratings yet

- Journaling PDFDocument1 pageJournaling PDFMargarita Maria Botero PerezNo ratings yet

- Professional English 1: WEB 20202 Ms Noorhayati SaharuddinDocument20 pagesProfessional English 1: WEB 20202 Ms Noorhayati SaharuddinAdellNo ratings yet

- TRANSITIONS 5 WebDocument40 pagesTRANSITIONS 5 WebCARDONA CHANG Micaela AlessandraNo ratings yet

- SOLIDserver Administrator Guide 5.0.3Document1,041 pagesSOLIDserver Administrator Guide 5.0.3proutNo ratings yet

- Lightolier Lytecaster 7-11 Downlights Brochure 1980Document8 pagesLightolier Lytecaster 7-11 Downlights Brochure 1980Alan MastersNo ratings yet

- DAFPUSDocument3 pagesDAFPUSNabila SalehNo ratings yet

- Manual Motores DieselDocument112 pagesManual Motores Dieselaldo pelaldoNo ratings yet