2.2 Intangible Assets Lecture 2 2023

2.2 Intangible Assets Lecture 2 2023

You might also like

- Write Two or Three Paragraphs in Which You Describe The Role That Culture Plays in The Development of A CountryDocument4 pagesWrite Two or Three Paragraphs in Which You Describe The Role That Culture Plays in The Development of A CountryVinnu KumarNo ratings yet

- Government Regulation 24/2012Document14 pagesGovernment Regulation 24/2012Adria SaputeroNo ratings yet

- Value Proposition Comparative AnalysisDocument8 pagesValue Proposition Comparative AnalysisNemesio Tejero, IIINo ratings yet

- 04 Ias 38Document4 pages04 Ias 38Irtiza AbbasNo ratings yet

- ACC702 Tutorial - Intangible AssetsDocument3 pagesACC702 Tutorial - Intangible AssetsUshra KhanNo ratings yet

- Audit of Intangible AssetsDocument8 pagesAudit of Intangible AssetsMikaela Graciel AnneNo ratings yet

- Intangible For Non-Current AssetsDocument55 pagesIntangible For Non-Current AssetsChitta LeeNo ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- Intagible Asset 1 1Document13 pagesIntagible Asset 1 1Trina Rose FandiñoNo ratings yet

- Intangible AssetsDocument1 pageIntangible Assetsarmor.coverNo ratings yet

- #23 Intangible Assets (Notes For 6208)Document6 pages#23 Intangible Assets (Notes For 6208)jaysonNo ratings yet

- Research & Development Tax Concession: Discussion SessionDocument18 pagesResearch & Development Tax Concession: Discussion SessionnugosuNo ratings yet

- Fresh BeginningsDocument3 pagesFresh BeginningsALIEVALINo ratings yet

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- Intangible AssetsDocument6 pagesIntangible AssetsChris tine Mae MendozaNo ratings yet

- Miafe B. Almendralejo BSA - 2 Intermediate Accounting 1 2 Sem 2021-22 Discussion (Chapter 33)Document4 pagesMiafe B. Almendralejo BSA - 2 Intermediate Accounting 1 2 Sem 2021-22 Discussion (Chapter 33)Miafe B. AlmendralejoNo ratings yet

- Ias 38 Intangible AssetsDocument4 pagesIas 38 Intangible AssetsYogesh BhattaraiNo ratings yet

- IFRS Development Costs Recognition PDFDocument3 pagesIFRS Development Costs Recognition PDFmizarkoNo ratings yet

- CIPFA PPT Template NEW IPFM PSFR Session 4Document57 pagesCIPFA PPT Template NEW IPFM PSFR Session 4SabNo ratings yet

- F3 - ACCA Chapter-9-1Document15 pagesF3 - ACCA Chapter-9-1Nile NguyenNo ratings yet

- Question 6: Ias 38 Intangible Assets: Page 1 of 2Document2 pagesQuestion 6: Ias 38 Intangible Assets: Page 1 of 2tazil shahNo ratings yet

- Research and Development CostDocument17 pagesResearch and Development CostKaye Choraine NadumaNo ratings yet

- Topic 10 - Intangible AssetsDocument7 pagesTopic 10 - Intangible AssetsEki OmallaoNo ratings yet

- Solution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDocument22 pagesSolution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDouglasWhiteheadxkwi100% (49)

- AASI302 MidtermLesson2Document7 pagesAASI302 MidtermLesson2guerrerojamesssNo ratings yet

- Development Phase: Measurement Subsequent To AcquisitionDocument2 pagesDevelopment Phase: Measurement Subsequent To AcquisitionKatrizia AbadNo ratings yet

- IFRS CH 7 Intangible AssetsDocument3 pagesIFRS CH 7 Intangible Assetsa.adel87No ratings yet

- ch12 PDFDocument9 pagesch12 PDFEmma Mariz GarciaNo ratings yet

- As - 26 Intangible AssetsDocument37 pagesAs - 26 Intangible AssetsVijay BhattiNo ratings yet

- FAR 12 - Intangible AssetsDocument5 pagesFAR 12 - Intangible Assetsmrsjeon0501No ratings yet

