CH 9 Risk

CH 9 Risk

You might also like

- Study Guide: Certified Information Systems Security OfficerDocument33 pagesStudy Guide: Certified Information Systems Security Officerellococareloco100% (1)

- CISSP - 1 Information Security & Risk ManagementDocument60 pagesCISSP - 1 Information Security & Risk ManagementlebenikosNo ratings yet

- Information Security Governance and Risk ManagementDocument6 pagesInformation Security Governance and Risk Managementjbrackett239No ratings yet

- Risk Management 1Document41 pagesRisk Management 1Amit Agarwal100% (2)

- CC7178 Cyber Security Management: Presenter: Kiran Kumar ShahDocument31 pagesCC7178 Cyber Security Management: Presenter: Kiran Kumar ShahManish SharmaNo ratings yet

- Risk Management: Predict - Preempt - ProtectDocument31 pagesRisk Management: Predict - Preempt - ProtectFerry100% (2)

- Information Security Governance and RiskDocument26 pagesInformation Security Governance and RiskSakil MahmudNo ratings yet

- Information Security Risk AnalysisDocument42 pagesInformation Security Risk AnalysisRishabh kapoorNo ratings yet

- Cisa Notes 2010Document26 pagesCisa Notes 2010Amanda Christine WijayaNo ratings yet

- Module 4 Ias321 Risk ManagementDocument12 pagesModule 4 Ias321 Risk ManagementMALLARI, HANNAH M.No ratings yet

- CSSLP 2016 NotesDocument26 pagesCSSLP 2016 Notesparul154No ratings yet

- Information Risk ManagementDocument30 pagesInformation Risk ManagementPukhrajNo ratings yet

- Risk Management-Assessing and Controlling RisksDocument43 pagesRisk Management-Assessing and Controlling RisksEswin AngelNo ratings yet

- A719552767 - 24968 - 24 - 2019 - ppt4 Info RiskDocument30 pagesA719552767 - 24968 - 24 - 2019 - ppt4 Info RiskVinay Singh Bittu100% (1)

- CISSP 8 DomainsDocument508 pagesCISSP 8 DomainsAntonio Galvez100% (10)

- "Risks in Information System ": Prepared By: Manoj Kumar Attri 23-MBA-2011Document26 pages"Risks in Information System ": Prepared By: Manoj Kumar Attri 23-MBA-2011Amit Pal SinghNo ratings yet

- IRM Lecture 6 - Information Security and Risk ManagementDocument7 pagesIRM Lecture 6 - Information Security and Risk ManagementLimberto SuarezNo ratings yet

- 304 SlideDocument46 pages304 SlidejavabeanNo ratings yet

- Isaa 2Document31 pagesIsaa 2rishabh agrawalNo ratings yet

- NIST SP800-30 Approach To Risk AssessmentDocument6 pagesNIST SP800-30 Approach To Risk AssessmentBabby BossNo ratings yet

- Informtion Risk ManagementDocument54 pagesInformtion Risk ManagementMuhammad IbrahimNo ratings yet

- Information Risk ManagementDocument29 pagesInformation Risk ManagementAnas Inam100% (1)

- Information Security Risk AnalysisDocument27 pagesInformation Security Risk AnalysisMahesh SinghNo ratings yet

- Risk Management: ISEC 4340Document166 pagesRisk Management: ISEC 4340يُ يَNo ratings yet

- Risk Analysis Nina GodboleDocument23 pagesRisk Analysis Nina GodboleRupesh AkulaNo ratings yet

- Unit 3 - Threat ModellingDocument13 pagesUnit 3 - Threat ModellingNivedhithaNo ratings yet

- CHAP 3 RM PROCESS ModifiedDocument36 pagesCHAP 3 RM PROCESS ModifiedhaiqalNo ratings yet

