Public Finance & Taxation - Chapter 4, PT IV

Public Finance & Taxation - Chapter 4, PT IV

You might also like

- Requirement: Prepare Journal Entries in The Books of The Home Office and in The Books of The Branch Office ForDocument2 pagesRequirement: Prepare Journal Entries in The Books of The Home Office and in The Books of The Branch Office ForvonnevaleNo ratings yet

- Noncurrent Asset Held For Sale: Problem 6-1 (IFRS)Document10 pagesNoncurrent Asset Held For Sale: Problem 6-1 (IFRS)Kimberly Claire Atienza71% (7)

- Cpa Reviewer PDFDocument18 pagesCpa Reviewer PDFAbigail Ann PasiliaoNo ratings yet

- Working Capital On WIPRO & ITCDocument50 pagesWorking Capital On WIPRO & ITCMainak Bose75% (8)

- 4 5980870078554441567Document483 pages4 5980870078554441567Pusheletso Mashilo100% (2)

- Other Income Tax AccountingDocument19 pagesOther Income Tax AccountingHabtamu Hailemariam AsfawNo ratings yet

- CH 6Document95 pagesCH 6mulu melakNo ratings yet

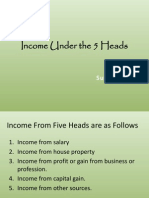

- Income Under The 5 Heads: Sudhir YadavDocument21 pagesIncome Under The 5 Heads: Sudhir YadavpreetkaurrandhawaNo ratings yet

- Public CHAPTER 4Document15 pagesPublic CHAPTER 4embiale ayaluNo ratings yet

- Chapter 7, 8, 12Document41 pagesChapter 7, 8, 12assadrafaqNo ratings yet

- TRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFDocument5 pagesTRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFblackmail1No ratings yet

- Income TaxationDocument38 pagesIncome TaxationElson TalotaloNo ratings yet

- Income Tax in IndiaDocument19 pagesIncome Tax in IndiaConcepts TreeNo ratings yet

- Module-1: Basic Concepts and DefinitionsDocument35 pagesModule-1: Basic Concepts and Definitions2VX20BA091No ratings yet

- Rental IncomeDocument3 pagesRental IncomeZhen WeiNo ratings yet

- Exemptions & Tax Incentives (Act 896) - Power Point PresentationDocument50 pagesExemptions & Tax Incentives (Act 896) - Power Point PresentationGabrielNo ratings yet

- OptDocument3 pagesOptNL CastañaresNo ratings yet

- Chamber of Real Estate and Builders' Association v. RomuloDocument19 pagesChamber of Real Estate and Builders' Association v. RomuloNxxxNo ratings yet

- NIRC Sec. 23 - 26Document5 pagesNIRC Sec. 23 - 26Loren MandaNo ratings yet

- Percentage Tax Excise Tax Documentary Stamp: Taxation LawDocument23 pagesPercentage Tax Excise Tax Documentary Stamp: Taxation LawB-an Javelosa100% (1)

- INCOMETAX M45 ReviewerDocument15 pagesINCOMETAX M45 ReviewerCaryl Isabel Francisco100% (1)

- Income Under The HeadDocument13 pagesIncome Under The HeadParul Bhardwaj VaidyaNo ratings yet

- Tax-Title V Other Percentage TaxesDocument55 pagesTax-Title V Other Percentage Taxesherbertwest19728490No ratings yet

- Tax Law ReviewDocument8 pagesTax Law ReviewIon FashNo ratings yet

- Mba 3 TaxDocument14 pagesMba 3 Taxkapil3518No ratings yet

- Chapter Iii - Tax On Individuals SEC. 24. Income Tax RatesDocument4 pagesChapter Iii - Tax On Individuals SEC. 24. Income Tax RatesangelaggabaoNo ratings yet

- Chapter 5Document7 pagesChapter 5yebegashetNo ratings yet

- Income Tax Unit 1Document44 pagesIncome Tax Unit 1Abhishek BhatiaNo ratings yet

- Fiscal Incentives To TEZ Operators and Registered Tourism Enterprises Within The TEZDocument2 pagesFiscal Incentives To TEZ Operators and Registered Tourism Enterprises Within The TEZjerson_xx6816No ratings yet

