Download as pptx, pdf, or txt

You might also like

- Original PDF Fundamentals of Corporate Finance 6th Canadian Edition PDFDocument38 pagesOriginal PDF Fundamentals of Corporate Finance 6th Canadian Edition PDFgwen.garcia161100% (37)

- Assignment 1 - 2021 - 2022Document4 pagesAssignment 1 - 2021 - 2022Assya El MoukademNo ratings yet

- Homework Assignment DoneDocument6 pagesHomework Assignment DoneKezia N. ApriliaNo ratings yet

- Cases Master PDFDocument11 pagesCases Master PDFSam PskovskiNo ratings yet

- Chapter 15 AnswerDocument11 pagesChapter 15 AnswerRojohn ValenzuelaNo ratings yet

- Pro Forma Models - StudentsDocument9 pagesPro Forma Models - Studentsshanker23scribd100% (1)

- A - Case Study: Dreaming Corp.: The Financial Statements of Dreaming Corp. Are The Following (In K )Document7 pagesA - Case Study: Dreaming Corp.: The Financial Statements of Dreaming Corp. Are The Following (In K )Mohamed Lamine SanohNo ratings yet

- Fm3 Chapter03 SV Part 2Document26 pagesFm3 Chapter03 SV Part 2Linh ChiNo ratings yet

- Fm3 Chapter03 SV Part 1Document7 pagesFm3 Chapter03 SV Part 1Linh ChiNo ratings yet

- Superhero Corporation Inc: Financial Statements For The Year Ended 31 December 2009Document9 pagesSuperhero Corporation Inc: Financial Statements For The Year Ended 31 December 2009shazNo ratings yet

- fm3 Chapter03Document45 pagesfm3 Chapter03Syed Zeeshan ArshadNo ratings yet

- Setting Up The Financial Statement ModelDocument45 pagesSetting Up The Financial Statement ModelSyed Ameer Ali ShahNo ratings yet

- Evaluating Financial PerformanceDocument31 pagesEvaluating Financial PerformanceShahruk AnwarNo ratings yet

- Tempest Accounting and AnalysisDocument10 pagesTempest Accounting and AnalysisSIXIAN JIANGNo ratings yet

- Setting Up The Financial Statement ModelDocument25 pagesSetting Up The Financial Statement Modelisaimartinez06No ratings yet

- WBSLive Lecture 5 Slides Pres VevoxDocument25 pagesWBSLive Lecture 5 Slides Pres VevoxabhirejanilNo ratings yet

- Statement of Cash Flow Chapter 2Document10 pagesStatement of Cash Flow Chapter 2Mary Ann PacilanNo ratings yet

- 2-DCF Valuation PDFDocument25 pages2-DCF Valuation PDFFlovgrNo ratings yet

- Analysing Historical Performance: Total Income 180 200 240Document3 pagesAnalysing Historical Performance: Total Income 180 200 240rohitNo ratings yet

- Management Accounting - I: - Dr. Sandeep GoelDocument109 pagesManagement Accounting - I: - Dr. Sandeep GoelRajat Jawa100% (1)

- Topic02 ValuationDocument62 pagesTopic02 ValuationGaukhar RyskulovaNo ratings yet

- Financial Statement Analysis: The Information MazeDocument43 pagesFinancial Statement Analysis: The Information MazeJay DaveNo ratings yet

- Financial AccountingDocument9 pagesFinancial AccountingRiya DhanukaNo ratings yet

- Eflatoun Company: Financial Statements For The Year Ended 31 December 2009Document10 pagesEflatoun Company: Financial Statements For The Year Ended 31 December 2009shazNo ratings yet

- Interpreting Financial StatementsDocument2 pagesInterpreting Financial StatementsSharen HariNo ratings yet

- True or FalseDocument4 pagesTrue or FalseMuchinNo ratings yet

- Copy 1 ACC 223 Practice Problems For Financial Ratio AnalysisDocument3 pagesCopy 1 ACC 223 Practice Problems For Financial Ratio AnalysisGiane Bernard PunayanNo ratings yet

- Credit Management in BanksDocument10 pagesCredit Management in BanksmarufNo ratings yet

