Download as pptx, pdf, or txt

You might also like

- SalaryDocument66 pagesSalaryFurqan AhmedNo ratings yet

- Tax Planning With Refrence To Employee's RemunerationDocument34 pagesTax Planning With Refrence To Employee's RemunerationRishabh Jain83% (6)

- Bar QuestionsDocument24 pagesBar QuestionsbrendamanganaanNo ratings yet

- Inclusion Gross IncomeDocument2 pagesInclusion Gross IncomeAllisa Padre-eNo ratings yet

- Udhayakumar Rice MillDocument12 pagesUdhayakumar Rice Millcachandhiran0% (1)

- Income From SalariesDocument48 pagesIncome From Salarieskeerthana_hassan67% (6)

- Income Under Head SalariesDocument61 pagesIncome Under Head SalariesAbhinay SrivastavNo ratings yet

- Unit 2 SalaryDocument131 pagesUnit 2 SalaryRekha BansalNo ratings yet

- Week 3 - Income From SalariesDocument46 pagesWeek 3 - Income From SalariesAdarsh PandeyNo ratings yet

- Taxation of Income From SalaryDocument20 pagesTaxation of Income From Salaryyokip59536No ratings yet

- 4.1 Salary Theory and Problems 1Document15 pages4.1 Salary Theory and Problems 1Krishna GuptaNo ratings yet

- Paper 7 New Book 83 152 SalaryDocument70 pagesPaper 7 New Book 83 152 SalaryHridya PrasadNo ratings yet

- SalaryDocument11 pagesSalaryshreshthasethi05No ratings yet

- O Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiDocument7 pagesO Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiRadhika SarawagiNo ratings yet

- The Payment of Bonus Act1965Document9 pagesThe Payment of Bonus Act1965nishi18guptaNo ratings yet

- HhytyDocument51 pagesHhytyNitin gNo ratings yet

- Income Under The Head Salary2Document142 pagesIncome Under The Head Salary2OnlineNo ratings yet

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaNo ratings yet

- Income From SalaryDocument21 pagesIncome From SalaryAditya Avasare60% (10)

- Income From Salary Final SEM 3Document49 pagesIncome From Salary Final SEM 3Baleshwar ChauhanNo ratings yet

- Contract For Service Doesnot Include Under The Ambit of Charging TaxDocument79 pagesContract For Service Doesnot Include Under The Ambit of Charging Taxbushra_anwarNo ratings yet

- Income From Salary-FinalDocument42 pagesIncome From Salary-FinalPrathibha TiwariNo ratings yet

- Final Indirect Tax ProjectDocument39 pagesFinal Indirect Tax Projectssg1015No ratings yet

- Chapter 4 Income From Salaries: (Sec.15 To 17)Document32 pagesChapter 4 Income From Salaries: (Sec.15 To 17)kiranshingoteNo ratings yet

- SalariesDocument209 pagesSalariesprajeeshNo ratings yet

- Income From SalaryDocument16 pagesIncome From SalaryGurpreet Singh100% (1)

- Salary Income-Pg DTDocument11 pagesSalary Income-Pg DTOnkar BandichhodeNo ratings yet

- Financial Planning For Salaried Employee and Strategies For Tax SavingsDocument10 pagesFinancial Planning For Salaried Employee and Strategies For Tax Savingscity cyberNo ratings yet

- Income From Salaries: CA Final Paper7 Direct Tax Laws Chapter 4 CA - Rachana KumarDocument65 pagesIncome From Salaries: CA Final Paper7 Direct Tax Laws Chapter 4 CA - Rachana KumarRupaliNo ratings yet

- Income From SalariesDocument70 pagesIncome From SalariesPratik AgrawalNo ratings yet

- Employee's Provident FundDocument31 pagesEmployee's Provident FundMayank ChaturvediNo ratings yet

- Taxation - Direct and Indirect - Chapter 4 PPT MkJy53msNBDocument32 pagesTaxation - Direct and Indirect - Chapter 4 PPT MkJy53msNBRupal DalalNo ratings yet

