Download as pptx, pdf, or txt

You might also like

- Case Study M&L ManufacturingDocument8 pagesCase Study M&L ManufacturingGeraldine Mahinay50% (2)

- Case1 Colorscope Solution PPTXDocument42 pagesCase1 Colorscope Solution PPTXAmit Dixit100% (1)

- Coping With Institutional Order Flow Zicklin School of Business Financial Markets SeriesDocument208 pagesCoping With Institutional Order Flow Zicklin School of Business Financial Markets SeriesRavi Varakala100% (6)

- 2223S1FL HW1 G3Document7 pages2223S1FL HW1 G3Tiến Nguyễn100% (1)

- Aggregate Planning Session 2: Course: Production & Operation Analysis Effective Period: September 2015Document27 pagesAggregate Planning Session 2: Course: Production & Operation Analysis Effective Period: September 2015AfifahSeptiaNo ratings yet

- Group 1 Donner Company CaseDocument7 pagesGroup 1 Donner Company CaseAjay Kumar100% (1)

- New EFT Level 1 ManualDocument64 pagesNew EFT Level 1 Manualemofree100% (6)

- Aggregate Planning: Operations Management Dr. Ron Tibben-LembkeDocument27 pagesAggregate Planning: Operations Management Dr. Ron Tibben-LembkeHoward Rivera RarangolNo ratings yet

- Case Study Assignment - Burger RamlyDocument14 pagesCase Study Assignment - Burger RamlyNUR AZIZAH HASANAH AHMAD KHAIRUL ANWARNo ratings yet

- Presentation - Question 11Document8 pagesPresentation - Question 11Jeremiah NcubeNo ratings yet

- Aggregate Production Planning in Industrial EngineeringDocument26 pagesAggregate Production Planning in Industrial EngineeringSuneel Kumar MeenaNo ratings yet

- Aggregate Planning 2Document49 pagesAggregate Planning 2Raj KumarNo ratings yet

- Additional Mathematics Project Work - Hari SampleDocument20 pagesAdditional Mathematics Project Work - Hari SampleFadzilah YayaNo ratings yet

- Cambridge DPW: Technology & Snow Clearing: Alice Yang, Nathalie Bloch, & Tyler JaeckelDocument15 pagesCambridge DPW: Technology & Snow Clearing: Alice Yang, Nathalie Bloch, & Tyler Jaeckelacsi1966No ratings yet

- Labour Cost L4Document40 pagesLabour Cost L4Yopie WishnugrahaNo ratings yet

- Group Test 2 W ASDocument10 pagesGroup Test 2 W ASmeeyaNo ratings yet

- Full-Time Equivalent (FTE) LRA MTG 070208Document18 pagesFull-Time Equivalent (FTE) LRA MTG 070208Adnanlatif23No ratings yet

- Aggregate PlanningDocument57 pagesAggregate Planningamitr_scribdNo ratings yet

- TO Operations & Supply Chain Management 2E Problems - SolutionsDocument11 pagesTO Operations & Supply Chain Management 2E Problems - SolutionsMiko Victoria VargasNo ratings yet

- 01 Serenity Makdi - January - CEO ReportDocument7 pages01 Serenity Makdi - January - CEO Reporthaytham.elsadyNo ratings yet

- Tutorial 09: Questions With Possible SolutionsDocument4 pagesTutorial 09: Questions With Possible SolutionsChand DivneshNo ratings yet

- Quick Lunch & Browning ManufacturingDocument9 pagesQuick Lunch & Browning ManufacturingMariaAngelicaMargenApeNo ratings yet

- Critical Path Method (CPM)Document9 pagesCritical Path Method (CPM)Chaudhary Zaeem WajahatNo ratings yet

- Accm507: Academic Task I: (Master of Business Administration)Document9 pagesAccm507: Academic Task I: (Master of Business Administration)kunarapu gopi krishnaNo ratings yet

- Putting Data To Work: Facilitator'S GuideDocument75 pagesPutting Data To Work: Facilitator'S GuideRajeshNo ratings yet

