Cfin5 PPT Chapter 14

Cfin5 PPT Chapter 14

You might also like

- Bank StatementDocument4 pagesBank StatementKenny Nam50% (2)

- Working Capital Management - BrighamDocument34 pagesWorking Capital Management - BrighamAldrin ZolinaNo ratings yet

- TitleMax E-Commerce CreditDocument30 pagesTitleMax E-Commerce Creditklassiq100% (1)

- Financial Statement Analysis: Charles H. GibsonDocument22 pagesFinancial Statement Analysis: Charles H. GibsonGud BooyNo ratings yet

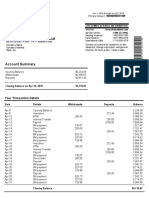

- Account Summary: Your Transaction DetailsDocument1 pageAccount Summary: Your Transaction Detailsdelfa100% (1)

- SMB18 e CH 22Document40 pagesSMB18 e CH 22Bantilan ElejunNo ratings yet

- Survey8e Ch01 InstructorDocument45 pagesSurvey8e Ch01 InstructorAndrew DameNo ratings yet

- Course: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit CollectionDocument27 pagesCourse: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit Collectionsalsabilla rpNo ratings yet

- Lec 4Document33 pagesLec 4Mohamed AliNo ratings yet

- Workingcapitalmanagement 120729142538 Phpapp01Document32 pagesWorkingcapitalmanagement 120729142538 Phpapp01Vikas BansalNo ratings yet

- Working Capital ManagementDocument25 pagesWorking Capital ManagementJaveria LeghariNo ratings yet

- 1.1 IISc SAP S4HANA TRM Overall Concept Presentation V 1.0Document44 pages1.1 IISc SAP S4HANA TRM Overall Concept Presentation V 1.0Ravi KurubaNo ratings yet

- Chapter 16 - Activities01Document27 pagesChapter 16 - Activities01Alex GuNo ratings yet

- Financial Markets and Institutions: Abridged 11 EditionDocument38 pagesFinancial Markets and Institutions: Abridged 11 Editionsaif khanNo ratings yet

- Working Capital Management: Dr. Arti Chandani, Associate Professor, SIMSDocument19 pagesWorking Capital Management: Dr. Arti Chandani, Associate Professor, SIMSHimanshu DuttaNo ratings yet

- Working Capital MGMT Practice Manual PDFDocument75 pagesWorking Capital MGMT Practice Manual PDFPankaj PandeyNo ratings yet

- AGibson 13E Ch10Document24 pagesAGibson 13E Ch10finance tutorNo ratings yet

- Week 6Document29 pagesWeek 6Lovepreet malhiNo ratings yet

- Capital Budgeting Techniques SlidesDocument36 pagesCapital Budgeting Techniques SlidesAryan ShahNo ratings yet

- PK14 NotesDocument22 pagesPK14 NotesContessa PetriniNo ratings yet

- FSA Ch10 Cashflow StatementDocument26 pagesFSA Ch10 Cashflow StatementazzaNo ratings yet

- Working Capital ManagementDocument45 pagesWorking Capital Managementvini2710No ratings yet

- TM5 Small Business ManagementDocument39 pagesTM5 Small Business ManagementHilyah Hana KeyNo ratings yet

- Dirección Financiera - Semana 2Document8 pagesDirección Financiera - Semana 2yessNo ratings yet

- Part 3 - Understanding Financial Statements and ReportsDocument7 pagesPart 3 - Understanding Financial Statements and ReportsJeanrey AlcantaraNo ratings yet

- Financial Statement Analysis: Charles H. GibsonDocument38 pagesFinancial Statement Analysis: Charles H. GibsonmohamedNo ratings yet

- EFM4, CH 17, Slides, 07-02-18Document34 pagesEFM4, CH 17, Slides, 07-02-18Nicholas Malvin SaputraNo ratings yet

- Week 12 13Document36 pagesWeek 12 13shani2010No ratings yet

- Chap 1Document32 pagesChap 1Trần Lê NaNo ratings yet

- 01-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesDocument60 pages01-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesThanh ThùyNo ratings yet

- 82 Working Capital ManagementDocument25 pages82 Working Capital ManagementPrashant SharmaNo ratings yet

- Sesi 12-Working Capital ManagementDocument33 pagesSesi 12-Working Capital Managementdias khairunnisaNo ratings yet

- Principles of Working CapitalDocument24 pagesPrinciples of Working CapitalAnuj VyasNo ratings yet

- Introduction and Working Capital ManagementDocument4 pagesIntroduction and Working Capital Managementmh bachooNo ratings yet

- FMP Lecture - Working CapitalDocument31 pagesFMP Lecture - Working CapitalFatima ZehraNo ratings yet

- Financial Statement Analysis: Charles H. GibsonDocument26 pagesFinancial Statement Analysis: Charles H. GibsonGud BooyNo ratings yet

- Working Capital ManagementDocument22 pagesWorking Capital Managementkelvin pogiNo ratings yet