- Week 7 SlidesDocument24 pagesWeek 7 Slideswali28936No ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- 6 Audit of Intangible Asset and Related Accounts Feu RevDocument5 pages6 Audit of Intangible Asset and Related Accounts Feu RevHanze MacasilNo ratings yet

- IAS 38 - IntangiblesDocument2 pagesIAS 38 - IntangiblesDawar Hussain (WT)No ratings yet

- ACCT245 ProjectDocument4 pagesACCT245 ProjectUsmanNo ratings yet

- Intangible AssetsDocument7 pagesIntangible AssetsRachell PabionaNo ratings yet

- Accounting For Assets, Impairments and GrantsDocument21 pagesAccounting For Assets, Impairments and GrantsSajid Iqbal100% (1)

- Ias 38Document2 pagesIas 38ξηεмψ шιτнιηNo ratings yet

- Last Hai PdfToWord - WordToPdf - Pagenumber PDFDocument216 pagesLast Hai PdfToWord - WordToPdf - Pagenumber PDFŞâh ŠůmiťNo ratings yet

- Performance Measures: Financial Measure Performance TechniquesDocument24 pagesPerformance Measures: Financial Measure Performance Techniquesmuttu2011No ratings yet

- The Gartner Cio Roadmap For Strategic Cost Optimization ExcerptDocument8 pagesThe Gartner Cio Roadmap For Strategic Cost Optimization Excerptamparito.acevedo6186No ratings yet

- Pas 38Document7 pagesPas 38elle friasNo ratings yet

- IAS 38 Intangible Assets PDFDocument3 pagesIAS 38 Intangible Assets PDFRICHARD GBAGONo ratings yet

- Accounting For Research and Development Costs: Statement of Accounting Standards March 1983Document11 pagesAccounting For Research and Development Costs: Statement of Accounting Standards March 1983Ade Irma HidayahNo ratings yet

- 2.PPT On Intangible AssetsDocument10 pages2.PPT On Intangible AssetsBhuvaneswari karuturiNo ratings yet

- Session 6 Assets Part 2 - Intangilbe and Investments (Marked Up)Document38 pagesSession 6 Assets Part 2 - Intangilbe and Investments (Marked Up)Kothari InvestmentsNo ratings yet

- FR - IAS 38 - CompleteDocument27 pagesFR - IAS 38 - CompleteahmadNo ratings yet

- Intangible AssetDocument38 pagesIntangible AssetRimissha Udenia 2No ratings yet

- 7 Scramble: Cost of UpgradingDocument4 pages7 Scramble: Cost of UpgradingMubashar HussainNo ratings yet

- Final AssignmentDocument6 pagesFinal AssignmentTalimur RahmanNo ratings yet

- Kaplan Ias 38 FinalDocument27 pagesKaplan Ias 38 FinalMahlet AbrahaNo ratings yet

- 6) Ias-38Document15 pages6) Ias-38manvi jainNo ratings yet

- Intangible Assets NotesDocument6 pagesIntangible Assets NotesRaizel RamirezNo ratings yet

- Lesson 3 AasiDocument5 pagesLesson 3 Aasidin matanguihanNo ratings yet

- Part D-9 Intangible Non-Current Assets (CH 07)Document21 pagesPart D-9 Intangible Non-Current Assets (CH 07)hyangNo ratings yet

- PROJECT STANDARDS AND SPECIFICATIONS Fesibiliy Studies Rev01.1Document13 pagesPROJECT STANDARDS AND SPECIFICATIONS Fesibiliy Studies Rev01.1Chika chukwonuNo ratings yet

- Chapter 04 Proj Change 1Document24 pagesChapter 04 Proj Change 1Dr Ricardo VincentNo ratings yet

- IAS 38 Intangible AssetsDocument4 pagesIAS 38 Intangible AssetsVikky BehNo ratings yet

- Unit 2Document14 pagesUnit 2ajinkyapolNo ratings yet

- Modern Systems Analysis and DesignDocument46 pagesModern Systems Analysis and Designcleverman677No ratings yet

- Modern Systems Analysis and DesignDocument46 pagesModern Systems Analysis and Designcleverman677No ratings yet