- ISA1 Module2Topic5Document67 pagesISA1 Module2Topic5サカイ アルジェイNo ratings yet

- FALLSEM2020-21 CSE3501 ETH VL2020210102645 Reference Material I 08-Sep-2020 Risk Management - V2Document171 pagesFALLSEM2020-21 CSE3501 ETH VL2020210102645 Reference Material I 08-Sep-2020 Risk Management - V2Game CrewNo ratings yet

- Incident ManagementDocument18 pagesIncident ManagementBalan Wv100% (1)

- Week 6 Risk Assessment and Analysis Part 1 2Document55 pagesWeek 6 Risk Assessment and Analysis Part 1 2Very danggerNo ratings yet

- Module-5: Risk Assessment & Configuration ReviewDocument28 pagesModule-5: Risk Assessment & Configuration ReviewAdityaNo ratings yet

- Day 7Document29 pagesDay 7scosee171No ratings yet

- Week 2 - Risk AssessmentDocument35 pagesWeek 2 - Risk AssessmentTahir BashirNo ratings yet

- Assignment Risk ManagementDocument5 pagesAssignment Risk ManagementHimanshu JainNo ratings yet

- Week 11Document55 pagesWeek 11rajnipriya0101No ratings yet

- Risk Assessment Frameworks: Rodney Petersen Government Relations Officer Security Task Force Coordinator EducauseDocument23 pagesRisk Assessment Frameworks: Rodney Petersen Government Relations Officer Security Task Force Coordinator EducausePiyush GuptaNo ratings yet

- Chapter 789101112Document54 pagesChapter 789101112Nasis DerejeNo ratings yet

- Manage Risk OMDocument2 pagesManage Risk OMVivek VashisthaNo ratings yet

- CISSP - 1 Information Security & Risk ManagementDocument60 pagesCISSP - 1 Information Security & Risk Managementjonty509No ratings yet

- Incident Management:-An Incident Is An Event That Could Lead To Loss Of, or Disruption To, AnDocument19 pagesIncident Management:-An Incident Is An Event That Could Lead To Loss Of, or Disruption To, Anjasmeet SinghNo ratings yet

- Risk Management (Cont'd)Document28 pagesRisk Management (Cont'd)Umar FarooqNo ratings yet

- Ch-05 Risk Management Tools and TechniquesDocument37 pagesCh-05 Risk Management Tools and TechniquesaafnanNo ratings yet

- Risk AssessmentDocument26 pagesRisk AssessmentANIRUDH B K 19BIT0348No ratings yet

- Important Definations - Risk ManagmentDocument11 pagesImportant Definations - Risk ManagmentomerNo ratings yet

- Risk Assessment: - By: Dedy Syamsuar, PHDDocument29 pagesRisk Assessment: - By: Dedy Syamsuar, PHDIstiarso BudiyuwonoNo ratings yet

- Comparison Between ISO 27005Document6 pagesComparison Between ISO 27005Indrian WahyudiNo ratings yet

- TQM, Lecture-11+12Document18 pagesTQM, Lecture-11+12Shakeel AhmadNo ratings yet

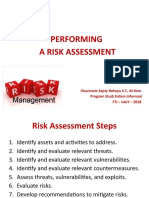

- Performing A Risk Assessment: Flourensia Sapty Rahayu S.T., M.KomDocument23 pagesPerforming A Risk Assessment: Flourensia Sapty Rahayu S.T., M.KomArinisa PakpahanNo ratings yet

- Lecture 5-White Board-20Dec2020Document12 pagesLecture 5-White Board-20Dec2020Plus PlusNo ratings yet

- Understanding Risk and Risk ManagementDocument30 pagesUnderstanding Risk and Risk ManagementSemargarengpetrukbagNo ratings yet

- Four Principles of ORM: Operational Risk Risk Human FactorsDocument10 pagesFour Principles of ORM: Operational Risk Risk Human FactorsivymaryNo ratings yet

- CISM 15e Domain2 New FormatDocument123 pagesCISM 15e Domain2 New Formatmrsph07No ratings yet

- Unit I Security Risk Assessment and ManagementDocument32 pagesUnit I Security Risk Assessment and ManagementShifa Khan100% (1)