- Working Capital ManagementDocument20 pagesWorking Capital ManagementHaardik GandhiNo ratings yet

- CH 2Document42 pagesCH 2koukifou4No ratings yet

- Working Capital ManagementDocument34 pagesWorking Capital ManagementAnna WilliamsNo ratings yet

- Chapter-3 - Working Capital MGTDocument57 pagesChapter-3 - Working Capital MGTRaunak YadavNo ratings yet

- AGibson 13E Ch10Document24 pagesAGibson 13E Ch10finance tutorNo ratings yet

- Financial ProjectDocument8 pagesFinancial ProjectShekibaNo ratings yet

- Module 1-1Document6 pagesModule 1-1shejal naikNo ratings yet

- AGibson 13E Ch10Document25 pagesAGibson 13E Ch10Ihab Al-AnabousiNo ratings yet

- Exploring The World of Business and EconomicsDocument53 pagesExploring The World of Business and EconomicsLalaNo ratings yet

- Ifrs15 Are You Good To Go ConstructionDocument19 pagesIfrs15 Are You Good To Go ConstructionbatuchemNo ratings yet

- Financial Accounting Module 6 SummaryDocument6 pagesFinancial Accounting Module 6 SummaryKashika LathNo ratings yet

- Liquidity of Short-Term Assets - Related Debt-Paying AbilityDocument48 pagesLiquidity of Short-Term Assets - Related Debt-Paying AbilityJuan LeonardoNo ratings yet

- Working Capital ManagementDocument20 pagesWorking Capital Managementsmwanginet7No ratings yet

- FSA - Ch06 - Liquidity of Short-Term Assets Related Debt-Paying AbilityDocument46 pagesFSA - Ch06 - Liquidity of Short-Term Assets Related Debt-Paying AbilityAmine AbdesmadNo ratings yet

- FM Week 13Document35 pagesFM Week 13shaikhsafwan7788No ratings yet

- Business FinanceDocument10 pagesBusiness FinanceLisaNo ratings yet

- Mergers & Acquisitions Basics: IFLP Boot Camp May 16, 2018Document59 pagesMergers & Acquisitions Basics: IFLP Boot Camp May 16, 2018Soumya KesharwaniNo ratings yet

- Financial Analysis Using RatiosDocument12 pagesFinancial Analysis Using Ratiossamar RamadanNo ratings yet

- Financial Statement Analysis: by Uditha JayasingheDocument19 pagesFinancial Statement Analysis: by Uditha JayasinghesanjuladasanNo ratings yet

- Working Capital ManagementDocument34 pagesWorking Capital ManagementNirmal ShresthaNo ratings yet

- Module 3 P1&2 Evol. of Intl. Business Gfd23Document30 pagesModule 3 P1&2 Evol. of Intl. Business Gfd23Kristian UyNo ratings yet

- Businessfinance12 q3 Mod4 FINAL PDFDocument13 pagesBusinessfinance12 q3 Mod4 FINAL PDFJoyce Anne ManzanilloNo ratings yet

- Financial Statement Analysis Using RatiosDocument11 pagesFinancial Statement Analysis Using RatiosRobin LlagunoNo ratings yet

- Working CapitalDocument111 pagesWorking Capitalshehjadi918No ratings yet

- Working Capital Management: Dr. Gurendra Nath BhardwajDocument48 pagesWorking Capital Management: Dr. Gurendra Nath BhardwajPrashant TyagiNo ratings yet

- Super7 Operations: The Next Step for Lean in Financial ServicesFrom EverandSuper7 Operations: The Next Step for Lean in Financial ServicesNo ratings yet

- Digital Banking - ISEI - 210722Document38 pagesDigital Banking - ISEI - 210722nora lizaNo ratings yet

- Global Money Dispatch: WarnedDocument4 pagesGlobal Money Dispatch: WarnedViolin_Man100% (1)

- 2017-07-01 10.02PM Email Trent To Schneider Re. PMT.Document3 pages2017-07-01 10.02PM Email Trent To Schneider Re. PMT.larry-612445No ratings yet

- Working Capital Management-Accounts Payable and Receivable: Margarita KouloumbriDocument30 pagesWorking Capital Management-Accounts Payable and Receivable: Margarita KouloumbriInga ȚîgaiNo ratings yet

- IFC History Book Second EditionDocument144 pagesIFC History Book Second EditionMinh Binh PhamNo ratings yet

- F 39343900 ngs0404 30-11-2022 30112022 134801Document1 pageF 39343900 ngs0404 30-11-2022 30112022 134801Reta BulardaNo ratings yet

- Fundamental Accounting Principles 24th Edition Wild Solutions ManualDocument10 pagesFundamental Accounting Principles 24th Edition Wild Solutions Manualeffigiesbuffoonmwve9100% (29)

- 16 MB Liquidity Ratio'sDocument22 pages16 MB Liquidity Ratio'sKrrishna Rajesh TOKARAWATNo ratings yet

