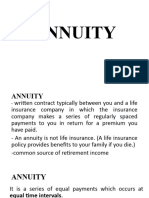

ORDINARY ANNUITY - Future and Present Value

ORDINARY ANNUITY - Future and Present Value

You might also like

- Engineering EconomyDocument159 pagesEngineering EconomyAlbert Aguilor88% (8)

- FNCE 623 Formulae For Mid Term ExamDocument3 pagesFNCE 623 Formulae For Mid Term Examleili fallahNo ratings yet

- Slm7 Present and Future Values 1Document18 pagesSlm7 Present and Future Values 1giovana therese duyapatNo ratings yet

- QuizDocument2 pagesQuizRepunzel RaajNo ratings yet

- TMV Solved ProblemDocument27 pagesTMV Solved ProblemIdrisNo ratings yet

- Annuity - Introduction Ordinary AnnuityDocument24 pagesAnnuity - Introduction Ordinary AnnuityThomasaquinos msigala JrNo ratings yet

- Simple AnnuityDocument22 pagesSimple AnnuityAshley AniganNo ratings yet

- Gen Math Q2 - Week 4 - General AnnuityDocument22 pagesGen Math Q2 - Week 4 - General AnnuityFrancisco, Ashley Dominique V.No ratings yet

- Module 7. Annuities: 1. Simple AnnuityDocument19 pagesModule 7. Annuities: 1. Simple AnnuityMori OugaiNo ratings yet

- Lecture9 - ES301 Engineering EconomicsDocument19 pagesLecture9 - ES301 Engineering EconomicsLory Liza Bulay-ogNo ratings yet

- FM CH - IiiDocument18 pagesFM CH - IiiGizaw BelayNo ratings yet

- MOI Midterm LessonDocument82 pagesMOI Midterm LessonPie CanapiNo ratings yet

- Basic QuantDocument12 pagesBasic Quantchickenmurgi365No ratings yet

- Genmath Q2 W3 4.1Document21 pagesGenmath Q2 W3 4.1Halloween NightNo ratings yet

- Financial Management Ch06Document52 pagesFinancial Management Ch06Muhammad Afnan MuammarNo ratings yet

- CHAPTER 4 Mathematics of FinanceDocument66 pagesCHAPTER 4 Mathematics of FinanceHailemariamNo ratings yet

- 15 AnnuitiesDocument28 pages15 AnnuitiesMahendra AvinashNo ratings yet

- 4 CHAPTER 4 Mathematics of Finance Short SlideDocument55 pages4 CHAPTER 4 Mathematics of Finance Short Slidevalenciawinno5No ratings yet

- Simple and General AnnuityDocument28 pagesSimple and General AnnuityLynn DomingoNo ratings yet

- General Mathematics 2nd Quarter Week 3 TERESA A. TACIS NHC HS NewDocument11 pagesGeneral Mathematics 2nd Quarter Week 3 TERESA A. TACIS NHC HS NewjohnNo ratings yet

- Time Value of MoneyDocument18 pagesTime Value of MoneyLatasha AdhiakriNo ratings yet

- General-Mathematics Simple-Annuity EDITEDDocument66 pagesGeneral-Mathematics Simple-Annuity EDITEDkcereban2021No ratings yet

- Define The Types of Annuities Overdue, Early, Differed, Undefined, Perpetual, General.Document19 pagesDefine The Types of Annuities Overdue, Early, Differed, Undefined, Perpetual, General.Fernando CooperNo ratings yet

- Annuities and Amortization: Classifications Formula Sample ProblemsDocument27 pagesAnnuities and Amortization: Classifications Formula Sample ProblemsMr.Clown 107No ratings yet

- ANNUITYDocument21 pagesANNUITYsuzhanearriba50No ratings yet

- Financial MGMT, Ch3Document29 pagesFinancial MGMT, Ch3heysemNo ratings yet

- TVM & CompoundingDocument8 pagesTVM & CompoundingUday BansalNo ratings yet

- Time Value of Money: Key PointsDocument5 pagesTime Value of Money: Key PointsUday BansalNo ratings yet

- General Mathematics: Quarter 2 - Module 6: Simple and Compound InterestsDocument22 pagesGeneral Mathematics: Quarter 2 - Module 6: Simple and Compound InterestsEldon Kim RaguindinNo ratings yet