- Salary IncomeDocument83 pagesSalary IncomechitkarashellyNo ratings yet

- Unit 2 Notes, Part 1Document19 pagesUnit 2 Notes, Part 1Sandip Kumar BhartiNo ratings yet

- Income From SalaryDocument66 pagesIncome From SalaryShamika LloydNo ratings yet

- Unit 2 of Income TaxDocument20 pagesUnit 2 of Income TaxHemal PanchalNo ratings yet

- Taxiation AssignmentDocument9 pagesTaxiation AssignmentNoman AreebNo ratings yet

- Income Under The Head Salary2 PDFDocument142 pagesIncome Under The Head Salary2 PDFswati0% (1)

- Payment of Bonus Act 1965Document31 pagesPayment of Bonus Act 1965Vetri VelanNo ratings yet

- Tax Unit 4 (Tax On Individual)Document116 pagesTax Unit 4 (Tax On Individual)Shivam PalNo ratings yet

- Unit II Part 2 Lecture Notes 5Document19 pagesUnit II Part 2 Lecture Notes 5stevin.john538No ratings yet

- Tax Planning in Respect of Employee's Remuneration ProjrctDocument15 pagesTax Planning in Respect of Employee's Remuneration ProjrctPreyNo ratings yet

- Mission Completed Shubham2Document63 pagesMission Completed Shubham2Ravi SinghNo ratings yet

- Meaning of Salary': Condition For Charging Income U/H "Salaries"Document21 pagesMeaning of Salary': Condition For Charging Income U/H "Salaries"kiranshingoteNo ratings yet

- Taxable Salary IncomeDocument253 pagesTaxable Salary IncomedjbbuzzzNo ratings yet

- Unit 2 - Income From SalaryDocument14 pagesUnit 2 - Income From SalaryRakhi DhamijaNo ratings yet

- Salary Tax CalculatorDocument7 pagesSalary Tax Calculatorbecito6195No ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Income From SalaryDocument19 pagesIncome From SalaryAnupriya BajpaiNo ratings yet

- Income From SalaryDocument29 pagesIncome From SalaryIsmail SayyadNo ratings yet

- Mission Completed Shubham2Document51 pagesMission Completed Shubham2Ravi SinghNo ratings yet

- Army Institute of Law: Concept of Income and Total IncomeDocument17 pagesArmy Institute of Law: Concept of Income and Total IncomeMehr MunjalNo ratings yet

- P2Document18 pagesP2YusufNo ratings yet

- Block 2Document90 pagesBlock 2G RAVIKISHORENo ratings yet

- Chapter-9 Salary IncomeDocument21 pagesChapter-9 Salary IncomeDhrubo Chandro RoyNo ratings yet

- Income From Salary-1Document25 pagesIncome From Salary-1Ila SinghNo ratings yet

- 1 .Income Tax On Salaries - (01.06.2015)Document57 pages1 .Income Tax On Salaries - (01.06.2015)yvNo ratings yet

- 5.3 Exemptions From Income From SalariesDocument3 pages5.3 Exemptions From Income From SalariesYash DedhiaNo ratings yet

- TaxDocument46 pagesTaxAkashTokeNo ratings yet

- Income Under The Head "Salaries"Document7 pagesIncome Under The Head "Salaries"Rahul AgarwalNo ratings yet

- Provident FundDocument18 pagesProvident FundRashmi Ranjan Panigrahi100% (1)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Airtech Systems (India) Pvt. LTD.: Salary Slip For The Month of October 2018Document1 pageAirtech Systems (India) Pvt. LTD.: Salary Slip For The Month of October 2018Mohsin ShaikhNo ratings yet

- TPA Refund ProcessDocument3 pagesTPA Refund ProcessYuan TianNo ratings yet

- Invoice: Shaklee Products (Malaysia) SDN BHDDocument1 pageInvoice: Shaklee Products (Malaysia) SDN BHDMia Sarah ImanNo ratings yet