- COSO FrameworkDocument47 pagesCOSO FrameworkMathew P. VargheseNo ratings yet

- ALS Limited Risk Management Policy and FrameworkDocument13 pagesALS Limited Risk Management Policy and FrameworkSyed Kashif AliNo ratings yet

- CH 04Document59 pagesCH 04faisal_cseduNo ratings yet

- CISA Exam-Testing Concept-Knowledge of Risk AssessmentFrom EverandCISA Exam-Testing Concept-Knowledge of Risk AssessmentRating: 2.5 out of 5 stars2.5/5 (4)

- CINS - 3044 - SAMPLE - SYLLABUS - CINS 3044-40277 FALL 2018.pdf. - 19-31-01 - 1-12-49pm - CINS 3044-40277 FALL 2018Document8 pagesCINS - 3044 - SAMPLE - SYLLABUS - CINS 3044-40277 FALL 2018.pdf. - 19-31-01 - 1-12-49pm - CINS 3044-40277 FALL 2018Naveed RiazNo ratings yet

- Topic 12Document36 pagesTopic 12Naveed RiazNo ratings yet

- Topic 5 - 2Document23 pagesTopic 5 - 2Naveed RiazNo ratings yet

- Topic 4 - 1Document23 pagesTopic 4 - 1Naveed RiazNo ratings yet

- L764000-XG11-00-CKL-150001 - FDS For PSS - RevGDocument104 pagesL764000-XG11-00-CKL-150001 - FDS For PSS - RevGAshok NavalNo ratings yet

- Section 5: Data Structures & AlgorithmsDocument12 pagesSection 5: Data Structures & AlgorithmsYT PremoneNo ratings yet

- Multimedia Presentation RubricDocument3 pagesMultimedia Presentation RubricMIKKIENNANo ratings yet

- PLC Motor LogicDocument5 pagesPLC Motor LogicInstrumentation ToolsNo ratings yet

- Org Four: Int 21H and INT 10H Programming and MacrosDocument31 pagesOrg Four: Int 21H and INT 10H Programming and MacrosBuket CüvelenkNo ratings yet

- 2020 Yr 12 Mathematics Extension 2 Task 1 Term 42019 V2Document6 pages2020 Yr 12 Mathematics Extension 2 Task 1 Term 42019 V2Jason Wenxuan MIAONo ratings yet

- TPS JD - Big Data Analyst (Python)Document2 pagesTPS JD - Big Data Analyst (Python)Mark Jayson P. DomaNo ratings yet

- FT Facebook AppsDocument97 pagesFT Facebook Appsfunforfunny25No ratings yet

- Manual para Uso Del Sistema OperaDocument144 pagesManual para Uso Del Sistema Operadanarg2286No ratings yet

- Softmart EndUser PricelistDocument59 pagesSoftmart EndUser PricelistSuvashreePradhanNo ratings yet

- IS 6533 Part 1 1989 Code of Practice For Design and Construction of Steel Chimneys Part 1 Mechanical Aspects)Document23 pagesIS 6533 Part 1 1989 Code of Practice For Design and Construction of Steel Chimneys Part 1 Mechanical Aspects)bbaplNo ratings yet

- Ecommerce WebsiteDocument49 pagesEcommerce WebsiteMonsta X100% (1)

- 7.3.7 Lab - View The Switch Mac Address TableDocument4 pages7.3.7 Lab - View The Switch Mac Address TableHenry Mejia ZuluagaNo ratings yet

- Nec Expresscluster X R3 Lan & Wan With Microsoft SQL Server Installation GuideDocument132 pagesNec Expresscluster X R3 Lan & Wan With Microsoft SQL Server Installation GuideMohammed AbdelrahmanNo ratings yet

- AzureDocument3 pagesAzureManjuNo ratings yet

- Galgotias College of Engineering & Technology: 1, Knowledge Park-II, Greater NoidaDocument5 pagesGalgotias College of Engineering & Technology: 1, Knowledge Park-II, Greater NoidaAshish yadavNo ratings yet

