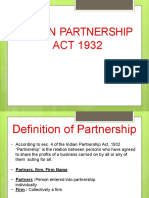

8 - Partnership Act

8 - Partnership Act

You might also like

- MBA 620 Week 3 HW SolutionsDocument5 pagesMBA 620 Week 3 HW SolutionsphoebeNo ratings yet

- Financial Acc, Partnership Acc Assignment 2Document17 pagesFinancial Acc, Partnership Acc Assignment 2Haroon Khan100% (1)

- Business Legal Forms of OwnershipDocument44 pagesBusiness Legal Forms of OwnershipNecie Nilugao Rodriguez100% (1)

- LevendaryDocument9 pagesLevendarySaurabhNo ratings yet

- Expressway Project Finance Task 4A (Avinash Singh)Document9 pagesExpressway Project Finance Task 4A (Avinash Singh)avinash singh100% (2)

- E-Commerce Start-Up Business PlanDocument45 pagesE-Commerce Start-Up Business PlanKhilesh Bharambe100% (4)

- 9 - Companies ActDocument58 pages9 - Companies Actbisma irfanNo ratings yet

- Dissolution of A Partnership FirmDocument14 pagesDissolution of A Partnership Firmrose rose100% (1)

- DevaangDev Sem4 CommercialLaw RegistrationOfFirmDocument12 pagesDevaangDev Sem4 CommercialLaw RegistrationOfFirmDeeveegeeNo ratings yet

- Partnership KarwanDocument7 pagesPartnership KarwanReving DuskiNo ratings yet

- XII Accountancy Notes All Chapters MR - Mohan H BaksaniDocument176 pagesXII Accountancy Notes All Chapters MR - Mohan H BaksaniALAY SINGHNo ratings yet

- Business LawDocument9 pagesBusiness Lawghoshsunny294No ratings yet

- Module 13 in Tourism LawDocument2 pagesModule 13 in Tourism LawJennifer Sisperez Buraga-Waña LptNo ratings yet

- Forms of Business OwnershipDocument20 pagesForms of Business OwnershipFahim AhmedNo ratings yet

- PA2C4 Pship NACFNDocument26 pagesPA2C4 Pship NACFNSelamNo ratings yet

- Laws Governing Business Structures: Dr. Bharat ChillakuriDocument24 pagesLaws Governing Business Structures: Dr. Bharat ChillakuriRishiraj SinghNo ratings yet

- Chapter 10 - Company FormationDocument11 pagesChapter 10 - Company FormationK59 Vo Doan Hoang AnhNo ratings yet

- ADV Accounting IIDocument177 pagesADV Accounting IIbrook buta100% (1)

- Legal Entities With BanksDocument115 pagesLegal Entities With Bankstasnim farooquiNo ratings yet

- Business Law ProjectDocument31 pagesBusiness Law ProjectMesSum HusnaiNNo ratings yet

- Partnership FirmDocument9 pagesPartnership FirmLowlyLutfur100% (1)

- Unit-17 Assessment of FirmDocument51 pagesUnit-17 Assessment of FirmRohit SinghNo ratings yet

- Indian Partnership ActDocument24 pagesIndian Partnership ActAditya AgrawalNo ratings yet

- Unit 17Document51 pagesUnit 17Awesome AngelNo ratings yet

- Advacc 1Document11 pagesAdvacc 1Jasmine PeraltaNo ratings yet

- Business Entities Exam Preparation-1Document59 pagesBusiness Entities Exam Preparation-1Veronika Shangeelao KaxwekaNo ratings yet

- Answer 1Document6 pagesAnswer 1Hezekiah AtindaNo ratings yet

- Advanced Accounting Unit 5Document42 pagesAdvanced Accounting Unit 5mubarek oumerNo ratings yet

- Book Keeping & AccountancyDocument24 pagesBook Keeping & AccountancyElvita Pinto100% (1)

- Mid-2 NCHDocument52 pagesMid-2 NCHKarthikNo ratings yet

- 4 Partnership LawDocument8 pages4 Partnership LawVaibhav AgarwalNo ratings yet

- Choosing A Form of Ownership: Lecture: Sana Munir UETDocument39 pagesChoosing A Form of Ownership: Lecture: Sana Munir UETMuhammad SameerNo ratings yet