- CE22 - 06 - Nominal Effective Interest RateDocument42 pagesCE22 - 06 - Nominal Effective Interest RateMarco ConopioNo ratings yet

- FM I CH IiiDocument8 pagesFM I CH IiiDùķe HPNo ratings yet

- Chapter 2 Money Time Relationships and Equivalence 2Document21 pagesChapter 2 Money Time Relationships and Equivalence 2Coreen ElizaldeNo ratings yet

- Module 3 Math1 Ge3Document10 pagesModule 3 Math1 Ge3orogrichchelynNo ratings yet

- Module 4 - BusimathDocument5 pagesModule 4 - BusimathAcelin Rayelle TULAGANNo ratings yet

- Simple and Compound Interest: Concept of Time and Value OfmoneyDocument11 pagesSimple and Compound Interest: Concept of Time and Value OfmoneyUnzila AtiqNo ratings yet

- Annuitie S: Liuren WuDocument39 pagesAnnuitie S: Liuren Wusaikumar selaNo ratings yet

- Consumer Mathematics: Gwendolyn TadeoDocument14 pagesConsumer Mathematics: Gwendolyn TadeoproximusNo ratings yet

- General Mathematics: Quarter 2 - Module 1 Simple and Compound InterestsDocument21 pagesGeneral Mathematics: Quarter 2 - Module 1 Simple and Compound InterestsThegame1991ususus100% (2)

- PEB4102 Chapter 4Document61 pagesPEB4102 Chapter 4LimNo ratings yet

- Assignment 1558589300 SmsDocument26 pagesAssignment 1558589300 Smspreciousfrancis365No ratings yet

- Module 3 Introduction To AnnuitiesDocument17 pagesModule 3 Introduction To AnnuitiesJenny AltazarNo ratings yet

- Ordinary Annuity and SuchDocument20 pagesOrdinary Annuity and SuchアゼロスレイゼルNo ratings yet

- Time Value of Money 1-1!1!044649Document67 pagesTime Value of Money 1-1!1!044649Yusuph HajiNo ratings yet

- Compound InterestDocument16 pagesCompound Interestv.garganera.551005No ratings yet

- Ch.4 Math of Finance-1Document19 pagesCh.4 Math of Finance-1hildamezmur9No ratings yet

- General Mathematics: Quarter 2 - Module 7 AnnuitiesDocument40 pagesGeneral Mathematics: Quarter 2 - Module 7 AnnuitiesBreanna CIel E. Cabahit100% (1)

- CUZ CORP FIN Time Value For Money-1Document16 pagesCUZ CORP FIN Time Value For Money-1KIMBERLY MUKAMBANo ratings yet

- Amortization and Sinking FundDocument16 pagesAmortization and Sinking FundRuthchel YaboNo ratings yet

- Simple AnnuityDocument28 pagesSimple AnnuityKelvin BarceLon33% (3)

- Topic 2 Principles of Money-Time RelationshipDocument28 pagesTopic 2 Principles of Money-Time RelationshipJeshua Llorera0% (1)

- Business Maths 1 Interest-1Document24 pagesBusiness Maths 1 Interest-1emmanuelifende1234No ratings yet

- Time Value of Money: Marios MavridesDocument35 pagesTime Value of Money: Marios Mavridesandreas panayiotouNo ratings yet

- Grade 11 Math MOd 6Document12 pagesGrade 11 Math MOd 6John Lois VanNo ratings yet

- Compound InterestDocument5 pagesCompound InterestLegaspi AllanNo ratings yet

- U N It: 7.0 Learning OutcomesDocument28 pagesU N It: 7.0 Learning Outcomesjokes & comedies onlyNo ratings yet

- Chapter 9: Mathematics of FinanceDocument55 pagesChapter 9: Mathematics of FinanceQuang PHAMNo ratings yet

- Mathematics of Investment Module 5Document4 pagesMathematics of Investment Module 5Kim JayNo ratings yet