- Chamber of Real Estate and Builders' Association v. Romulo, SupraDocument18 pagesChamber of Real Estate and Builders' Association v. Romulo, SupraJMae MagatNo ratings yet

- Taxation CasesDocument296 pagesTaxation CasesshelNo ratings yet

- Chapter Iii - Tax On Individuals SEC. 24. Income Tax RatesDocument2 pagesChapter Iii - Tax On Individuals SEC. 24. Income Tax RatesvocksNo ratings yet

- Module 9 Deductions From Gross IncomeDocument13 pagesModule 9 Deductions From Gross IncomeNineteen AùgùstNo ratings yet

- II Income TaxationDocument8 pagesII Income TaxationNatasha MilitarNo ratings yet

- BLT Challenge (7.17.09)Document8 pagesBLT Challenge (7.17.09)Ren A EleponioNo ratings yet

- 01 Law1993Document17 pages01 Law1993GgoudNo ratings yet

- Percentage Tax: Percentage Tax Is A Business Tax Imposed On Persons, Entities, or TransactionsDocument16 pagesPercentage Tax: Percentage Tax Is A Business Tax Imposed On Persons, Entities, or TransactionsDon CabasiNo ratings yet

- Percentage Tax CTBDocument16 pagesPercentage Tax CTBDon CabasiNo ratings yet

- 22.-CREBA, Inc. v. Romulo, G.R No. 160756Document24 pages22.-CREBA, Inc. v. Romulo, G.R No. 160756Christine Rose Bonilla LikiganNo ratings yet

- Taxation Aef130 BlackboardDocument92 pagesTaxation Aef130 Blackboardqmwdb2k27kNo ratings yet

- Estate TaxDocument10 pagesEstate TaxCharrie Grace PabloNo ratings yet

- General Tax Liabilities of Domestic CorpsDocument5 pagesGeneral Tax Liabilities of Domestic CorpsCora EleazarNo ratings yet

- Chapter 3 Cfs SubsequentDocument48 pagesChapter 3 Cfs SubsequentFasiko AsmaroNo ratings yet

- Allowable Deductions NotesDocument5 pagesAllowable Deductions NotesPaula Mae DacanayNo ratings yet

- Tax On CorporationsDocument4 pagesTax On Corporationsdenise airaNo ratings yet

- Module No 4 - Capital Gains TaxDocument8 pagesModule No 4 - Capital Gains TaxBetty SantiagoNo ratings yet

- Dealings in PropertiesDocument6 pagesDealings in PropertieserespemaychisagangNo ratings yet

- Income Taxation 1: Holding PeriodDocument4 pagesIncome Taxation 1: Holding PeriodKarl John Jay ValderamaNo ratings yet

- Notes in Tax On CorporationDocument7 pagesNotes in Tax On CorporationNinaNo ratings yet

- Chapt-2 Taxation - Source of Public RevenueDocument26 pagesChapt-2 Taxation - Source of Public RevenueYitera SisayNo ratings yet

- Week 4 Co Ownership 2023 241 2Document67 pagesWeek 4 Co Ownership 2023 241 2Arellano Rhovic R.No ratings yet

- T 4 - Co-Ownership Estate TrustDocument21 pagesT 4 - Co-Ownership Estate TrustKristine Aubrey AlvarezNo ratings yet

- Revised Tax QuestionsDocument25 pagesRevised Tax QuestionssophiaNo ratings yet

- Public Finance & Taxation - Chapter 4, PT IIIDocument32 pagesPublic Finance & Taxation - Chapter 4, PT IIIbekelesolomon828No ratings yet

- 7 Taxation For Estates and Trusts CompressDocument6 pages7 Taxation For Estates and Trusts CompressGiella MagnayeNo ratings yet

- Revised Tax QuestionsDocument25 pagesRevised Tax QuestionssophiaNo ratings yet

- Lecture NoDocument6 pagesLecture Nocom01156499073No ratings yet

- Tax Treatment of InvestmentsDocument7 pagesTax Treatment of InvestmentsbnmallickNo ratings yet

- Chapter Ii - General P RinciplesDocument19 pagesChapter Ii - General P RincipleskkkNo ratings yet

- NothingDocument14 pagesNothingitatchi regenciaNo ratings yet

- Final Review Jawaban IntermediateDocument33 pagesFinal Review Jawaban Intermediatelukes12No ratings yet