- Business Forms 2Document7 pagesBusiness Forms 2Wamema joshuaNo ratings yet

- Chapter - 5 Legal Forms of Business OwnershipDocument19 pagesChapter - 5 Legal Forms of Business OwnershipmohammedkasoNo ratings yet

- Topic 8Document22 pagesTopic 8Victor AjraebrillNo ratings yet

- 4 Forms of Business Organizations 5 PagesDocument5 pages4 Forms of Business Organizations 5 PagesSujd HesjjfgsNo ratings yet

- Nayve, Kimberly IDocument113 pagesNayve, Kimberly IKim Nayve50% (10)

- Comparative Study of A Company and A PartnershipDocument7 pagesComparative Study of A Company and A PartnershipNandini BansalNo ratings yet

- Prelims Reviewer in Partnership and Corporation (FAR II)Document6 pagesPrelims Reviewer in Partnership and Corporation (FAR II)Belle TacuyanNo ratings yet

- Forms of Business OrganizationsDocument16 pagesForms of Business Organizationsjewren_159No ratings yet

- Steps in Incorporation of A CompanyDocument7 pagesSteps in Incorporation of A CompanyJayesh RajputNo ratings yet

- Mehak B.law 3rd AssignmentDocument10 pagesMehak B.law 3rd AssignmentWazeeer AhmadNo ratings yet

- Lecture 6Document18 pagesLecture 6sjalalisNo ratings yet

- UNIT 18 Company LawDocument14 pagesUNIT 18 Company LawRaven471No ratings yet

- 001 PartnershipDocument40 pages001 PartnershipbhattiafsaNo ratings yet

- BPPTDocument11 pagesBPPTkishore ortanNo ratings yet

- Parnership ActDocument28 pagesParnership ActKruti BhattNo ratings yet

- Advance Chapter OneDocument42 pagesAdvance Chapter OneSolomon Abebe100% (4)

- Meaning & Formation of CompanyDocument21 pagesMeaning & Formation of Companysmsmba67% (3)

- CHAPTER 12 Partnerships Basic Considerations and FormationsDocument9 pagesCHAPTER 12 Partnerships Basic Considerations and FormationsGabrielle Joshebed AbaricoNo ratings yet

- Business Organisation and Structure Unit 2Document59 pagesBusiness Organisation and Structure Unit 2pragnesh dholakiaNo ratings yet

- PartnershipDocument19 pagesPartnershipwijerathnadilmiNo ratings yet

- Concept of PartnershipDocument6 pagesConcept of PartnershipShweta AgrawalNo ratings yet

- Business Law PresentationDocument25 pagesBusiness Law PresentationFabia ArshadNo ratings yet

- 5-Contract of AgencyDocument34 pages5-Contract of Agencybisma irfanNo ratings yet

- FINAL Exam Revision QuestionsDocument10 pagesFINAL Exam Revision QuestionsĐào ĐăngNo ratings yet

- Accounting For Partnership-FinalDocument14 pagesAccounting For Partnership-Finalgetnet5195No ratings yet

- FINAL Exam - Revision QuestionsDocument10 pagesFINAL Exam - Revision QuestionsĐào ĐăngNo ratings yet

- PartnershipDocument23 pagesPartnershipathulkannanNo ratings yet

- PartnershipDocument6 pagesPartnershipCristina ClemensoNo ratings yet

- Law of Partnership (Business Law)Document8 pagesLaw of Partnership (Business Law)Sajib AliNo ratings yet

- Special Contract / Contract of Agency Page 133-147: Accounting and Finance Faculty - (Business Law and Taxation Team)Document34 pagesSpecial Contract / Contract of Agency Page 133-147: Accounting and Finance Faculty - (Business Law and Taxation Team)fayaz khanNo ratings yet

- Partnership Chapter 2Document6 pagesPartnership Chapter 2Nyah MallariNo ratings yet

- Canadian Equine Law: A Guide For Anyone Working With Horses In CanadaFrom EverandCanadian Equine Law: A Guide For Anyone Working With Horses In CanadaNo ratings yet

- Decline ThesisDocument3 pagesDecline ThesisMaya Singh67% (3)