- AC 2101 CHAPTER 33 NotesDocument2 pagesAC 2101 CHAPTER 33 NotesChriz VillasNo ratings yet

- CASE STUDY ANALYSIS Assignment 2 Case - UnlockedDocument3 pagesCASE STUDY ANALYSIS Assignment 2 Case - Unlockedmandana.heidaria1166No ratings yet

- Nfjpia Nmbe Far 2017 Ans-1Document10 pagesNfjpia Nmbe Far 2017 Ans-1Stephen ChuaNo ratings yet

- Fakultas Ekonomi Universitas Pandjadjaran (Unpad) BandungDocument20 pagesFakultas Ekonomi Universitas Pandjadjaran (Unpad) BandungSalmiNo ratings yet

- Small Estate AffidavitDocument4 pagesSmall Estate Affidavitnickscribd01No ratings yet

- Kraft Pulp and Paper CoDocument2 pagesKraft Pulp and Paper CoFernando Treviño JuarezNo ratings yet

- SAP MM STO + P2P Part 1Document18 pagesSAP MM STO + P2P Part 1Harish KumarNo ratings yet

- DEll Value ChainDocument7 pagesDEll Value ChainStanley PakpahanNo ratings yet

- Dss 10Document47 pagesDss 10Om PrakashNo ratings yet

- GMAT Awa 109 SampleDocument90 pagesGMAT Awa 109 SampleMelissa GuzmanNo ratings yet

- Januvia Success StoryDocument16 pagesJanuvia Success StoryMedicinMan0% (1)

- Tax Invoice: Rekha Indane Gramin VITRAK (0000270706)Document2 pagesTax Invoice: Rekha Indane Gramin VITRAK (0000270706)sujeet sharmaNo ratings yet

- Declining SuratDocument34 pagesDeclining Suratvaishalitadvi053No ratings yet

- The Philippine Financial SystemDocument14 pagesThe Philippine Financial SystemAnonymous gJ6QEiNo ratings yet

- Case 1-1 Sources of GAAPDocument6 pagesCase 1-1 Sources of GAAPBella TjendriawanNo ratings yet

- Annual Career Guidance Advocacy Program (CgapDocument3 pagesAnnual Career Guidance Advocacy Program (CgapROGERNo ratings yet

- Recruitment & Selection of Incepta PharmaceuticalsDocument60 pagesRecruitment & Selection of Incepta PharmaceuticalsJhalak SauravNo ratings yet

- Honda HRDocument13 pagesHonda HRHarsh YadavNo ratings yet

- The Impact of ERP Systems On Firm and Business Process PerformanceDocument17 pagesThe Impact of ERP Systems On Firm and Business Process Performanceincrediblekashif7916No ratings yet

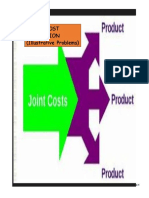

- Joint Cost Allocation-Illustrative ProblemsDocument4 pagesJoint Cost Allocation-Illustrative ProblemspamssyNo ratings yet

- Google, Red Hat, BlackBerry and Earthlink On Patent Trolls, PrivateeringDocument22 pagesGoogle, Red Hat, BlackBerry and Earthlink On Patent Trolls, PrivateeringRachel KingNo ratings yet

- Unit 4-Intro To Services MKTG - Price - Place - Jessy Nair - PESU - JN-MinorsDocument109 pagesUnit 4-Intro To Services MKTG - Price - Place - Jessy Nair - PESU - JN-MinorsJaya HarshitNo ratings yet

- BBP BrochureDocument2 pagesBBP BrochureTouqeer Ahmed KhanNo ratings yet

- Berkenkotter v. CADocument5 pagesBerkenkotter v. CAjealousmistressNo ratings yet

- Contract of LeaseDocument2 pagesContract of LeaseesormikNo ratings yet

- 1S16 IT Strategy - Week-1Document49 pages1S16 IT Strategy - Week-1S GDNo ratings yet

- Special Power of Attorney - BantasanDocument1 pageSpecial Power of Attorney - BantasanHazel-mae LabradaNo ratings yet