- AnnuitiesDocument68 pagesAnnuitiesnimra khaliqNo ratings yet

- A. Simple Interest B. Compound Interest Simple Interest: Interest Is Simply The Price Paid For The Use of Borrowed MoneyDocument12 pagesA. Simple Interest B. Compound Interest Simple Interest: Interest Is Simply The Price Paid For The Use of Borrowed MoneyArcon Solite BarbanidaNo ratings yet

- Simple Annuity 1Document13 pagesSimple Annuity 1Kelvin BarceLon0% (1)

- MATH 112 - Final Exam - Costas - Ana MaeDocument6 pagesMATH 112 - Final Exam - Costas - Ana MaeMildred MuzonesNo ratings yet

- Module 7-8-AnnuityDocument19 pagesModule 7-8-AnnuityI am AngelllNo ratings yet

- Simple InterestDocument3 pagesSimple InterestlalaNo ratings yet

- General MathDocument13 pagesGeneral MathKristine BurlaNo ratings yet

- Study Unit 5 - Spreadsheet Formulas and FunctionsDocument46 pagesStudy Unit 5 - Spreadsheet Formulas and FunctionsShane GowerNo ratings yet

- Introduction To Valuation - The Time Value of MoneyDocument8 pagesIntroduction To Valuation - The Time Value of MoneyPia AlcantaraNo ratings yet

- Lecture 3 Answers 1Document5 pagesLecture 3 Answers 1Thắng ThôngNo ratings yet

- SecAB, Assignment#4, Rebecca HamiltonDocument11 pagesSecAB, Assignment#4, Rebecca HamiltonBeccaNo ratings yet

- QMS - Question Bank - 2013Document99 pagesQMS - Question Bank - 2013Syed Haseeb Naqvi0% (1)

- Module 5Document21 pagesModule 5cris laslasNo ratings yet

- An Hoài Thu - CHAPTER 5+6 - FIN202Document19 pagesAn Hoài Thu - CHAPTER 5+6 - FIN202An Hoài ThuNo ratings yet

- 10 General AnnuityDocument24 pages10 General AnnuityALJON TABUADANo ratings yet

- Chap 3 Time Value of MoneyDocument19 pagesChap 3 Time Value of MoneyClaudine DuhapaNo ratings yet

- Financial Management For Engineers & ProfessionalsDocument10 pagesFinancial Management For Engineers & Professionalsumair_b86No ratings yet

- Lecture Engineering Economic AnalysisDocument64 pagesLecture Engineering Economic Analysisvon11No ratings yet

- Tutorial 2 - Mathematics of Finance PDFDocument3 pagesTutorial 2 - Mathematics of Finance PDFИбрагим ИбрагимовNo ratings yet

- FM Reviewer MidtermDocument21 pagesFM Reviewer MidtermPablo CoelhoNo ratings yet

- CF Unit1-4 Time Value of Money Video LecturesDocument2 pagesCF Unit1-4 Time Value of Money Video LecturesvishwaNo ratings yet

- Vidallon BF LP q1 w5!6!1006Document8 pagesVidallon BF LP q1 w5!6!1006Ailene QuirapNo ratings yet

- Financial Management of Projects and Contracts Lecture 1Document37 pagesFinancial Management of Projects and Contracts Lecture 1Mohamed AtefNo ratings yet

- Introduction To Valuation: The Time Value of Money: Chapter OrganizationDocument58 pagesIntroduction To Valuation: The Time Value of Money: Chapter OrganizationAshar Ahmad FastNuNo ratings yet

- Foundations of Financial Planning - Overview& ProcessDocument90 pagesFoundations of Financial Planning - Overview& ProcesstsrajanNo ratings yet

- Pound - Interest InvestigationDocument7 pagesPound - Interest InvestigationNatalia FilipowiczNo ratings yet

- Financial Math With Calculators and ExcellDocument22 pagesFinancial Math With Calculators and ExcellJulio JoséNo ratings yet

- Chapter 3 - Time Value of MoneyDocument25 pagesChapter 3 - Time Value of MoneyVainess S Zulu0% (1)

- Financial Management (FN-550) : Course IntroductionDocument5 pagesFinancial Management (FN-550) : Course IntroductionAsadEjazButtNo ratings yet

- Understanding The Time Value of MoneyDocument13 pagesUnderstanding The Time Value of MoneyDaniel HunksNo ratings yet