- Southern Automobiles LTD.: CNG Station, Dhaka Daily Sales Statement (Shift Wise)Document1 pageSouthern Automobiles LTD.: CNG Station, Dhaka Daily Sales Statement (Shift Wise)Arpita NandiNo ratings yet

- Vietnam Table Mounted Water Purifiers Market, Forecast and Opportunities, 2030 - Updated ReportDocument77 pagesVietnam Table Mounted Water Purifiers Market, Forecast and Opportunities, 2030 - Updated ReportTuan Anh DuongNo ratings yet

- New Dealer Account ApplicationDocument2 pagesNew Dealer Account ApplicationCarol Joy PorrasNo ratings yet

- Human Resource Accounting Human Resource Accounting: Dhananjaya (A2)Document16 pagesHuman Resource Accounting Human Resource Accounting: Dhananjaya (A2)Raghu pokakaNo ratings yet

- CMA DataDocument35 pagesCMA Dataashishy99No ratings yet

- Assessment of Working CapitalDocument72 pagesAssessment of Working Capitaladil sheikhNo ratings yet

- CT MAF251 Q OCT2023 NopasswordDocument3 pagesCT MAF251 Q OCT2023 Nopassword2022890872No ratings yet

- Iim Indore: Final Placement Report 2011 - 2013Document5 pagesIim Indore: Final Placement Report 2011 - 2013Abdal LalitNo ratings yet

- PHD Corp Fin Syllabus - 2015 PDFDocument11 pagesPHD Corp Fin Syllabus - 2015 PDFMacarenaAntonioNo ratings yet

- Case Study in Revenue Management For Youth HostelsDocument6 pagesCase Study in Revenue Management For Youth HostelsSujay Vikram SinghNo ratings yet

- 5 Real Property Tax Proclamation (Draft)Document35 pages5 Real Property Tax Proclamation (Draft)Fehim Seid92% (12)

- Business Forecasting PDFDocument296 pagesBusiness Forecasting PDFSachin Chaudhari100% (1)

- Small Hydropower in AfricaDocument2 pagesSmall Hydropower in AfricawklunneNo ratings yet

- Demand-Side Analysis of Access To Financial Services For Businesses in Zambia - ZBS July 2010Document56 pagesDemand-Side Analysis of Access To Financial Services For Businesses in Zambia - ZBS July 2010Chola MukangaNo ratings yet

- 295 - Interim Payment Certificate No.13 For The Month of November - 2021.Document4 pages295 - Interim Payment Certificate No.13 For The Month of November - 2021.ceku4iroad2No ratings yet

- Introduction To Securities and InvestmentDocument26 pagesIntroduction To Securities and InvestmentJerome GaliciaNo ratings yet

- VEP - A.T. Kearney 2003Document48 pagesVEP - A.T. Kearney 2003punit_sonikaNo ratings yet

- Unit 02 HRM and Personnel ManagementDocument11 pagesUnit 02 HRM and Personnel Managementkhaled ShojiveNo ratings yet

- Revealing The ValueDocument9 pagesRevealing The ValueHaVinhDuyNo ratings yet

- EFFECTS OF INTERNAL CONTROL SYSTEMS ON FINANCIAL PERFORMANCE IN AN INSTITUTION OF HIGHER LEARNING IN UGANDA - Lay Bien The Che Chinh TriDocument95 pagesEFFECTS OF INTERNAL CONTROL SYSTEMS ON FINANCIAL PERFORMANCE IN AN INSTITUTION OF HIGHER LEARNING IN UGANDA - Lay Bien The Che Chinh TriHoang QuanNo ratings yet

- Operations Management Assignment Starbucks CorporationDocument5 pagesOperations Management Assignment Starbucks CorporationPRIYANSHA GARGNo ratings yet

- Customer Satisfaction Towards Lic Housing FinancDocument69 pagesCustomer Satisfaction Towards Lic Housing Financboss_144569224100% (1)

- Futures: Distinction in Between Futures Contract and Forward ContractDocument85 pagesFutures: Distinction in Between Futures Contract and Forward ContractRDHNo ratings yet

- Ano Ang Structural Mitigation at Non Structural Mitigatio1Document4 pagesAno Ang Structural Mitigation at Non Structural Mitigatio1sean ollerNo ratings yet