- WorksheetDocument54 pagesWorksheetSayed Farrukh AhmedNo ratings yet

- Sample Project PDFDocument26 pagesSample Project PDFsumitNo ratings yet

- Disadvantage of Life Cycle CostingDocument6 pagesDisadvantage of Life Cycle CostingchekuhakimNo ratings yet

- Zero-Based Golf Course Budgeting: A Model For Increased EffectivenessDocument23 pagesZero-Based Golf Course Budgeting: A Model For Increased EffectivenessMichael D. Vogt100% (2)

- 25 Class WFMDocument22 pages25 Class WFMabdullah.m.m123No ratings yet

- Chapter 3Document13 pagesChapter 3Carl John SedimoNo ratings yet

- Project Report On Costing System Followed by A Hotel..Document14 pagesProject Report On Costing System Followed by A Hotel..Vaibhavi Shah0% (1)

- OM-HP Project Report Group3Document3 pagesOM-HP Project Report Group3Ninaad MadrasNo ratings yet

- Submitted By: Submitted ToDocument14 pagesSubmitted By: Submitted ToDevang JasoliyaNo ratings yet

- Construction Cost Analysis and Financial Controls (Week 3)Document65 pagesConstruction Cost Analysis and Financial Controls (Week 3)RichardNo ratings yet

- Cost SheetDocument29 pagesCost SheetJunaid JamshaidNo ratings yet

- Day 2 - Reduce COGSDocument195 pagesDay 2 - Reduce COGSarpitkhemka1602871No ratings yet

- DI TableDocument44 pagesDI TableSahil AroraNo ratings yet

- Data Entry RulesDocument46 pagesData Entry RulesNguyen Quang HuyNo ratings yet

- 2022 English Module Framework 188 179Document21 pages2022 English Module Framework 188 179Sayuri NaidooNo ratings yet

- Experiment 1: To Determine The Normal and Standard Time For Given ActivityDocument8 pagesExperiment 1: To Determine The Normal and Standard Time For Given ActivityUsamaIjazNo ratings yet

- Bussiness Plan For Manufacturing of Guar Gum: Submitted By: E.Mounika VH/16-58Document35 pagesBussiness Plan For Manufacturing of Guar Gum: Submitted By: E.Mounika VH/16-58eerla mounikaNo ratings yet

- 02 Serenity Makdi - February - CEO ReportDocument7 pages02 Serenity Makdi - February - CEO Reporthaytham.elsadyNo ratings yet

- Nguyễn Minh Nguyên - 31211020572 - MidtermDocument9 pagesNguyễn Minh Nguyên - 31211020572 - MidtermMinh NguyênNo ratings yet

- Problem 6Document7 pagesProblem 6Jaylord PidoNo ratings yet

- 20454-Akshaya Patra Post-Discussion QuestionsDocument2 pages20454-Akshaya Patra Post-Discussion QuestionsSai BhargavNo ratings yet

- Accounting For LabourDocument43 pagesAccounting For LabourMunyaradzi Onismas ChinyukwiNo ratings yet

- Aggregate Planning: Translating Demand Forecasts Production Capacity LevelsDocument27 pagesAggregate Planning: Translating Demand Forecasts Production Capacity LevelsArshad AbbasNo ratings yet

- Work Hard TheroyDocument3 pagesWork Hard TheroyMohammad TooneerNo ratings yet

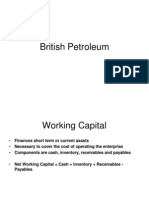

- British PetroleumDocument7 pagesBritish PetroleumboniadityaNo ratings yet

- Ministry of Education and Training Ueh University - Ueh College of Business School of International Business - MarketingDocument26 pagesMinistry of Education and Training Ueh University - Ueh College of Business School of International Business - MarketingTracy M.No ratings yet

- Aggregate Planning: Translating Demand Forecasts Production Capacity LevelsDocument27 pagesAggregate Planning: Translating Demand Forecasts Production Capacity LevelsDotecho Jzo EyNo ratings yet

- MBA 504 Ch3 SolutionsDocument22 pagesMBA 504 Ch3 SolutionsMohit Kumar GuptaNo ratings yet