- MG 3027 TAXATION - Week 19 Introduction To Capital Gains Tax, Computation of Gains and LossesDocument39 pagesMG 3027 TAXATION - Week 19 Introduction To Capital Gains Tax, Computation of Gains and LossesSyed SafdarNo ratings yet

- Property & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsFrom EverandProperty & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsNo ratings yet

- Dividend Discount Model: by Harpreet Kaur Sehgal (Intern, AR Finance Room)Document14 pagesDividend Discount Model: by Harpreet Kaur Sehgal (Intern, AR Finance Room)Tapas SamNo ratings yet

- Chap 011Document33 pagesChap 011ducacapupuNo ratings yet

- Blackswan ProposalDocument6 pagesBlackswan ProposalAmy perottiNo ratings yet

- 905pm - 10.EPRA JOURNALS 13145Document3 pages905pm - 10.EPRA JOURNALS 13145Mohammed YASEENNo ratings yet

- 93-First Pb-AudDocument12 pages93-First Pb-AudAmeroden AbdullahNo ratings yet

- Problem 23-8 QuickBooks Guide PDFDocument1 pageProblem 23-8 QuickBooks Guide PDFJoseph Salido100% (1)

- Kelompok 5 - ALK Problem 9-3Document4 pagesKelompok 5 - ALK Problem 9-3UmiUmiNo ratings yet

- Sample Exam QuestionsDocument16 pagesSample Exam QuestionsMadina SuleimenovaNo ratings yet

- Ace AnalyserDocument4 pagesAce AnalyserRahul MalhotraNo ratings yet

- CapSim Quiz Sample QuestionsDocument2 pagesCapSim Quiz Sample QuestionsDanieNo ratings yet

- E Auction 23 01 2023 FPJ 06 11 Mumbai6Document1 pageE Auction 23 01 2023 FPJ 06 11 Mumbai6Ravie S DhamaNo ratings yet

- HW On Book Value Per ShareDocument4 pagesHW On Book Value Per ShareCharles TuazonNo ratings yet

- Mock BoardsDocument11 pagesMock BoardsRaenessa FranciscoNo ratings yet

- Double Declining Balance Depreciation. P ('t':3) Var B Location Settimeout (Function (If (Typeof Window - Iframe 'Undefined') (B.href B.href ) ), 15000)Document2 pagesDouble Declining Balance Depreciation. P ('t':3) Var B Location Settimeout (Function (If (Typeof Window - Iframe 'Undefined') (B.href B.href ) ), 15000)Johan Mustiko WNo ratings yet

- E 000382112005 Rev0Document2 pagesE 000382112005 Rev0bhaaNo ratings yet

- Individual Assignment: Course Details Fin202 Corporate Finance MR. Vo An Hai Assignment DetailsDocument9 pagesIndividual Assignment: Course Details Fin202 Corporate Finance MR. Vo An Hai Assignment DetailsDoan Thi Cat Linh (K15 DN)No ratings yet

- MODULE 6A Home Office and Branch AccountingDocument14 pagesMODULE 6A Home Office and Branch AccountingmcespressoblendNo ratings yet

- By I/, /uDocument21 pagesBy I/, /uContra Value BetsNo ratings yet

- RitikaDocument73 pagesRitikahanshikagupta6No ratings yet

- Tugas Chapter 10 - Adelia Ana Bella - 1613120001 - AKL2Document3 pagesTugas Chapter 10 - Adelia Ana Bella - 1613120001 - AKL2Meko N TNo ratings yet

- AFAR02-06 JOINT-ARRANGEMENT-iCARE-March-2021 - EncryptedDocument5 pagesAFAR02-06 JOINT-ARRANGEMENT-iCARE-March-2021 - EncryptedSophia PerezNo ratings yet

- WACC and Vol: Counterpoint Global InsightsDocument13 pagesWACC and Vol: Counterpoint Global InsightsHoward QinNo ratings yet

- Single Entry and Incomplete RecordsDocument5 pagesSingle Entry and Incomplete RecordsCalifornia KnightNo ratings yet

- Chirkhwa Hydro Power Ltd.Document36 pagesChirkhwa Hydro Power Ltd.Manita KunwarNo ratings yet