- Am Take Food Orders Provide Table Serv 180113Document70 pagesAm Take Food Orders Provide Table Serv 180113Mustafa TopeNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Write Two or Three Paragraphs in Which You Describe The Role That Culture Plays in The Development of A CountryDocument4 pagesWrite Two or Three Paragraphs in Which You Describe The Role That Culture Plays in The Development of A CountryVinnu KumarNo ratings yet

- Government Regulation 24/2012Document14 pagesGovernment Regulation 24/2012Adria SaputeroNo ratings yet

- Value Proposition Comparative AnalysisDocument8 pagesValue Proposition Comparative AnalysisNemesio Tejero, IIINo ratings yet

- 04 Ias 38Document4 pages04 Ias 38Irtiza AbbasNo ratings yet

- ACC702 Tutorial - Intangible AssetsDocument3 pagesACC702 Tutorial - Intangible AssetsUshra KhanNo ratings yet

- Audit of Intangible AssetsDocument8 pagesAudit of Intangible AssetsMikaela Graciel AnneNo ratings yet

- Intangible For Non-Current AssetsDocument55 pagesIntangible For Non-Current AssetsChitta LeeNo ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- Intagible Asset 1 1Document13 pagesIntagible Asset 1 1Trina Rose FandiñoNo ratings yet

- Intangible AssetsDocument1 pageIntangible Assetsarmor.coverNo ratings yet

- #23 Intangible Assets (Notes For 6208)Document6 pages#23 Intangible Assets (Notes For 6208)jaysonNo ratings yet

- Research & Development Tax Concession: Discussion SessionDocument18 pagesResearch & Development Tax Concession: Discussion SessionnugosuNo ratings yet

- Fresh BeginningsDocument3 pagesFresh BeginningsALIEVALINo ratings yet

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- Intangible AssetsDocument6 pagesIntangible AssetsChris tine Mae MendozaNo ratings yet

- Miafe B. Almendralejo BSA - 2 Intermediate Accounting 1 2 Sem 2021-22 Discussion (Chapter 33)Document4 pagesMiafe B. Almendralejo BSA - 2 Intermediate Accounting 1 2 Sem 2021-22 Discussion (Chapter 33)Miafe B. AlmendralejoNo ratings yet

- Ias 38 Intangible AssetsDocument4 pagesIas 38 Intangible AssetsYogesh BhattaraiNo ratings yet

- IFRS Development Costs Recognition PDFDocument3 pagesIFRS Development Costs Recognition PDFmizarkoNo ratings yet

- CIPFA PPT Template NEW IPFM PSFR Session 4Document57 pagesCIPFA PPT Template NEW IPFM PSFR Session 4SabNo ratings yet

- F3 - ACCA Chapter-9-1Document15 pagesF3 - ACCA Chapter-9-1Nile NguyenNo ratings yet

- Question 6: Ias 38 Intangible Assets: Page 1 of 2Document2 pagesQuestion 6: Ias 38 Intangible Assets: Page 1 of 2tazil shahNo ratings yet

- Research and Development CostDocument17 pagesResearch and Development CostKaye Choraine NadumaNo ratings yet

- Topic 10 - Intangible AssetsDocument7 pagesTopic 10 - Intangible AssetsEki OmallaoNo ratings yet

- Solution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDocument22 pagesSolution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDouglasWhiteheadxkwi100% (49)

- AASI302 MidtermLesson2Document7 pagesAASI302 MidtermLesson2guerrerojamesssNo ratings yet

- Development Phase: Measurement Subsequent To AcquisitionDocument2 pagesDevelopment Phase: Measurement Subsequent To AcquisitionKatrizia AbadNo ratings yet

- IFRS CH 7 Intangible AssetsDocument3 pagesIFRS CH 7 Intangible Assetsa.adel87No ratings yet

- ch12 PDFDocument9 pagesch12 PDFEmma Mariz GarciaNo ratings yet

- As - 26 Intangible AssetsDocument37 pagesAs - 26 Intangible AssetsVijay BhattiNo ratings yet

- FAR 12 - Intangible AssetsDocument5 pagesFAR 12 - Intangible Assetsmrsjeon0501No ratings yet