- Adani 2017-18 - PrintedDocument92 pagesAdani 2017-18 - PrintedDhanoob SureshkumarNo ratings yet

- Rslogix 5000 Fuzzydesigner: Installation GuideDocument8 pagesRslogix 5000 Fuzzydesigner: Installation GuideItachi UchihaNo ratings yet

- Qualified Vendors List (QVL), Model Name: X299X AORUS MASTERDocument9 pagesQualified Vendors List (QVL), Model Name: X299X AORUS MASTERMike ChromeNo ratings yet

- Splitter LogDocument1 pageSplitter LogTalhaNo ratings yet

- KR C4 Na: ControllerDocument185 pagesKR C4 Na: ControllerAndrea DoriaNo ratings yet

- ConfigurationDocument28 pagesConfigurationMohamed ShabanaNo ratings yet

- MSP Extension Cover Letter SampleDocument6 pagesMSP Extension Cover Letter Samplef5dct2q8100% (2)

- QuickRide LogcatDocument231 pagesQuickRide Logcatanirudha joshiNo ratings yet

- Augmentation ResearchDocument4 pagesAugmentation ResearchPrasadNo ratings yet

- Dbms NotesDocument9 pagesDbms NotesRitik PantNo ratings yet

- Desigo CC Brochure 040512Document10 pagesDesigo CC Brochure 040512anon_666806471No ratings yet

- The Song of Twilight - Yoshinao Nakada Sheet Music For Piano (Solo)Document1 pageThe Song of Twilight - Yoshinao Nakada Sheet Music For Piano (Solo)Dorotea GavrilNo ratings yet

- 027e89cb1bce9-Bar Graphs Worksheet-1 27 Apr 2024Document8 pages027e89cb1bce9-Bar Graphs Worksheet-1 27 Apr 2024aakangshaharsanaNo ratings yet

- MITSUBISHI FR CS80 Instruction ManualDocument246 pagesMITSUBISHI FR CS80 Instruction ManualLaurentiu LapusescuNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Study Guide: Certified Information Systems Security OfficerDocument33 pagesStudy Guide: Certified Information Systems Security Officerellococareloco100% (1)

- CISSP - 1 Information Security & Risk ManagementDocument60 pagesCISSP - 1 Information Security & Risk ManagementlebenikosNo ratings yet

- Information Security Governance and Risk ManagementDocument6 pagesInformation Security Governance and Risk Managementjbrackett239No ratings yet

- Risk Management 1Document41 pagesRisk Management 1Amit Agarwal100% (2)

- CC7178 Cyber Security Management: Presenter: Kiran Kumar ShahDocument31 pagesCC7178 Cyber Security Management: Presenter: Kiran Kumar ShahManish SharmaNo ratings yet

- Risk Management: Predict - Preempt - ProtectDocument31 pagesRisk Management: Predict - Preempt - ProtectFerry100% (2)

- Information Security Governance and RiskDocument26 pagesInformation Security Governance and RiskSakil MahmudNo ratings yet

- Information Security Risk AnalysisDocument42 pagesInformation Security Risk AnalysisRishabh kapoorNo ratings yet

- Cisa Notes 2010Document26 pagesCisa Notes 2010Amanda Christine WijayaNo ratings yet

- Module 4 Ias321 Risk ManagementDocument12 pagesModule 4 Ias321 Risk ManagementMALLARI, HANNAH M.No ratings yet

- CSSLP 2016 NotesDocument26 pagesCSSLP 2016 Notesparul154No ratings yet

- Information Risk ManagementDocument30 pagesInformation Risk ManagementPukhrajNo ratings yet

- Risk Management-Assessing and Controlling RisksDocument43 pagesRisk Management-Assessing and Controlling RisksEswin AngelNo ratings yet

- A719552767 - 24968 - 24 - 2019 - ppt4 Info RiskDocument30 pagesA719552767 - 24968 - 24 - 2019 - ppt4 Info RiskVinay Singh Bittu100% (1)