- Time Value of MoneyDocument20 pagesTime Value of MoneyEddie KibuthuNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Engineering EconomyDocument159 pagesEngineering EconomyAlbert Aguilor88% (8)

- FNCE 623 Formulae For Mid Term ExamDocument3 pagesFNCE 623 Formulae For Mid Term Examleili fallahNo ratings yet

- Slm7 Present and Future Values 1Document18 pagesSlm7 Present and Future Values 1giovana therese duyapatNo ratings yet

- QuizDocument2 pagesQuizRepunzel RaajNo ratings yet

- TMV Solved ProblemDocument27 pagesTMV Solved ProblemIdrisNo ratings yet

- Annuity - Introduction Ordinary AnnuityDocument24 pagesAnnuity - Introduction Ordinary AnnuityThomasaquinos msigala JrNo ratings yet

- Simple AnnuityDocument22 pagesSimple AnnuityAshley AniganNo ratings yet

- Gen Math Q2 - Week 4 - General AnnuityDocument22 pagesGen Math Q2 - Week 4 - General AnnuityFrancisco, Ashley Dominique V.No ratings yet

- Module 7. Annuities: 1. Simple AnnuityDocument19 pagesModule 7. Annuities: 1. Simple AnnuityMori OugaiNo ratings yet

- Lecture9 - ES301 Engineering EconomicsDocument19 pagesLecture9 - ES301 Engineering EconomicsLory Liza Bulay-ogNo ratings yet

- FM CH - IiiDocument18 pagesFM CH - IiiGizaw BelayNo ratings yet

- MOI Midterm LessonDocument82 pagesMOI Midterm LessonPie CanapiNo ratings yet

- Basic QuantDocument12 pagesBasic Quantchickenmurgi365No ratings yet

- Genmath Q2 W3 4.1Document21 pagesGenmath Q2 W3 4.1Halloween NightNo ratings yet

- Financial Management Ch06Document52 pagesFinancial Management Ch06Muhammad Afnan MuammarNo ratings yet

- CHAPTER 4 Mathematics of FinanceDocument66 pagesCHAPTER 4 Mathematics of FinanceHailemariamNo ratings yet

- 15 AnnuitiesDocument28 pages15 AnnuitiesMahendra AvinashNo ratings yet

- 4 CHAPTER 4 Mathematics of Finance Short SlideDocument55 pages4 CHAPTER 4 Mathematics of Finance Short Slidevalenciawinno5No ratings yet

- Simple and General AnnuityDocument28 pagesSimple and General AnnuityLynn DomingoNo ratings yet

- General Mathematics 2nd Quarter Week 3 TERESA A. TACIS NHC HS NewDocument11 pagesGeneral Mathematics 2nd Quarter Week 3 TERESA A. TACIS NHC HS NewjohnNo ratings yet

- Time Value of MoneyDocument18 pagesTime Value of MoneyLatasha AdhiakriNo ratings yet

- General-Mathematics Simple-Annuity EDITEDDocument66 pagesGeneral-Mathematics Simple-Annuity EDITEDkcereban2021No ratings yet

- Define The Types of Annuities Overdue, Early, Differed, Undefined, Perpetual, General.Document19 pagesDefine The Types of Annuities Overdue, Early, Differed, Undefined, Perpetual, General.Fernando CooperNo ratings yet

- Annuities and Amortization: Classifications Formula Sample ProblemsDocument27 pagesAnnuities and Amortization: Classifications Formula Sample ProblemsMr.Clown 107No ratings yet

- ANNUITYDocument21 pagesANNUITYsuzhanearriba50No ratings yet

- Financial MGMT, Ch3Document29 pagesFinancial MGMT, Ch3heysemNo ratings yet

- TVM & CompoundingDocument8 pagesTVM & CompoundingUday BansalNo ratings yet

- Time Value of Money: Key PointsDocument5 pagesTime Value of Money: Key PointsUday BansalNo ratings yet

- General Mathematics: Quarter 2 - Module 6: Simple and Compound InterestsDocument22 pagesGeneral Mathematics: Quarter 2 - Module 6: Simple and Compound InterestsEldon Kim RaguindinNo ratings yet