- Edelweiss Internship ProjectDocument17 pagesEdelweiss Internship ProjectHenal PanchmatiyaNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Requirement: Prepare Journal Entries in The Books of The Home Office and in The Books of The Branch Office ForDocument2 pagesRequirement: Prepare Journal Entries in The Books of The Home Office and in The Books of The Branch Office ForvonnevaleNo ratings yet

- Noncurrent Asset Held For Sale: Problem 6-1 (IFRS)Document10 pagesNoncurrent Asset Held For Sale: Problem 6-1 (IFRS)Kimberly Claire Atienza71% (7)

- Cpa Reviewer PDFDocument18 pagesCpa Reviewer PDFAbigail Ann PasiliaoNo ratings yet

- Working Capital On WIPRO & ITCDocument50 pagesWorking Capital On WIPRO & ITCMainak Bose75% (8)

- 4 5980870078554441567Document483 pages4 5980870078554441567Pusheletso Mashilo100% (2)

- Other Income Tax AccountingDocument19 pagesOther Income Tax AccountingHabtamu Hailemariam AsfawNo ratings yet

- CH 6Document95 pagesCH 6mulu melakNo ratings yet

- Income Under The 5 Heads: Sudhir YadavDocument21 pagesIncome Under The 5 Heads: Sudhir YadavpreetkaurrandhawaNo ratings yet

- Public CHAPTER 4Document15 pagesPublic CHAPTER 4embiale ayaluNo ratings yet

- Chapter 7, 8, 12Document41 pagesChapter 7, 8, 12assadrafaqNo ratings yet

- TRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFDocument5 pagesTRAIN (Changes) ???? Pages 2, 6, 10, 14, 15 PDFblackmail1No ratings yet

- Income TaxationDocument38 pagesIncome TaxationElson TalotaloNo ratings yet

- Income Tax in IndiaDocument19 pagesIncome Tax in IndiaConcepts TreeNo ratings yet

- Module-1: Basic Concepts and DefinitionsDocument35 pagesModule-1: Basic Concepts and Definitions2VX20BA091No ratings yet

- Rental IncomeDocument3 pagesRental IncomeZhen WeiNo ratings yet

- Exemptions & Tax Incentives (Act 896) - Power Point PresentationDocument50 pagesExemptions & Tax Incentives (Act 896) - Power Point PresentationGabrielNo ratings yet

- OptDocument3 pagesOptNL CastañaresNo ratings yet

- Chamber of Real Estate and Builders' Association v. RomuloDocument19 pagesChamber of Real Estate and Builders' Association v. RomuloNxxxNo ratings yet

- NIRC Sec. 23 - 26Document5 pagesNIRC Sec. 23 - 26Loren MandaNo ratings yet

- Percentage Tax Excise Tax Documentary Stamp: Taxation LawDocument23 pagesPercentage Tax Excise Tax Documentary Stamp: Taxation LawB-an Javelosa100% (1)

- INCOMETAX M45 ReviewerDocument15 pagesINCOMETAX M45 ReviewerCaryl Isabel Francisco100% (1)

- Income Under The HeadDocument13 pagesIncome Under The HeadParul Bhardwaj VaidyaNo ratings yet

- Tax-Title V Other Percentage TaxesDocument55 pagesTax-Title V Other Percentage Taxesherbertwest19728490No ratings yet

- Tax Law ReviewDocument8 pagesTax Law ReviewIon FashNo ratings yet

- Mba 3 TaxDocument14 pagesMba 3 Taxkapil3518No ratings yet

- Chapter Iii - Tax On Individuals SEC. 24. Income Tax RatesDocument4 pagesChapter Iii - Tax On Individuals SEC. 24. Income Tax RatesangelaggabaoNo ratings yet

- Chapter 5Document7 pagesChapter 5yebegashetNo ratings yet

- Income Tax Unit 1Document44 pagesIncome Tax Unit 1Abhishek BhatiaNo ratings yet

- Fiscal Incentives To TEZ Operators and Registered Tourism Enterprises Within The TEZDocument2 pagesFiscal Incentives To TEZ Operators and Registered Tourism Enterprises Within The TEZjerson_xx6816No ratings yet

- Chamber of Real Estate and Builders' Association v. Romulo, SupraDocument18 pagesChamber of Real Estate and Builders' Association v. Romulo, SupraJMae MagatNo ratings yet