- Week 7 SlidesDocument24 pagesWeek 7 Slideswali28936No ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- 6 Audit of Intangible Asset and Related Accounts Feu RevDocument5 pages6 Audit of Intangible Asset and Related Accounts Feu RevHanze MacasilNo ratings yet

- IAS 38 - IntangiblesDocument2 pagesIAS 38 - IntangiblesDawar Hussain (WT)No ratings yet

- ACCT245 ProjectDocument4 pagesACCT245 ProjectUsmanNo ratings yet

- Intangible AssetsDocument7 pagesIntangible AssetsRachell PabionaNo ratings yet

- Accounting For Assets, Impairments and GrantsDocument21 pagesAccounting For Assets, Impairments and GrantsSajid Iqbal100% (1)

- Ias 38Document2 pagesIas 38ξηεмψ шιτнιηNo ratings yet

- Last Hai PdfToWord - WordToPdf - Pagenumber PDFDocument216 pagesLast Hai PdfToWord - WordToPdf - Pagenumber PDFŞâh ŠůmiťNo ratings yet

- Performance Measures: Financial Measure Performance TechniquesDocument24 pagesPerformance Measures: Financial Measure Performance Techniquesmuttu2011No ratings yet

- The Gartner Cio Roadmap For Strategic Cost Optimization ExcerptDocument8 pagesThe Gartner Cio Roadmap For Strategic Cost Optimization Excerptamparito.acevedo6186No ratings yet

- Pas 38Document7 pagesPas 38elle friasNo ratings yet

- IAS 38 Intangible Assets PDFDocument3 pagesIAS 38 Intangible Assets PDFRICHARD GBAGONo ratings yet

- Accounting For Research and Development Costs: Statement of Accounting Standards March 1983Document11 pagesAccounting For Research and Development Costs: Statement of Accounting Standards March 1983Ade Irma HidayahNo ratings yet

- 2.PPT On Intangible AssetsDocument10 pages2.PPT On Intangible AssetsBhuvaneswari karuturiNo ratings yet

- Session 6 Assets Part 2 - Intangilbe and Investments (Marked Up)Document38 pagesSession 6 Assets Part 2 - Intangilbe and Investments (Marked Up)Kothari InvestmentsNo ratings yet

- FR - IAS 38 - CompleteDocument27 pagesFR - IAS 38 - CompleteahmadNo ratings yet

- Intangible AssetDocument38 pagesIntangible AssetRimissha Udenia 2No ratings yet

- 7 Scramble: Cost of UpgradingDocument4 pages7 Scramble: Cost of UpgradingMubashar HussainNo ratings yet

- Final AssignmentDocument6 pagesFinal AssignmentTalimur RahmanNo ratings yet

- Kaplan Ias 38 FinalDocument27 pagesKaplan Ias 38 FinalMahlet AbrahaNo ratings yet

- 6) Ias-38Document15 pages6) Ias-38manvi jainNo ratings yet

- Intangible Assets NotesDocument6 pagesIntangible Assets NotesRaizel RamirezNo ratings yet

- Lesson 3 AasiDocument5 pagesLesson 3 Aasidin matanguihanNo ratings yet

- Part D-9 Intangible Non-Current Assets (CH 07)Document21 pagesPart D-9 Intangible Non-Current Assets (CH 07)hyangNo ratings yet

- PROJECT STANDARDS AND SPECIFICATIONS Fesibiliy Studies Rev01.1Document13 pagesPROJECT STANDARDS AND SPECIFICATIONS Fesibiliy Studies Rev01.1Chika chukwonuNo ratings yet

- Chapter 04 Proj Change 1Document24 pagesChapter 04 Proj Change 1Dr Ricardo VincentNo ratings yet

- IAS 38 Intangible AssetsDocument4 pagesIAS 38 Intangible AssetsVikky BehNo ratings yet

- Unit 2Document14 pagesUnit 2ajinkyapolNo ratings yet

- Modern Systems Analysis and DesignDocument46 pagesModern Systems Analysis and Designcleverman677No ratings yet

- Modern Systems Analysis and DesignDocument46 pagesModern Systems Analysis and Designcleverman677No ratings yet