- CE22 - 06 - Nominal Effective Interest RateDocument42 pagesCE22 - 06 - Nominal Effective Interest RateMarco ConopioNo ratings yet

- FM I CH IiiDocument8 pagesFM I CH IiiDùķe HPNo ratings yet

- Chapter 2 Money Time Relationships and Equivalence 2Document21 pagesChapter 2 Money Time Relationships and Equivalence 2Coreen ElizaldeNo ratings yet

- Module 3 Math1 Ge3Document10 pagesModule 3 Math1 Ge3orogrichchelynNo ratings yet

- Module 4 - BusimathDocument5 pagesModule 4 - BusimathAcelin Rayelle TULAGANNo ratings yet

- Simple and Compound Interest: Concept of Time and Value OfmoneyDocument11 pagesSimple and Compound Interest: Concept of Time and Value OfmoneyUnzila AtiqNo ratings yet

- Annuitie S: Liuren WuDocument39 pagesAnnuitie S: Liuren Wusaikumar selaNo ratings yet

- Consumer Mathematics: Gwendolyn TadeoDocument14 pagesConsumer Mathematics: Gwendolyn TadeoproximusNo ratings yet

- General Mathematics: Quarter 2 - Module 1 Simple and Compound InterestsDocument21 pagesGeneral Mathematics: Quarter 2 - Module 1 Simple and Compound InterestsThegame1991ususus100% (2)

- PEB4102 Chapter 4Document61 pagesPEB4102 Chapter 4LimNo ratings yet

- Assignment 1558589300 SmsDocument26 pagesAssignment 1558589300 Smspreciousfrancis365No ratings yet

- Module 3 Introduction To AnnuitiesDocument17 pagesModule 3 Introduction To AnnuitiesJenny AltazarNo ratings yet

- Ordinary Annuity and SuchDocument20 pagesOrdinary Annuity and SuchアゼロスレイゼルNo ratings yet

- Time Value of Money 1-1!1!044649Document67 pagesTime Value of Money 1-1!1!044649Yusuph HajiNo ratings yet

- Compound InterestDocument16 pagesCompound Interestv.garganera.551005No ratings yet

- Ch.4 Math of Finance-1Document19 pagesCh.4 Math of Finance-1hildamezmur9No ratings yet

- General Mathematics: Quarter 2 - Module 7 AnnuitiesDocument40 pagesGeneral Mathematics: Quarter 2 - Module 7 AnnuitiesBreanna CIel E. Cabahit100% (1)

- CUZ CORP FIN Time Value For Money-1Document16 pagesCUZ CORP FIN Time Value For Money-1KIMBERLY MUKAMBANo ratings yet

- Amortization and Sinking FundDocument16 pagesAmortization and Sinking FundRuthchel YaboNo ratings yet

- Simple AnnuityDocument28 pagesSimple AnnuityKelvin BarceLon33% (3)

- Topic 2 Principles of Money-Time RelationshipDocument28 pagesTopic 2 Principles of Money-Time RelationshipJeshua Llorera0% (1)

- Business Maths 1 Interest-1Document24 pagesBusiness Maths 1 Interest-1emmanuelifende1234No ratings yet

- Time Value of Money: Marios MavridesDocument35 pagesTime Value of Money: Marios Mavridesandreas panayiotouNo ratings yet

- Grade 11 Math MOd 6Document12 pagesGrade 11 Math MOd 6John Lois VanNo ratings yet

- Compound InterestDocument5 pagesCompound InterestLegaspi AllanNo ratings yet

- U N It: 7.0 Learning OutcomesDocument28 pagesU N It: 7.0 Learning Outcomesjokes & comedies onlyNo ratings yet

- Chapter 9: Mathematics of FinanceDocument55 pagesChapter 9: Mathematics of FinanceQuang PHAMNo ratings yet

- Mathematics of Investment Module 5Document4 pagesMathematics of Investment Module 5Kim JayNo ratings yet

- AnnuitiesDocument68 pagesAnnuitiesnimra khaliqNo ratings yet

- A. Simple Interest B. Compound Interest Simple Interest: Interest Is Simply The Price Paid For The Use of Borrowed MoneyDocument12 pagesA. Simple Interest B. Compound Interest Simple Interest: Interest Is Simply The Price Paid For The Use of Borrowed MoneyArcon Solite BarbanidaNo ratings yet