- Chapter 2Document19 pagesChapter 2ahmedgalalabdalbaath2003No ratings yet

- Operations Management Session 6 - Chap 4-Prof. Furquan IHfIfZgRKlDocument30 pagesOperations Management Session 6 - Chap 4-Prof. Furquan IHfIfZgRKlNABARUN MAJUMDARNo ratings yet

- Ceres Gardening Company Submission TemplateDocument7 pagesCeres Gardening Company Submission TemplateAnkur PansaraNo ratings yet

- Ie 212 Final Project Case StudyDocument6 pagesIe 212 Final Project Case StudyPatrick Joel PalcoNo ratings yet

- Programme: Assignment Cover SheetDocument18 pagesProgramme: Assignment Cover SheetncengimpiloNo ratings yet

- AT&T Vs MegafonDocument18 pagesAT&T Vs MegafonMikhay IstratiyNo ratings yet

- Work Analysis and Improvement: Prof M G KorgaonkerDocument10 pagesWork Analysis and Improvement: Prof M G KorgaonkerMeghna AgarwalNo ratings yet

- Construction Quantity Surveying: A Practical Guide for the Contractor's QSFrom EverandConstruction Quantity Surveying: A Practical Guide for the Contractor's QSRating: 5 out of 5 stars5/5 (2)

- hygDocument3 pageshygJeremiah NcubeNo ratings yet

- Inclass TestDocument2 pagesInclass TestJeremiah NcubeNo ratings yet

- zviko CVDocument2 pageszviko CVJeremiah NcubeNo ratings yet

- Group 18 PresentationDocument11 pagesGroup 18 PresentationJeremiah NcubeNo ratings yet

- Assignment 0ne Due 25 October 2020 Group (1)Document7 pagesAssignment 0ne Due 25 October 2020 Group (1)Jeremiah NcubeNo ratings yet

- SummaryDocument4 pagesSummaryJeremiah NcubeNo ratings yet

- Joy Ben Question 13Document13 pagesJoy Ben Question 13Jeremiah NcubeNo ratings yet

- Mlambi Shingai Qn14 PresentatDocument11 pagesMlambi Shingai Qn14 PresentatJeremiah NcubeNo ratings yet

- Nigel Mutukwa Question 9 PresentationDocument10 pagesNigel Mutukwa Question 9 PresentationJeremiah NcubeNo ratings yet

- PM PresentationDocument12 pagesPM PresentationJeremiah NcubeNo ratings yet

- Group 17 Block Presentation (c20141840x)Document7 pagesGroup 17 Block Presentation (c20141840x)Jeremiah NcubeNo ratings yet

- Question 8 PresentationDocument11 pagesQuestion 8 PresentationJeremiah NcubeNo ratings yet

- Question 13 Mangwiro LTDDocument3 pagesQuestion 13 Mangwiro LTDJeremiah NcubeNo ratings yet

- Group 18 PreseNtation. (Evalaution of The Synergy Between Communication and Leadersip)Document15 pagesGroup 18 PreseNtation. (Evalaution of The Synergy Between Communication and Leadersip)Jeremiah NcubeNo ratings yet

- Performance Management PresentationDocument14 pagesPerformance Management PresentationJeremiah NcubeNo ratings yet

- QN 5 Performance Management PresentationDocument8 pagesQN 5 Performance Management PresentationJeremiah NcubeNo ratings yet

- Chingombe Kudzai and Julius CUACM 413 PresentationDocument9 pagesChingombe Kudzai and Julius CUACM 413 PresentationJeremiah NcubeNo ratings yet

- Group PresentationDocument3 pagesGroup PresentationJeremiah NcubeNo ratings yet

- SolutionDocument57 pagesSolutionJeremiah NcubeNo ratings yet

- Transfer Pricing, Tax Avoidance and International TaxationDocument81 pagesTransfer Pricing, Tax Avoidance and International TaxationJeremiah NcubeNo ratings yet

- Group 3 PresentationDocument10 pagesGroup 3 PresentationJeremiah NcubeNo ratings yet

- Corporate Government Oct 2023Document1 pageCorporate Government Oct 2023Jeremiah NcubeNo ratings yet