- Od 327194816997610100Document1 pageOd 327194816997610100aradhnag878No ratings yet

Download as pptx, pdf, or txt

You might also like

- MBA 620 Week 3 HW SolutionsDocument5 pagesMBA 620 Week 3 HW SolutionsphoebeNo ratings yet

- Financial Acc, Partnership Acc Assignment 2Document17 pagesFinancial Acc, Partnership Acc Assignment 2Haroon Khan100% (1)

- Business Legal Forms of OwnershipDocument44 pagesBusiness Legal Forms of OwnershipNecie Nilugao Rodriguez100% (1)

- LevendaryDocument9 pagesLevendarySaurabhNo ratings yet

- Expressway Project Finance Task 4A (Avinash Singh)Document9 pagesExpressway Project Finance Task 4A (Avinash Singh)avinash singh100% (2)

- E-Commerce Start-Up Business PlanDocument45 pagesE-Commerce Start-Up Business PlanKhilesh Bharambe100% (4)

- 9 - Companies ActDocument58 pages9 - Companies Actbisma irfanNo ratings yet

- Dissolution of A Partnership FirmDocument14 pagesDissolution of A Partnership Firmrose rose100% (1)

- DevaangDev Sem4 CommercialLaw RegistrationOfFirmDocument12 pagesDevaangDev Sem4 CommercialLaw RegistrationOfFirmDeeveegeeNo ratings yet

- Partnership KarwanDocument7 pagesPartnership KarwanReving DuskiNo ratings yet

- XII Accountancy Notes All Chapters MR - Mohan H BaksaniDocument176 pagesXII Accountancy Notes All Chapters MR - Mohan H BaksaniALAY SINGHNo ratings yet

- Business LawDocument9 pagesBusiness Lawghoshsunny294No ratings yet

- Module 13 in Tourism LawDocument2 pagesModule 13 in Tourism LawJennifer Sisperez Buraga-Waña LptNo ratings yet

- Forms of Business OwnershipDocument20 pagesForms of Business OwnershipFahim AhmedNo ratings yet

- PA2C4 Pship NACFNDocument26 pagesPA2C4 Pship NACFNSelamNo ratings yet

- Laws Governing Business Structures: Dr. Bharat ChillakuriDocument24 pagesLaws Governing Business Structures: Dr. Bharat ChillakuriRishiraj SinghNo ratings yet

- Chapter 10 - Company FormationDocument11 pagesChapter 10 - Company FormationK59 Vo Doan Hoang AnhNo ratings yet

- ADV Accounting IIDocument177 pagesADV Accounting IIbrook buta100% (1)

- Legal Entities With BanksDocument115 pagesLegal Entities With Bankstasnim farooquiNo ratings yet

- Business Law ProjectDocument31 pagesBusiness Law ProjectMesSum HusnaiNNo ratings yet

- Partnership FirmDocument9 pagesPartnership FirmLowlyLutfur100% (1)

- Unit-17 Assessment of FirmDocument51 pagesUnit-17 Assessment of FirmRohit SinghNo ratings yet

- Indian Partnership ActDocument24 pagesIndian Partnership ActAditya AgrawalNo ratings yet

- Unit 17Document51 pagesUnit 17Awesome AngelNo ratings yet

- Advacc 1Document11 pagesAdvacc 1Jasmine PeraltaNo ratings yet

- Business Entities Exam Preparation-1Document59 pagesBusiness Entities Exam Preparation-1Veronika Shangeelao KaxwekaNo ratings yet

- Answer 1Document6 pagesAnswer 1Hezekiah AtindaNo ratings yet

- Advanced Accounting Unit 5Document42 pagesAdvanced Accounting Unit 5mubarek oumerNo ratings yet

- Book Keeping & AccountancyDocument24 pagesBook Keeping & AccountancyElvita Pinto100% (1)

- Mid-2 NCHDocument52 pagesMid-2 NCHKarthikNo ratings yet

- 4 Partnership LawDocument8 pages4 Partnership LawVaibhav AgarwalNo ratings yet

- Choosing A Form of Ownership: Lecture: Sana Munir UETDocument39 pagesChoosing A Form of Ownership: Lecture: Sana Munir UETMuhammad SameerNo ratings yet

