Download as pptx, pdf, or txt

You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)Rating: 5 out of 5 stars5/5 (1)

- B326 TMA 23-24 (Fall) V1Document5 pagesB326 TMA 23-24 (Fall) V1adel.dahbour9733% (3)

- HW - Third AttemptDocument49 pagesHW - Third AttemptRolando GrayNo ratings yet

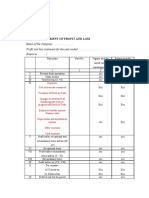

- Vertical Format: Format of Income Statement ParticularsDocument4 pagesVertical Format: Format of Income Statement ParticularsAnjali Betala Kothari100% (1)

- Afa CompilationDocument36 pagesAfa CompilationAnkur ChowdharyNo ratings yet

- Unit 02 Preparation of Financial Statement As Per IND AS 01Document13 pagesUnit 02 Preparation of Financial Statement As Per IND AS 01Deepak LNo ratings yet

- FormatDocument3 pagesFormatCharles RussellNo ratings yet

- Introduction To Corporate FinanceDocument18 pagesIntroduction To Corporate FinanceGauri SinglaNo ratings yet

- NCERT Solutions For Class 11 Accountancy Chapter 10 Financial Statements - 2Document90 pagesNCERT Solutions For Class 11 Accountancy Chapter 10 Financial Statements - 2Badal singh ThakurNo ratings yet

- selfstudys_com_file (8)Document37 pagesselfstudys_com_file (8)khushbooraghani11No ratings yet

- Chapter 21 IAS 1Document4 pagesChapter 21 IAS 1Chandan SamalNo ratings yet

- Statement of Profit and Loss (As Per Division I of Schedule Iii)Document7 pagesStatement of Profit and Loss (As Per Division I of Schedule Iii)Yash GoyalNo ratings yet

- 06 Handout 1Document19 pages06 Handout 1Johnlloyd CahuloganNo ratings yet

- Financial Accounting: Accounting - Process of Identifying, Measuring, and Communicating EconomicDocument7 pagesFinancial Accounting: Accounting - Process of Identifying, Measuring, and Communicating EconomicKyle Daniel PimentelNo ratings yet

- Management Accounting Unit-2Document9 pagesManagement Accounting Unit-2prof.hpk18No ratings yet

- Vertical Balance SheetDocument14 pagesVertical Balance Sheetabhi82% (11)

- Financial Statements and Disclosure of InformationDocument7 pagesFinancial Statements and Disclosure of InformationAjit PatilNo ratings yet

- Income StatementDocument5 pagesIncome Statementrramandeep773No ratings yet

- Unit IDocument10 pagesUnit IsoundarpandiyanNo ratings yet

- CompanyDocument4 pagesCompanyparwez_0505No ratings yet

- Name of The Company . Profit and Loss Statement For The Year EndedDocument7 pagesName of The Company . Profit and Loss Statement For The Year EndedAnitha RNo ratings yet

- Cash Flow Statement Ias 7Document5 pagesCash Flow Statement Ias 7JOSEPH LUBEMBANo ratings yet

- Cash Flow StatementDocument36 pagesCash Flow StatementNAVYA MITTAL 2224070No ratings yet

- Pre Reading Material For Session 17 FA (Cash Flow)Document10 pagesPre Reading Material For Session 17 FA (Cash Flow)Rohit Roy100% (1)

- Cash Flow StatementDocument19 pagesCash Flow StatementCharu100% (1)

- R.Kanchanamala: Faculty Member IibfDocument74 pagesR.Kanchanamala: Faculty Member Iibfmithilesh tabhaneNo ratings yet

- Final Accounts of Company Format of Balance Sheet Particulars Sch. No. Rs. RsDocument3 pagesFinal Accounts of Company Format of Balance Sheet Particulars Sch. No. Rs. Rshem2_3No ratings yet

- Lecture 1 Understanding Financial StatementsDocument38 pagesLecture 1 Understanding Financial Statementsdev guptaNo ratings yet