- Taxation CasesDocument296 pagesTaxation CasesshelNo ratings yet

- Chapter Iii - Tax On Individuals SEC. 24. Income Tax RatesDocument2 pagesChapter Iii - Tax On Individuals SEC. 24. Income Tax RatesvocksNo ratings yet

- Module 9 Deductions From Gross IncomeDocument13 pagesModule 9 Deductions From Gross IncomeNineteen AùgùstNo ratings yet

- II Income TaxationDocument8 pagesII Income TaxationNatasha MilitarNo ratings yet

- BLT Challenge (7.17.09)Document8 pagesBLT Challenge (7.17.09)Ren A EleponioNo ratings yet

- 01 Law1993Document17 pages01 Law1993GgoudNo ratings yet

- Percentage Tax: Percentage Tax Is A Business Tax Imposed On Persons, Entities, or TransactionsDocument16 pagesPercentage Tax: Percentage Tax Is A Business Tax Imposed On Persons, Entities, or TransactionsDon CabasiNo ratings yet

- Percentage Tax CTBDocument16 pagesPercentage Tax CTBDon CabasiNo ratings yet

- 22.-CREBA, Inc. v. Romulo, G.R No. 160756Document24 pages22.-CREBA, Inc. v. Romulo, G.R No. 160756Christine Rose Bonilla LikiganNo ratings yet

- Taxation Aef130 BlackboardDocument92 pagesTaxation Aef130 Blackboardqmwdb2k27kNo ratings yet

- Estate TaxDocument10 pagesEstate TaxCharrie Grace PabloNo ratings yet

- General Tax Liabilities of Domestic CorpsDocument5 pagesGeneral Tax Liabilities of Domestic CorpsCora EleazarNo ratings yet

- Chapter 3 Cfs SubsequentDocument48 pagesChapter 3 Cfs SubsequentFasiko AsmaroNo ratings yet

- Allowable Deductions NotesDocument5 pagesAllowable Deductions NotesPaula Mae DacanayNo ratings yet

- Tax On CorporationsDocument4 pagesTax On Corporationsdenise airaNo ratings yet

- Module No 4 - Capital Gains TaxDocument8 pagesModule No 4 - Capital Gains TaxBetty SantiagoNo ratings yet

- Dealings in PropertiesDocument6 pagesDealings in PropertieserespemaychisagangNo ratings yet

- Income Taxation 1: Holding PeriodDocument4 pagesIncome Taxation 1: Holding PeriodKarl John Jay ValderamaNo ratings yet

- Notes in Tax On CorporationDocument7 pagesNotes in Tax On CorporationNinaNo ratings yet

- Chapt-2 Taxation - Source of Public RevenueDocument26 pagesChapt-2 Taxation - Source of Public RevenueYitera SisayNo ratings yet

- Week 4 Co Ownership 2023 241 2Document67 pagesWeek 4 Co Ownership 2023 241 2Arellano Rhovic R.No ratings yet

- T 4 - Co-Ownership Estate TrustDocument21 pagesT 4 - Co-Ownership Estate TrustKristine Aubrey AlvarezNo ratings yet

- Revised Tax QuestionsDocument25 pagesRevised Tax QuestionssophiaNo ratings yet

- Public Finance & Taxation - Chapter 4, PT IIIDocument32 pagesPublic Finance & Taxation - Chapter 4, PT IIIbekelesolomon828No ratings yet

- 7 Taxation For Estates and Trusts CompressDocument6 pages7 Taxation For Estates and Trusts CompressGiella MagnayeNo ratings yet

- Revised Tax QuestionsDocument25 pagesRevised Tax QuestionssophiaNo ratings yet

- Lecture NoDocument6 pagesLecture Nocom01156499073No ratings yet

- Tax Treatment of InvestmentsDocument7 pagesTax Treatment of InvestmentsbnmallickNo ratings yet

- Chapter Ii - General P RinciplesDocument19 pagesChapter Ii - General P RincipleskkkNo ratings yet

- NothingDocument14 pagesNothingitatchi regenciaNo ratings yet

- Final Review Jawaban IntermediateDocument33 pagesFinal Review Jawaban Intermediatelukes12No ratings yet