- CISSP 8 DomainsDocument508 pagesCISSP 8 DomainsAntonio Galvez100% (10)

- "Risks in Information System ": Prepared By: Manoj Kumar Attri 23-MBA-2011Document26 pages"Risks in Information System ": Prepared By: Manoj Kumar Attri 23-MBA-2011Amit Pal SinghNo ratings yet

- IRM Lecture 6 - Information Security and Risk ManagementDocument7 pagesIRM Lecture 6 - Information Security and Risk ManagementLimberto SuarezNo ratings yet

- 304 SlideDocument46 pages304 SlidejavabeanNo ratings yet

- Isaa 2Document31 pagesIsaa 2rishabh agrawalNo ratings yet

- NIST SP800-30 Approach To Risk AssessmentDocument6 pagesNIST SP800-30 Approach To Risk AssessmentBabby BossNo ratings yet

- Informtion Risk ManagementDocument54 pagesInformtion Risk ManagementMuhammad IbrahimNo ratings yet

- Information Risk ManagementDocument29 pagesInformation Risk ManagementAnas Inam100% (1)

- Information Security Risk AnalysisDocument27 pagesInformation Security Risk AnalysisMahesh SinghNo ratings yet

- Risk Management: ISEC 4340Document166 pagesRisk Management: ISEC 4340يُ يَNo ratings yet

- Risk Analysis Nina GodboleDocument23 pagesRisk Analysis Nina GodboleRupesh AkulaNo ratings yet

- Unit 3 - Threat ModellingDocument13 pagesUnit 3 - Threat ModellingNivedhithaNo ratings yet

- CHAP 3 RM PROCESS ModifiedDocument36 pagesCHAP 3 RM PROCESS ModifiedhaiqalNo ratings yet

- ISA1 Module2Topic5Document67 pagesISA1 Module2Topic5サカイ アルジェイNo ratings yet

- FALLSEM2020-21 CSE3501 ETH VL2020210102645 Reference Material I 08-Sep-2020 Risk Management - V2Document171 pagesFALLSEM2020-21 CSE3501 ETH VL2020210102645 Reference Material I 08-Sep-2020 Risk Management - V2Game CrewNo ratings yet

- Incident ManagementDocument18 pagesIncident ManagementBalan Wv100% (1)

- Week 6 Risk Assessment and Analysis Part 1 2Document55 pagesWeek 6 Risk Assessment and Analysis Part 1 2Very danggerNo ratings yet

- Module-5: Risk Assessment & Configuration ReviewDocument28 pagesModule-5: Risk Assessment & Configuration ReviewAdityaNo ratings yet

- Day 7Document29 pagesDay 7scosee171No ratings yet

- Week 2 - Risk AssessmentDocument35 pagesWeek 2 - Risk AssessmentTahir BashirNo ratings yet

- Assignment Risk ManagementDocument5 pagesAssignment Risk ManagementHimanshu JainNo ratings yet

- Week 11Document55 pagesWeek 11rajnipriya0101No ratings yet

- Risk Assessment Frameworks: Rodney Petersen Government Relations Officer Security Task Force Coordinator EducauseDocument23 pagesRisk Assessment Frameworks: Rodney Petersen Government Relations Officer Security Task Force Coordinator EducausePiyush GuptaNo ratings yet

- Chapter 789101112Document54 pagesChapter 789101112Nasis DerejeNo ratings yet

- Manage Risk OMDocument2 pagesManage Risk OMVivek VashisthaNo ratings yet

- CISSP - 1 Information Security & Risk ManagementDocument60 pagesCISSP - 1 Information Security & Risk Managementjonty509No ratings yet

- Incident Management:-An Incident Is An Event That Could Lead To Loss Of, or Disruption To, AnDocument19 pagesIncident Management:-An Incident Is An Event That Could Lead To Loss Of, or Disruption To, Anjasmeet SinghNo ratings yet