- Accounting For Banks and Other Similar InstitutionsDocument9 pagesAccounting For Banks and Other Similar InstitutionsKenyan GNo ratings yet

- Term 1 Part BDocument47 pagesTerm 1 Part BFitness ChiselersNo ratings yet

- As 17Document6 pagesAs 17abhishekkapse654No ratings yet

- Cash Flow Statements6Document28 pagesCash Flow Statements6kimuli FreddieNo ratings yet

- Notes Cash FlowDocument16 pagesNotes Cash FlowsamundeswaryNo ratings yet

- Preparation of Published Financial StatementsDocument46 pagesPreparation of Published Financial StatementsBenard Bett100% (2)

- Income From Business TheoryDocument5 pagesIncome From Business TheoryYashin Y HNo ratings yet

- Financial Statement AnalysisDocument46 pagesFinancial Statement AnalysisMusom BBANo ratings yet

- Lecture 3Document14 pagesLecture 3Lol 123No ratings yet

- Fund Flow:: Working CapitalDocument19 pagesFund Flow:: Working CapitalAlex JayachandranNo ratings yet

- Accounting FormatsDocument21 pagesAccounting FormatsAsima ZubairNo ratings yet

- FSs For CompaniesDocument9 pagesFSs For CompaniesFarid UddinNo ratings yet

- Funds Flow Statement FormatDocument2 pagesFunds Flow Statement FormatBheemeswar ReddyNo ratings yet

- Business FinanceDocument6 pagesBusiness FinanceHassan AbdullahNo ratings yet

- CFM 221 2023 Capital Budgets NotesDocument19 pagesCFM 221 2023 Capital Budgets NotesChantell KatlegoNo ratings yet

- Acc TestDocument3 pagesAcc Testsk23skNo ratings yet

- ICAI FoundationDocument16 pagesICAI Foundationbullalulla840No ratings yet

- Advanced AccountingDocument372 pagesAdvanced AccountingNidhi ShahNo ratings yet

- Cash Flow StatementDocument16 pagesCash Flow Statementrajesh337masssNo ratings yet

- Cash Flow Statement Mcqs With AnswerDocument25 pagesCash Flow Statement Mcqs With Answermahesh patilNo ratings yet

- Quarterly Information System - Form IDocument2 pagesQuarterly Information System - Form IRavindra ReddyNo ratings yet

- Cash Flow Statement: by B.K.VashishthaDocument20 pagesCash Flow Statement: by B.K.VashishthaNadya Shamini100% (1)

- Financial - Statement Reporting-IIDocument29 pagesFinancial - Statement Reporting-IIAshwini KhareNo ratings yet

- Preparation of Published Financial StatementsDocument19 pagesPreparation of Published Financial StatementsRuth Nyawira100% (1)

- Company Final AccountsDocument13 pagesCompany Final Accountsshanthala mNo ratings yet

- CFS - Accountancy - Grade 12 - Session 10Document62 pagesCFS - Accountancy - Grade 12 - Session 10Nirav Sheth100% (1)

- Institute-University School of Business Department-MbaDocument13 pagesInstitute-University School of Business Department-MbaAbhishek kumarNo ratings yet

- Cash Flow StatementDocument5 pagesCash Flow StatementDebaditya SenguptaNo ratings yet

- Dr. Ajay Dwivedi Professor Department of Financial StudiesDocument16 pagesDr. Ajay Dwivedi Professor Department of Financial StudiesKaran Pratap Singh100% (1)

- Corporate Accounting I Module IIIDocument6 pagesCorporate Accounting I Module III2vj77sn8x5No ratings yet

- Quarterly Information System - Form II: Performance During The Quarter Ended:.................Document2 pagesQuarterly Information System - Form II: Performance During The Quarter Ended:.................Ravindra ReddyNo ratings yet

- Part Ii - Statement of Profit and LossDocument3 pagesPart Ii - Statement of Profit and LossSaumyajit DeyNo ratings yet

- Financial Accounting Topic FiveDocument14 pagesFinancial Accounting Topic FiveGABRIEL KAMAU KUNG'UNo ratings yet