- Business Forms 2Document7 pagesBusiness Forms 2Wamema joshuaNo ratings yet

- Chapter - 5 Legal Forms of Business OwnershipDocument19 pagesChapter - 5 Legal Forms of Business OwnershipmohammedkasoNo ratings yet

- Topic 8Document22 pagesTopic 8Victor AjraebrillNo ratings yet

- 4 Forms of Business Organizations 5 PagesDocument5 pages4 Forms of Business Organizations 5 PagesSujd HesjjfgsNo ratings yet

- Nayve, Kimberly IDocument113 pagesNayve, Kimberly IKim Nayve50% (10)

- Comparative Study of A Company and A PartnershipDocument7 pagesComparative Study of A Company and A PartnershipNandini BansalNo ratings yet

- Prelims Reviewer in Partnership and Corporation (FAR II)Document6 pagesPrelims Reviewer in Partnership and Corporation (FAR II)Belle TacuyanNo ratings yet

- Forms of Business OrganizationsDocument16 pagesForms of Business Organizationsjewren_159No ratings yet

- Steps in Incorporation of A CompanyDocument7 pagesSteps in Incorporation of A CompanyJayesh RajputNo ratings yet

- Mehak B.law 3rd AssignmentDocument10 pagesMehak B.law 3rd AssignmentWazeeer AhmadNo ratings yet

- Lecture 6Document18 pagesLecture 6sjalalisNo ratings yet

- UNIT 18 Company LawDocument14 pagesUNIT 18 Company LawRaven471No ratings yet

- 001 PartnershipDocument40 pages001 PartnershipbhattiafsaNo ratings yet

- BPPTDocument11 pagesBPPTkishore ortanNo ratings yet

- Parnership ActDocument28 pagesParnership ActKruti BhattNo ratings yet

- Advance Chapter OneDocument42 pagesAdvance Chapter OneSolomon Abebe100% (4)

- Meaning & Formation of CompanyDocument21 pagesMeaning & Formation of Companysmsmba67% (3)

- CHAPTER 12 Partnerships Basic Considerations and FormationsDocument9 pagesCHAPTER 12 Partnerships Basic Considerations and FormationsGabrielle Joshebed AbaricoNo ratings yet

- Business Organisation and Structure Unit 2Document59 pagesBusiness Organisation and Structure Unit 2pragnesh dholakiaNo ratings yet

- PartnershipDocument19 pagesPartnershipwijerathnadilmiNo ratings yet

- Concept of PartnershipDocument6 pagesConcept of PartnershipShweta AgrawalNo ratings yet

- Business Law PresentationDocument25 pagesBusiness Law PresentationFabia ArshadNo ratings yet

- 5-Contract of AgencyDocument34 pages5-Contract of Agencybisma irfanNo ratings yet

- FINAL Exam Revision QuestionsDocument10 pagesFINAL Exam Revision QuestionsĐào ĐăngNo ratings yet

- Accounting For Partnership-FinalDocument14 pagesAccounting For Partnership-Finalgetnet5195No ratings yet

- FINAL Exam - Revision QuestionsDocument10 pagesFINAL Exam - Revision QuestionsĐào ĐăngNo ratings yet

- PartnershipDocument23 pagesPartnershipathulkannanNo ratings yet

- PartnershipDocument6 pagesPartnershipCristina ClemensoNo ratings yet

- Law of Partnership (Business Law)Document8 pagesLaw of Partnership (Business Law)Sajib AliNo ratings yet

- Special Contract / Contract of Agency Page 133-147: Accounting and Finance Faculty - (Business Law and Taxation Team)Document34 pagesSpecial Contract / Contract of Agency Page 133-147: Accounting and Finance Faculty - (Business Law and Taxation Team)fayaz khanNo ratings yet

- Partnership Chapter 2Document6 pagesPartnership Chapter 2Nyah MallariNo ratings yet

- Canadian Equine Law: A Guide For Anyone Working With Horses In CanadaFrom EverandCanadian Equine Law: A Guide For Anyone Working With Horses In CanadaNo ratings yet

- Decline ThesisDocument3 pagesDecline ThesisMaya Singh67% (3)