- Analysis of FSDocument28 pagesAnalysis of FSHaseeb TariqNo ratings yet

- Financial Planning - ForecastingDocument4 pagesFinancial Planning - ForecastingPrathamesh411No ratings yet

- 03RATIO ANALYSIS MbaDocument18 pages03RATIO ANALYSIS MbaAbid XargarNo ratings yet

- B203B - Accounting and Finance (Part BDocument32 pagesB203B - Accounting and Finance (Part Bahmed helmyNo ratings yet

- Financial Ratios-Hamna RizwanDocument5 pagesFinancial Ratios-Hamna RizwanHamna RizwanNo ratings yet

- International Financial Reporting Cases Topic 1: Case 1: Transactions and Accounting EntriesDocument6 pagesInternational Financial Reporting Cases Topic 1: Case 1: Transactions and Accounting EntriesAnmol SinghNo ratings yet

- Topic 10-12 Alk (Hitungannya)Document6 pagesTopic 10-12 Alk (Hitungannya)Daffa Permana PutraNo ratings yet

- Mio Booklet 2024Document22 pagesMio Booklet 2024Qurat Ul Ain NaqviNo ratings yet

- Subject: Fundamentals of Corporate Finance: Mr. Raza Saeed Hailey College of Banking & FinanceDocument8 pagesSubject: Fundamentals of Corporate Finance: Mr. Raza Saeed Hailey College of Banking & FinanceUmer PrinceNo ratings yet

- Additional ExcelSpreadsheetsDocument35 pagesAdditional ExcelSpreadsheetsbipin kumarNo ratings yet

- Ratio Analysis: Categories of RatiosDocument7 pagesRatio Analysis: Categories of RatiosAhmad vlogsNo ratings yet

- Reformulation of Financial StatementsDocument30 pagesReformulation of Financial StatementsKatty MothaNo ratings yet

- FinStat and FinAnaDocument38 pagesFinStat and FinAnaHaizii PritziiNo ratings yet

- Analytical Income Statement and Balance SheetDocument38 pagesAnalytical Income Statement and Balance SheetSanjayNo ratings yet

- IB Bussiness Management Financial Statements Layout GuideDocument2 pagesIB Bussiness Management Financial Statements Layout GuideBhavish Adwani100% (1)

- Lecture 2-FS, CF TaxesDocument30 pagesLecture 2-FS, CF TaxesAreeba QureshiNo ratings yet

- Acc Cap M - 2019 - Exercise Pack - With SolutionsDocument26 pagesAcc Cap M - 2019 - Exercise Pack - With SolutionsValentinNo ratings yet

- Topic 3.5 Ratio AnalysisDocument22 pagesTopic 3.5 Ratio AnalysisSevarakhon UmarovaNo ratings yet

- 1.0 CFI - FS Primer PDFDocument10 pages1.0 CFI - FS Primer PDFSarthak NautiyalNo ratings yet

- Review FinalDocument10 pagesReview FinalNguyen Minh QuanNo ratings yet

- Financial ForecastingDocument22 pagesFinancial ForecastingKaustav BanerjeeNo ratings yet

- Chapter 2. Understanding The Income StatementDocument10 pagesChapter 2. Understanding The Income StatementVượng TạNo ratings yet

- Chapter 03Document29 pagesChapter 03andi.w.rahardjoNo ratings yet

- Investment Analysis and Portfolio Management 2012Document61 pagesInvestment Analysis and Portfolio Management 2012Nelson Ivan Acosta100% (1)

- Chapter 6 Financial Statement Ratio AnalysisDocument9 pagesChapter 6 Financial Statement Ratio AnalysisHafeezNo ratings yet

- BAB SolutionsDocument8 pagesBAB SolutionsSaraNo ratings yet

- Financial Statement AnalysisDocument14 pagesFinancial Statement AnalysisnabhayNo ratings yet

- Solved ProblemDocument4 pagesSolved ProblemSophiya NeupaneNo ratings yet

- Finance ExplanationsDocument27 pagesFinance ExplanationsAriel Alejandro Guañuna LincangoNo ratings yet