- Risk Management (Cont'd)Document28 pagesRisk Management (Cont'd)Umar FarooqNo ratings yet

- Ch-05 Risk Management Tools and TechniquesDocument37 pagesCh-05 Risk Management Tools and TechniquesaafnanNo ratings yet

- Risk AssessmentDocument26 pagesRisk AssessmentANIRUDH B K 19BIT0348No ratings yet

- Important Definations - Risk ManagmentDocument11 pagesImportant Definations - Risk ManagmentomerNo ratings yet

- Risk Assessment: - By: Dedy Syamsuar, PHDDocument29 pagesRisk Assessment: - By: Dedy Syamsuar, PHDIstiarso BudiyuwonoNo ratings yet

- Comparison Between ISO 27005Document6 pagesComparison Between ISO 27005Indrian WahyudiNo ratings yet

- TQM, Lecture-11+12Document18 pagesTQM, Lecture-11+12Shakeel AhmadNo ratings yet

- Performing A Risk Assessment: Flourensia Sapty Rahayu S.T., M.KomDocument23 pagesPerforming A Risk Assessment: Flourensia Sapty Rahayu S.T., M.KomArinisa PakpahanNo ratings yet

- Lecture 5-White Board-20Dec2020Document12 pagesLecture 5-White Board-20Dec2020Plus PlusNo ratings yet

- Understanding Risk and Risk ManagementDocument30 pagesUnderstanding Risk and Risk ManagementSemargarengpetrukbagNo ratings yet

- Four Principles of ORM: Operational Risk Risk Human FactorsDocument10 pagesFour Principles of ORM: Operational Risk Risk Human FactorsivymaryNo ratings yet

- CISM 15e Domain2 New FormatDocument123 pagesCISM 15e Domain2 New Formatmrsph07No ratings yet

- Unit I Security Risk Assessment and ManagementDocument32 pagesUnit I Security Risk Assessment and ManagementShifa Khan100% (1)

- COSO FrameworkDocument47 pagesCOSO FrameworkMathew P. VargheseNo ratings yet

- ALS Limited Risk Management Policy and FrameworkDocument13 pagesALS Limited Risk Management Policy and FrameworkSyed Kashif AliNo ratings yet

- CH 04Document59 pagesCH 04faisal_cseduNo ratings yet

- CISA Exam-Testing Concept-Knowledge of Risk AssessmentFrom EverandCISA Exam-Testing Concept-Knowledge of Risk AssessmentRating: 2.5 out of 5 stars2.5/5 (4)

- CINS - 3044 - SAMPLE - SYLLABUS - CINS 3044-40277 FALL 2018.pdf. - 19-31-01 - 1-12-49pm - CINS 3044-40277 FALL 2018Document8 pagesCINS - 3044 - SAMPLE - SYLLABUS - CINS 3044-40277 FALL 2018.pdf. - 19-31-01 - 1-12-49pm - CINS 3044-40277 FALL 2018Naveed RiazNo ratings yet

- Topic 12Document36 pagesTopic 12Naveed RiazNo ratings yet

- Topic 5 - 2Document23 pagesTopic 5 - 2Naveed RiazNo ratings yet

- Topic 4 - 1Document23 pagesTopic 4 - 1Naveed RiazNo ratings yet

- L764000-XG11-00-CKL-150001 - FDS For PSS - RevGDocument104 pagesL764000-XG11-00-CKL-150001 - FDS For PSS - RevGAshok NavalNo ratings yet

- Section 5: Data Structures & AlgorithmsDocument12 pagesSection 5: Data Structures & AlgorithmsYT PremoneNo ratings yet

- Multimedia Presentation RubricDocument3 pagesMultimedia Presentation RubricMIKKIENNANo ratings yet

- PLC Motor LogicDocument5 pagesPLC Motor LogicInstrumentation ToolsNo ratings yet

- Org Four: Int 21H and INT 10H Programming and MacrosDocument31 pagesOrg Four: Int 21H and INT 10H Programming and MacrosBuket CüvelenkNo ratings yet