- Exploring Combinations and The Pascal Triangle Through MusicDocument17 pagesExploring Combinations and The Pascal Triangle Through MusicWayne Pedranti100% (2)

- DichotomousKeyNYFish PDFDocument13 pagesDichotomousKeyNYFish PDFNermine AbedNo ratings yet

- CRDB Bank Job Opportunities Customer ExperienceDocument4 pagesCRDB Bank Job Opportunities Customer ExperienceAnonymous FnM14a0No ratings yet

- UF - 455 - G Presentation Sheet 2011Document4 pagesUF - 455 - G Presentation Sheet 2011Carlos Perez TrujilloNo ratings yet

- ISBB CompilationDocument6 pagesISBB CompilationElla SalesNo ratings yet

- Diesel Engine Crankshaft DisassemblyDocument15 pagesDiesel Engine Crankshaft DisassemblyAnshar NaraNo ratings yet

- JILG Students Learn by Serving Others.: Benton High School JILG ReportDocument4 pagesJILG Students Learn by Serving Others.: Benton High School JILG ReportjilgincNo ratings yet

- Principle of ManagementDocument6 pagesPrinciple of ManagementArthiNo ratings yet

- IB Chemistry - SL Topic 7 Questions 1Document19 pagesIB Chemistry - SL Topic 7 Questions 1vaxor16689No ratings yet

- Nutrition Education Project Final VersionDocument16 pagesNutrition Education Project Final Versionapi-535168013No ratings yet

- Complex GroupsDocument12 pagesComplex GroupsRaquibul HasanNo ratings yet

- Early DwellingsDocument33 pagesEarly DwellingsVasudha UNo ratings yet

- Bluetooth Car Using ArduinoDocument13 pagesBluetooth Car Using ArduinoRainy Thakur100% (1)

- METRIX AUTOCOMP - Company ProfileDocument2 pagesMETRIX AUTOCOMP - Company ProfileVaibhav AggarwalNo ratings yet

- FEG Token Litepaper v2.1Document15 pagesFEG Token Litepaper v2.1TelorNo ratings yet

- Zairi 2018Document6 pagesZairi 2018Vinu KohliNo ratings yet

- Analysis of New Topology For 7 - Level Asymmetrical Multilevel Inverter and Its Extension To 19 LevelsDocument19 pagesAnalysis of New Topology For 7 - Level Asymmetrical Multilevel Inverter and Its Extension To 19 LevelsInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Cunningworths' Checklist (1995) : Number Items YES NO A. Aims and Approaches 1 2 3 4 B. Design and Organization 5 6 7 8Document3 pagesCunningworths' Checklist (1995) : Number Items YES NO A. Aims and Approaches 1 2 3 4 B. Design and Organization 5 6 7 8Thảo NhiNo ratings yet

- ANSI B30.8 InterpretationDocument10 pagesANSI B30.8 InterpretationAndreyNo ratings yet

- General Information: Location A Location BDocument2 pagesGeneral Information: Location A Location BNikNo ratings yet

- Selection & Applications of Power Factor Correction Capacitor For Industrial and Large Commercial Users Ben Banerjee Power Quality Solution GroupDocument61 pagesSelection & Applications of Power Factor Correction Capacitor For Industrial and Large Commercial Users Ben Banerjee Power Quality Solution Groupraghav4life8724No ratings yet

- Department of Musicology Faculty of MusicDocument196 pagesDepartment of Musicology Faculty of MusicBojan MarjanovicNo ratings yet

- The Decline of The WestDocument3 pagesThe Decline of The Westyasminbahat80% (5)

- Phantom Turbo 6000Document22 pagesPhantom Turbo 6000Manos LoukianosNo ratings yet

- Leakage Management TechnologiesDocument380 pagesLeakage Management TechnologiesWengineerNo ratings yet

- PhilosophyDocument4 pagesPhilosophyJudalineNo ratings yet

- 3rdquarter Week7 Landslide and SinkholeDocument4 pages3rdquarter Week7 Landslide and SinkholeNayeon IeeNo ratings yet

- Seven Paths To Perfection Kirpal SinghDocument52 pagesSeven Paths To Perfection Kirpal SinghjaideepkdNo ratings yet