- Simple Annuity 1Document13 pagesSimple Annuity 1Kelvin BarceLon0% (1)

- MATH 112 - Final Exam - Costas - Ana MaeDocument6 pagesMATH 112 - Final Exam - Costas - Ana MaeMildred MuzonesNo ratings yet

- Module 7-8-AnnuityDocument19 pagesModule 7-8-AnnuityI am AngelllNo ratings yet

- Simple InterestDocument3 pagesSimple InterestlalaNo ratings yet

- General MathDocument13 pagesGeneral MathKristine BurlaNo ratings yet

- Study Unit 5 - Spreadsheet Formulas and FunctionsDocument46 pagesStudy Unit 5 - Spreadsheet Formulas and FunctionsShane GowerNo ratings yet

- Introduction To Valuation - The Time Value of MoneyDocument8 pagesIntroduction To Valuation - The Time Value of MoneyPia AlcantaraNo ratings yet

- Lecture 3 Answers 1Document5 pagesLecture 3 Answers 1Thắng ThôngNo ratings yet

- SecAB, Assignment#4, Rebecca HamiltonDocument11 pagesSecAB, Assignment#4, Rebecca HamiltonBeccaNo ratings yet

- QMS - Question Bank - 2013Document99 pagesQMS - Question Bank - 2013Syed Haseeb Naqvi0% (1)

- Module 5Document21 pagesModule 5cris laslasNo ratings yet

- An Hoài Thu - CHAPTER 5+6 - FIN202Document19 pagesAn Hoài Thu - CHAPTER 5+6 - FIN202An Hoài ThuNo ratings yet

- 10 General AnnuityDocument24 pages10 General AnnuityALJON TABUADANo ratings yet

- Chap 3 Time Value of MoneyDocument19 pagesChap 3 Time Value of MoneyClaudine DuhapaNo ratings yet

- Financial Management For Engineers & ProfessionalsDocument10 pagesFinancial Management For Engineers & Professionalsumair_b86No ratings yet

- Lecture Engineering Economic AnalysisDocument64 pagesLecture Engineering Economic Analysisvon11No ratings yet

- Tutorial 2 - Mathematics of Finance PDFDocument3 pagesTutorial 2 - Mathematics of Finance PDFИбрагим ИбрагимовNo ratings yet

- FM Reviewer MidtermDocument21 pagesFM Reviewer MidtermPablo CoelhoNo ratings yet

- CF Unit1-4 Time Value of Money Video LecturesDocument2 pagesCF Unit1-4 Time Value of Money Video LecturesvishwaNo ratings yet

- Vidallon BF LP q1 w5!6!1006Document8 pagesVidallon BF LP q1 w5!6!1006Ailene QuirapNo ratings yet

- Financial Management of Projects and Contracts Lecture 1Document37 pagesFinancial Management of Projects and Contracts Lecture 1Mohamed AtefNo ratings yet

- Introduction To Valuation: The Time Value of Money: Chapter OrganizationDocument58 pagesIntroduction To Valuation: The Time Value of Money: Chapter OrganizationAshar Ahmad FastNuNo ratings yet

- Foundations of Financial Planning - Overview& ProcessDocument90 pagesFoundations of Financial Planning - Overview& ProcesstsrajanNo ratings yet

- Pound - Interest InvestigationDocument7 pagesPound - Interest InvestigationNatalia FilipowiczNo ratings yet

- Financial Math With Calculators and ExcellDocument22 pagesFinancial Math With Calculators and ExcellJulio JoséNo ratings yet

- Chapter 3 - Time Value of MoneyDocument25 pagesChapter 3 - Time Value of MoneyVainess S Zulu0% (1)

- Financial Management (FN-550) : Course IntroductionDocument5 pagesFinancial Management (FN-550) : Course IntroductionAsadEjazButtNo ratings yet

- Understanding The Time Value of MoneyDocument13 pagesUnderstanding The Time Value of MoneyDaniel HunksNo ratings yet

- Time Value of MoneyDocument20 pagesTime Value of MoneyEddie KibuthuNo ratings yet