- 210 - RFP - Sewa Ruangan, Internet, Listrik & Over Time SguDocument8 pages210 - RFP - Sewa Ruangan, Internet, Listrik & Over Time SguSulis SetioriniNo ratings yet

- AdmitereDocument10 pagesAdmitereNicole AdinaNo ratings yet

- Law Commission Report No. 12 - Income Tax Act 1922Document496 pagesLaw Commission Report No. 12 - Income Tax Act 1922Latest Laws Team0% (1)

- Account Statement 011219 290220Document14 pagesAccount Statement 011219 290220ManishNo ratings yet

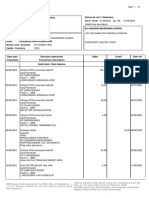

- (Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountDocument1 page(Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountSarthak GahlawatNo ratings yet

- Aq 10Document58 pagesAq 10Minie KimNo ratings yet

- AP AR NettingDocument16 pagesAP AR NettingSurya MaddiboinaNo ratings yet

- Contoh InvoiceDocument1 pageContoh InvoiceChiska TiwieNo ratings yet

- E-Banking: Standard Chartered BankDocument21 pagesE-Banking: Standard Chartered Bankhiral chhedaNo ratings yet

- Cash Flow Statement Indirect MethodDocument5 pagesCash Flow Statement Indirect MethodSaivyjayanthiNo ratings yet

- Irs 1041 FormDocument4 pagesIrs 1041 FormcaliechNo ratings yet

- RMO No. 23-2018 DigestDocument4 pagesRMO No. 23-2018 DigestMary Joy NavajaNo ratings yet

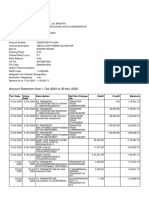

- Account Statement From 1 Oct 2020 To 30 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 1 Oct 2020 To 30 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNITIK BAISOYANo ratings yet

- Government of India Ministry of Corporate Affairs: Signature Not VerifiedDocument1 pageGovernment of India Ministry of Corporate Affairs: Signature Not VerifiedSuman Kalyan SarkarNo ratings yet

- Scenarios For SAP FCVDocument21 pagesScenarios For SAP FCVmanishpawar11No ratings yet

- Sunrise Credit Union: Name No. of Dependents Hourly Wage Hours WorkedDocument2 pagesSunrise Credit Union: Name No. of Dependents Hourly Wage Hours WorkedanzarNo ratings yet

- @ Tarakan - Swiss Bel HotelDocument2 pages@ Tarakan - Swiss Bel Hotelyasa saba100% (2)

- LetterDocument5 pagesLetterJyotirmay SahuNo ratings yet

- Summary Regulation CPA NotesDocument2 pagesSummary Regulation CPA Notesjklein2588100% (1)

- Procedure of Approval of Gratuity Funds Under Income Tax Act, 1961 - Taxguru - inDocument15 pagesProcedure of Approval of Gratuity Funds Under Income Tax Act, 1961 - Taxguru - inJay SharmaNo ratings yet

- Quiz Chapter 2 Statement of Comprehensive IncomeDocument13 pagesQuiz Chapter 2 Statement of Comprehensive Incomefinn mertensNo ratings yet

- PDFDocument4 pagesPDFAnonymous nqKtbr1CrNo ratings yet

- Study On Impact of Banking Technology On Indian EconomyDocument11 pagesStudy On Impact of Banking Technology On Indian EconomyArpita ChoudharyNo ratings yet

- تﺎﺑﺎﺴﺤﻠﻟ ﺪّﺣﻮﻣ ﻒﺸﻛ Consolidated Statement of AccountsDocument11 pagesتﺎﺑﺎﺴﺤﻠﻟ ﺪّﺣﻮﻣ ﻒﺸﻛ Consolidated Statement of Accounts6zf86h9f8gNo ratings yet