- MG 3027 TAXATION - Week 19 Introduction To Capital Gains Tax, Computation of Gains and LossesDocument39 pagesMG 3027 TAXATION - Week 19 Introduction To Capital Gains Tax, Computation of Gains and LossesSyed SafdarNo ratings yet

- Property & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsFrom EverandProperty & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsNo ratings yet

- Dividend Discount Model: by Harpreet Kaur Sehgal (Intern, AR Finance Room)Document14 pagesDividend Discount Model: by Harpreet Kaur Sehgal (Intern, AR Finance Room)Tapas SamNo ratings yet

- Chap 011Document33 pagesChap 011ducacapupuNo ratings yet

- Blackswan ProposalDocument6 pagesBlackswan ProposalAmy perottiNo ratings yet

- 905pm - 10.EPRA JOURNALS 13145Document3 pages905pm - 10.EPRA JOURNALS 13145Mohammed YASEENNo ratings yet

- 93-First Pb-AudDocument12 pages93-First Pb-AudAmeroden AbdullahNo ratings yet

- Problem 23-8 QuickBooks Guide PDFDocument1 pageProblem 23-8 QuickBooks Guide PDFJoseph Salido100% (1)

- Kelompok 5 - ALK Problem 9-3Document4 pagesKelompok 5 - ALK Problem 9-3UmiUmiNo ratings yet

- Sample Exam QuestionsDocument16 pagesSample Exam QuestionsMadina SuleimenovaNo ratings yet

- Ace AnalyserDocument4 pagesAce AnalyserRahul MalhotraNo ratings yet

- CapSim Quiz Sample QuestionsDocument2 pagesCapSim Quiz Sample QuestionsDanieNo ratings yet

- E Auction 23 01 2023 FPJ 06 11 Mumbai6Document1 pageE Auction 23 01 2023 FPJ 06 11 Mumbai6Ravie S DhamaNo ratings yet

- HW On Book Value Per ShareDocument4 pagesHW On Book Value Per ShareCharles TuazonNo ratings yet

- Mock BoardsDocument11 pagesMock BoardsRaenessa FranciscoNo ratings yet

- Double Declining Balance Depreciation. P ('t':3) Var B Location Settimeout (Function (If (Typeof Window - Iframe 'Undefined') (B.href B.href ) ), 15000)Document2 pagesDouble Declining Balance Depreciation. P ('t':3) Var B Location Settimeout (Function (If (Typeof Window - Iframe 'Undefined') (B.href B.href ) ), 15000)Johan Mustiko WNo ratings yet

- E 000382112005 Rev0Document2 pagesE 000382112005 Rev0bhaaNo ratings yet

- Individual Assignment: Course Details Fin202 Corporate Finance MR. Vo An Hai Assignment DetailsDocument9 pagesIndividual Assignment: Course Details Fin202 Corporate Finance MR. Vo An Hai Assignment DetailsDoan Thi Cat Linh (K15 DN)No ratings yet

- MODULE 6A Home Office and Branch AccountingDocument14 pagesMODULE 6A Home Office and Branch AccountingmcespressoblendNo ratings yet

- By I/, /uDocument21 pagesBy I/, /uContra Value BetsNo ratings yet

- RitikaDocument73 pagesRitikahanshikagupta6No ratings yet

- Tugas Chapter 10 - Adelia Ana Bella - 1613120001 - AKL2Document3 pagesTugas Chapter 10 - Adelia Ana Bella - 1613120001 - AKL2Meko N TNo ratings yet

- AFAR02-06 JOINT-ARRANGEMENT-iCARE-March-2021 - EncryptedDocument5 pagesAFAR02-06 JOINT-ARRANGEMENT-iCARE-March-2021 - EncryptedSophia PerezNo ratings yet

- WACC and Vol: Counterpoint Global InsightsDocument13 pagesWACC and Vol: Counterpoint Global InsightsHoward QinNo ratings yet

- Single Entry and Incomplete RecordsDocument5 pagesSingle Entry and Incomplete RecordsCalifornia KnightNo ratings yet

- Chirkhwa Hydro Power Ltd.Document36 pagesChirkhwa Hydro Power Ltd.Manita KunwarNo ratings yet

- Edelweiss Internship ProjectDocument17 pagesEdelweiss Internship ProjectHenal PanchmatiyaNo ratings yet