- Southern Automobiles LTD.: CNG Station, Dhaka Daily Sales Statement (Shift Wise)Document1 pageSouthern Automobiles LTD.: CNG Station, Dhaka Daily Sales Statement (Shift Wise)Arpita NandiNo ratings yet

- Vietnam Table Mounted Water Purifiers Market, Forecast and Opportunities, 2030 - Updated ReportDocument77 pagesVietnam Table Mounted Water Purifiers Market, Forecast and Opportunities, 2030 - Updated ReportTuan Anh DuongNo ratings yet

- New Dealer Account ApplicationDocument2 pagesNew Dealer Account ApplicationCarol Joy PorrasNo ratings yet

- Human Resource Accounting Human Resource Accounting: Dhananjaya (A2)Document16 pagesHuman Resource Accounting Human Resource Accounting: Dhananjaya (A2)Raghu pokakaNo ratings yet

- CMA DataDocument35 pagesCMA Dataashishy99No ratings yet

- Assessment of Working CapitalDocument72 pagesAssessment of Working Capitaladil sheikhNo ratings yet

- CT MAF251 Q OCT2023 NopasswordDocument3 pagesCT MAF251 Q OCT2023 Nopassword2022890872No ratings yet

- Iim Indore: Final Placement Report 2011 - 2013Document5 pagesIim Indore: Final Placement Report 2011 - 2013Abdal LalitNo ratings yet

- PHD Corp Fin Syllabus - 2015 PDFDocument11 pagesPHD Corp Fin Syllabus - 2015 PDFMacarenaAntonioNo ratings yet

- Case Study in Revenue Management For Youth HostelsDocument6 pagesCase Study in Revenue Management For Youth HostelsSujay Vikram SinghNo ratings yet

- 5 Real Property Tax Proclamation (Draft)Document35 pages5 Real Property Tax Proclamation (Draft)Fehim Seid92% (12)

- Business Forecasting PDFDocument296 pagesBusiness Forecasting PDFSachin Chaudhari100% (1)

- Small Hydropower in AfricaDocument2 pagesSmall Hydropower in AfricawklunneNo ratings yet

- Demand-Side Analysis of Access To Financial Services For Businesses in Zambia - ZBS July 2010Document56 pagesDemand-Side Analysis of Access To Financial Services For Businesses in Zambia - ZBS July 2010Chola MukangaNo ratings yet

- 295 - Interim Payment Certificate No.13 For The Month of November - 2021.Document4 pages295 - Interim Payment Certificate No.13 For The Month of November - 2021.ceku4iroad2No ratings yet

- Introduction To Securities and InvestmentDocument26 pagesIntroduction To Securities and InvestmentJerome GaliciaNo ratings yet

- VEP - A.T. Kearney 2003Document48 pagesVEP - A.T. Kearney 2003punit_sonikaNo ratings yet

- Unit 02 HRM and Personnel ManagementDocument11 pagesUnit 02 HRM and Personnel Managementkhaled ShojiveNo ratings yet

- Revealing The ValueDocument9 pagesRevealing The ValueHaVinhDuyNo ratings yet

- EFFECTS OF INTERNAL CONTROL SYSTEMS ON FINANCIAL PERFORMANCE IN AN INSTITUTION OF HIGHER LEARNING IN UGANDA - Lay Bien The Che Chinh TriDocument95 pagesEFFECTS OF INTERNAL CONTROL SYSTEMS ON FINANCIAL PERFORMANCE IN AN INSTITUTION OF HIGHER LEARNING IN UGANDA - Lay Bien The Che Chinh TriHoang QuanNo ratings yet

- Operations Management Assignment Starbucks CorporationDocument5 pagesOperations Management Assignment Starbucks CorporationPRIYANSHA GARGNo ratings yet

- Customer Satisfaction Towards Lic Housing FinancDocument69 pagesCustomer Satisfaction Towards Lic Housing Financboss_144569224100% (1)

- Futures: Distinction in Between Futures Contract and Forward ContractDocument85 pagesFutures: Distinction in Between Futures Contract and Forward ContractRDHNo ratings yet

- Ano Ang Structural Mitigation at Non Structural Mitigatio1Document4 pagesAno Ang Structural Mitigation at Non Structural Mitigatio1sean ollerNo ratings yet

- Od 327194816997610100Document1 pageOd 327194816997610100aradhnag878No ratings yet