- CAPE Accounting 2007 U1 P2Document7 pagesCAPE Accounting 2007 U1 P2preshNo ratings yet

- Dabur Standalone Balance SheetDocument1 pageDabur Standalone Balance SheetVIJAY KUMARNo ratings yet

- IFRS 3 Business CombinationsDocument17 pagesIFRS 3 Business CombinationsGround ZeroNo ratings yet

- AFAR Preweek Lecture Part 2Document18 pagesAFAR Preweek Lecture Part 2Joris YapNo ratings yet

- Viewing Business Through The Lens of Financial StatementsDocument55 pagesViewing Business Through The Lens of Financial StatementsAkib Mahbub KhanNo ratings yet

- Personal Assigment PDFDocument13 pagesPersonal Assigment PDFImran Azizi Zulkifli67% (3)

- Accounting Concept and Principle QuizDocument2 pagesAccounting Concept and Principle QuizkristelNo ratings yet

- 07 Analyzing Business Transactions of A Service EntityDocument4 pages07 Analyzing Business Transactions of A Service EntityRewsEnNo ratings yet

- TOA Quizzer 2 - Conceptual FrameworkDocument13 pagesTOA Quizzer 2 - Conceptual FrameworkmarkNo ratings yet

- AISAE 103 Module 1 Lesson 1 To 3Document36 pagesAISAE 103 Module 1 Lesson 1 To 3Mariel Mae MoralesNo ratings yet

- Conceptual Framework of Cash FlowDocument19 pagesConceptual Framework of Cash FlowAkshit Sandooja0% (1)

- Chapter 6Document45 pagesChapter 6Ishan Kapoor100% (1)

- Handouts ACCOUNTING-2Document39 pagesHandouts ACCOUNTING-2Marc John IlanoNo ratings yet

- Summary of Important Us Gaap:: Under US GAAP, The Financial Statements Include TheDocument28 pagesSummary of Important Us Gaap:: Under US GAAP, The Financial Statements Include TheSangram PandaNo ratings yet

- COA FormulaDocument2 pagesCOA Formulakcent236No ratings yet

- Ppe 1Document5 pagesPpe 1Nykee PenNo ratings yet

- Analisis Penerapan PSAK No.16 Dalam Perlakuan Akuntansi Aset Tetap PerusahaanDocument10 pagesAnalisis Penerapan PSAK No.16 Dalam Perlakuan Akuntansi Aset Tetap PerusahaanNurlaili RomadhaniNo ratings yet

- Company Law Unit-IVDocument16 pagesCompany Law Unit-IVKaran Veer Singh100% (1)

- AFAR-01 PartnershipDocument6 pagesAFAR-01 PartnershipRamainne Ronquillo0% (1)

- Afar Partnership LiquidationDocument42 pagesAfar Partnership LiquidationKrizia Mae Uzielle PeneroNo ratings yet

- Ratio Analysis of TATA MOTORSDocument8 pagesRatio Analysis of TATA MOTORSmr_anderson47100% (8)

- Test Bank Accounting For Partnerships PDFDocument49 pagesTest Bank Accounting For Partnerships PDFRose Vanessa BurceNo ratings yet

- AttachmentDocument8 pagesAttachmentchintya milathania100% (1)

- Dwnload Full Corporate Finance Canadian 2nd Edition Berk Test Bank PDFDocument12 pagesDwnload Full Corporate Finance Canadian 2nd Edition Berk Test Bank PDFgoblinerentageb0rls7100% (19)

- 6gbr 2006 Dec QDocument9 pages6gbr 2006 Dec Qapi-19836745No ratings yet

- AI - Materi 9 Analisis LK InternasDocument21 pagesAI - Materi 9 Analisis LK Internasbams_febNo ratings yet

- MM Due Diligence Startups ChecklistDocument5 pagesMM Due Diligence Startups ChecklistpriyawanshNo ratings yet

- Item No. 23 Teresita BuenaflorDocument14 pagesItem No. 23 Teresita BuenaflorXiaoNo ratings yet