- 2020 Yr 12 Mathematics Extension 2 Task 1 Term 42019 V2Document6 pages2020 Yr 12 Mathematics Extension 2 Task 1 Term 42019 V2Jason Wenxuan MIAONo ratings yet

- TPS JD - Big Data Analyst (Python)Document2 pagesTPS JD - Big Data Analyst (Python)Mark Jayson P. DomaNo ratings yet

- FT Facebook AppsDocument97 pagesFT Facebook Appsfunforfunny25No ratings yet

- Manual para Uso Del Sistema OperaDocument144 pagesManual para Uso Del Sistema Operadanarg2286No ratings yet

- Softmart EndUser PricelistDocument59 pagesSoftmart EndUser PricelistSuvashreePradhanNo ratings yet

- IS 6533 Part 1 1989 Code of Practice For Design and Construction of Steel Chimneys Part 1 Mechanical Aspects)Document23 pagesIS 6533 Part 1 1989 Code of Practice For Design and Construction of Steel Chimneys Part 1 Mechanical Aspects)bbaplNo ratings yet

- Ecommerce WebsiteDocument49 pagesEcommerce WebsiteMonsta X100% (1)

- 7.3.7 Lab - View The Switch Mac Address TableDocument4 pages7.3.7 Lab - View The Switch Mac Address TableHenry Mejia ZuluagaNo ratings yet

- Nec Expresscluster X R3 Lan & Wan With Microsoft SQL Server Installation GuideDocument132 pagesNec Expresscluster X R3 Lan & Wan With Microsoft SQL Server Installation GuideMohammed AbdelrahmanNo ratings yet

- AzureDocument3 pagesAzureManjuNo ratings yet

- Galgotias College of Engineering & Technology: 1, Knowledge Park-II, Greater NoidaDocument5 pagesGalgotias College of Engineering & Technology: 1, Knowledge Park-II, Greater NoidaAshish yadavNo ratings yet

- Adani 2017-18 - PrintedDocument92 pagesAdani 2017-18 - PrintedDhanoob SureshkumarNo ratings yet

- Rslogix 5000 Fuzzydesigner: Installation GuideDocument8 pagesRslogix 5000 Fuzzydesigner: Installation GuideItachi UchihaNo ratings yet

- Qualified Vendors List (QVL), Model Name: X299X AORUS MASTERDocument9 pagesQualified Vendors List (QVL), Model Name: X299X AORUS MASTERMike ChromeNo ratings yet

- Splitter LogDocument1 pageSplitter LogTalhaNo ratings yet

- KR C4 Na: ControllerDocument185 pagesKR C4 Na: ControllerAndrea DoriaNo ratings yet

- ConfigurationDocument28 pagesConfigurationMohamed ShabanaNo ratings yet

- MSP Extension Cover Letter SampleDocument6 pagesMSP Extension Cover Letter Samplef5dct2q8100% (2)

- QuickRide LogcatDocument231 pagesQuickRide Logcatanirudha joshiNo ratings yet

- Augmentation ResearchDocument4 pagesAugmentation ResearchPrasadNo ratings yet

- Dbms NotesDocument9 pagesDbms NotesRitik PantNo ratings yet

- Desigo CC Brochure 040512Document10 pagesDesigo CC Brochure 040512anon_666806471No ratings yet

- The Song of Twilight - Yoshinao Nakada Sheet Music For Piano (Solo)Document1 pageThe Song of Twilight - Yoshinao Nakada Sheet Music For Piano (Solo)Dorotea GavrilNo ratings yet

- 027e89cb1bce9-Bar Graphs Worksheet-1 27 Apr 2024Document8 pages027e89cb1bce9-Bar Graphs Worksheet-1 27 Apr 2024aakangshaharsanaNo ratings yet

- MITSUBISHI FR CS80 Instruction ManualDocument246 pagesMITSUBISHI FR CS80 Instruction ManualLaurentiu LapusescuNo ratings yet