- Ias 7 Cash FlowDocument15 pagesIas 7 Cash FlowManda simzNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Frs Project - Tata Steel AnalysisDocument12 pagesFrs Project - Tata Steel AnalysisSubhasish mahapatraNo ratings yet

- Brief History of BankingDocument5 pagesBrief History of BankingrohanshettymanipalNo ratings yet

- Energy DerivativesDocument126 pagesEnergy DerivativesSachin RawatNo ratings yet

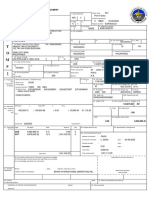

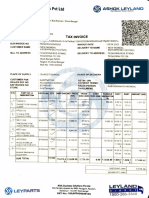

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Vijay SNo ratings yet

- Futures MarketDocument31 pagesFutures MarketyanaNo ratings yet

- Imperfect Competition and TradeDocument48 pagesImperfect Competition and TradeISHIKA SAHANo ratings yet

- Chapter 4Document43 pagesChapter 4Hồ ThảoNo ratings yet

- C2 Note ComprehensiveDocument18 pagesC2 Note ComprehensiveNadiahNo ratings yet

- Week10 EditedDocument6 pagesWeek10 EditedCejay MilNo ratings yet

- Class 1Document39 pagesClass 1Jawad ArkoNo ratings yet

- Module 6 - Lect 3 - Role of CBDocument22 pagesModule 6 - Lect 3 - Role of CBBHAVYA GOPAL 18103096No ratings yet

- Module 4 - Financial Ratios S23Document27 pagesModule 4 - Financial Ratios S23Prachi YadavNo ratings yet

- Breakdown of Transactions-4Document1 pageBreakdown of Transactions-4BabamkweNo ratings yet

- Effects of Demonetization On BanksDocument22 pagesEffects of Demonetization On BanksKrishna GuptaNo ratings yet

- LibroDocument212 pagesLibromiguelchp02No ratings yet

- Chapter 2Document18 pagesChapter 2geexellNo ratings yet

- Open Book Review: Ability: Bs English (Tesol) 3 Semester Department of EnglishDocument12 pagesOpen Book Review: Ability: Bs English (Tesol) 3 Semester Department of EnglishUsama JavaidNo ratings yet

- Bill of Lading Copy Non Negotiable: CarrierDocument4 pagesBill of Lading Copy Non Negotiable: CarrierDaisy, Roda,JhonNo ratings yet

- DeptStores Advanced Shopping PDFReadingDocument3 pagesDeptStores Advanced Shopping PDFReadingNawelNo ratings yet

- Receipt: Transfer OverviewDocument3 pagesReceipt: Transfer OverviewIndo TrackingNo ratings yet

- 9661 Sad PDFDocument2 pages9661 Sad PDFprincess carellNo ratings yet

- Adil ShahDocument9 pagesAdil ShahTalking HistoryNo ratings yet

- SAP Business One Exercises On CurrenciesDocument2 pagesSAP Business One Exercises On CurrenciesAlou CortezNo ratings yet

- 1081 Supporting BillDocument2 pages1081 Supporting BillAshirwad BanerjeeNo ratings yet

- Global Automotive Sector - Euler ReportDocument14 pagesGlobal Automotive Sector - Euler ReportAkshay SatijaNo ratings yet

- Commercial Banking: Prepared By: M2020 - Jeemol Raji Oommen M2021 - Jidnyasa DarneDocument33 pagesCommercial Banking: Prepared By: M2020 - Jeemol Raji Oommen M2021 - Jidnyasa DarneJeemol RajiNo ratings yet

- Chapter-08-Ideas On Operating SegmentsDocument12 pagesChapter-08-Ideas On Operating Segmentsmdrifathossain835No ratings yet

- Au Gold Bullion Buyer'S 1. Terms & Conditions: PROCEDURE: Swiss ProcedureDocument2 pagesAu Gold Bullion Buyer'S 1. Terms & Conditions: PROCEDURE: Swiss ProceduresprataNo ratings yet

- ListDocument6 pagesListRoshelleNo ratings yet