- AC 2101 CHAPTER 33 NotesDocument2 pagesAC 2101 CHAPTER 33 NotesChriz VillasNo ratings yet

- CASE STUDY ANALYSIS Assignment 2 Case - UnlockedDocument3 pagesCASE STUDY ANALYSIS Assignment 2 Case - Unlockedmandana.heidaria1166No ratings yet

- Nfjpia Nmbe Far 2017 Ans-1Document10 pagesNfjpia Nmbe Far 2017 Ans-1Stephen ChuaNo ratings yet

- Fakultas Ekonomi Universitas Pandjadjaran (Unpad) BandungDocument20 pagesFakultas Ekonomi Universitas Pandjadjaran (Unpad) BandungSalmiNo ratings yet

- Small Estate AffidavitDocument4 pagesSmall Estate Affidavitnickscribd01No ratings yet

- Kraft Pulp and Paper CoDocument2 pagesKraft Pulp and Paper CoFernando Treviño JuarezNo ratings yet

- SAP MM STO + P2P Part 1Document18 pagesSAP MM STO + P2P Part 1Harish KumarNo ratings yet

- DEll Value ChainDocument7 pagesDEll Value ChainStanley PakpahanNo ratings yet

- Dss 10Document47 pagesDss 10Om PrakashNo ratings yet

- GMAT Awa 109 SampleDocument90 pagesGMAT Awa 109 SampleMelissa GuzmanNo ratings yet

- Januvia Success StoryDocument16 pagesJanuvia Success StoryMedicinMan0% (1)

- Tax Invoice: Rekha Indane Gramin VITRAK (0000270706)Document2 pagesTax Invoice: Rekha Indane Gramin VITRAK (0000270706)sujeet sharmaNo ratings yet

- Declining SuratDocument34 pagesDeclining Suratvaishalitadvi053No ratings yet

- The Philippine Financial SystemDocument14 pagesThe Philippine Financial SystemAnonymous gJ6QEiNo ratings yet

- Case 1-1 Sources of GAAPDocument6 pagesCase 1-1 Sources of GAAPBella TjendriawanNo ratings yet

- Annual Career Guidance Advocacy Program (CgapDocument3 pagesAnnual Career Guidance Advocacy Program (CgapROGERNo ratings yet

- Recruitment & Selection of Incepta PharmaceuticalsDocument60 pagesRecruitment & Selection of Incepta PharmaceuticalsJhalak SauravNo ratings yet

- Honda HRDocument13 pagesHonda HRHarsh YadavNo ratings yet

- The Impact of ERP Systems On Firm and Business Process PerformanceDocument17 pagesThe Impact of ERP Systems On Firm and Business Process Performanceincrediblekashif7916No ratings yet

- Joint Cost Allocation-Illustrative ProblemsDocument4 pagesJoint Cost Allocation-Illustrative ProblemspamssyNo ratings yet

- Google, Red Hat, BlackBerry and Earthlink On Patent Trolls, PrivateeringDocument22 pagesGoogle, Red Hat, BlackBerry and Earthlink On Patent Trolls, PrivateeringRachel KingNo ratings yet

- Unit 4-Intro To Services MKTG - Price - Place - Jessy Nair - PESU - JN-MinorsDocument109 pagesUnit 4-Intro To Services MKTG - Price - Place - Jessy Nair - PESU - JN-MinorsJaya HarshitNo ratings yet

- BBP BrochureDocument2 pagesBBP BrochureTouqeer Ahmed KhanNo ratings yet

- Berkenkotter v. CADocument5 pagesBerkenkotter v. CAjealousmistressNo ratings yet

- Contract of LeaseDocument2 pagesContract of LeaseesormikNo ratings yet

- 1S16 IT Strategy - Week-1Document49 pages1S16 IT Strategy - Week-1S GDNo ratings yet

- Special Power of Attorney - BantasanDocument1 pageSpecial Power of Attorney - BantasanHazel-mae LabradaNo ratings yet

- Am Take Food Orders Provide Table Serv 180113Document70 pagesAm Take Food Orders Provide Table Serv 180113Mustafa TopeNo ratings yet