- Personal Finance SyllabusDocument3 pagesPersonal Finance SyllabusLigia LandowNo ratings yet

- Chapter 2 AccountingDocument12 pagesChapter 2 Accountingmoon loverNo ratings yet

- Delegation of Loaning Powers in UbiDocument2 pagesDelegation of Loaning Powers in UbiShradha KhandareNo ratings yet

- Origin of TransactionDocument7 pagesOrigin of TransactionrudraNo ratings yet

- Business Banking Price ListDocument15 pagesBusiness Banking Price ListSARFRAZ ALINo ratings yet

- T24 System Build - Core V1.0Document30 pagesT24 System Build - Core V1.0Quoc Dat TranNo ratings yet

- BankingLaws BEQDocument7 pagesBankingLaws BEQAnastasia ZaitsevNo ratings yet

- Secrecy of Bank Deposits ActDocument7 pagesSecrecy of Bank Deposits ActJohn Churchill Gil SaducosNo ratings yet

- BSA 3-4 - Quiz 1 - Group 3Document7 pagesBSA 3-4 - Quiz 1 - Group 3Jornel MandiaNo ratings yet

- Faqs On Internet Banking Services (Ibs) For NrisDocument2 pagesFaqs On Internet Banking Services (Ibs) For NrisABMNo ratings yet

- DATA ANALYSIS AND INTERPRETATION of Rain Bow PipesDocument10 pagesDATA ANALYSIS AND INTERPRETATION of Rain Bow Pipesarmeena falakNo ratings yet

- Credit Card StatementDocument3 pagesCredit Card StatementSayan GhoshNo ratings yet

- Handbook On CTS Clearing For BranchesDocument30 pagesHandbook On CTS Clearing For BranchesparthaNo ratings yet

- Danta Health Bank Statement 06.30.10Document7 pagesDanta Health Bank Statement 06.30.10Md. Mahabubur rahamanNo ratings yet

- Statement 2022 8Document4 pagesStatement 2022 8wconceptouNo ratings yet

- Shriram Transport Finance Company Ltd. - Initiating Coverage - 30032021Document12 pagesShriram Transport Finance Company Ltd. - Initiating Coverage - 30032021Devarsh VakilNo ratings yet

- Standard Chartered PLC Is A British Multinational BankingDocument8 pagesStandard Chartered PLC Is A British Multinational Bankingaditya saiNo ratings yet

- Strawman DeceptionDocument11 pagesStrawman DeceptionGrey WolfNo ratings yet

- What Is A Bank Identification Number (BIN), and HDocument1 pageWhat Is A Bank Identification Number (BIN), and HYogeshwaran.sNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Bank StatementDocument4 pagesBank StatementKenny Nam50% (2)

- Working Capital Management - BrighamDocument34 pagesWorking Capital Management - BrighamAldrin ZolinaNo ratings yet

- TitleMax E-Commerce CreditDocument30 pagesTitleMax E-Commerce Creditklassiq100% (1)

- Financial Statement Analysis: Charles H. GibsonDocument22 pagesFinancial Statement Analysis: Charles H. GibsonGud BooyNo ratings yet

- Account Summary: Your Transaction DetailsDocument1 pageAccount Summary: Your Transaction Detailsdelfa100% (1)

- SMB18 e CH 22Document40 pagesSMB18 e CH 22Bantilan ElejunNo ratings yet

- Survey8e Ch01 InstructorDocument45 pagesSurvey8e Ch01 InstructorAndrew DameNo ratings yet

- Course: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit CollectionDocument27 pagesCourse: FINC6001 Effective Period: September2019: Managing Cash Flow, Sales Collection, Credit Collectionsalsabilla rpNo ratings yet

- Lec 4Document33 pagesLec 4Mohamed AliNo ratings yet

- Workingcapitalmanagement 120729142538 Phpapp01Document32 pagesWorkingcapitalmanagement 120729142538 Phpapp01Vikas BansalNo ratings yet

- Working Capital ManagementDocument25 pagesWorking Capital ManagementJaveria LeghariNo ratings yet

- 1.1 IISc SAP S4HANA TRM Overall Concept Presentation V 1.0Document44 pages1.1 IISc SAP S4HANA TRM Overall Concept Presentation V 1.0Ravi KurubaNo ratings yet

- Chapter 16 - Activities01Document27 pagesChapter 16 - Activities01Alex GuNo ratings yet

- Financial Markets and Institutions: Abridged 11 EditionDocument38 pagesFinancial Markets and Institutions: Abridged 11 Editionsaif khanNo ratings yet

- Working Capital Management: Dr. Arti Chandani, Associate Professor, SIMSDocument19 pagesWorking Capital Management: Dr. Arti Chandani, Associate Professor, SIMSHimanshu DuttaNo ratings yet

- Working Capital MGMT Practice Manual PDFDocument75 pagesWorking Capital MGMT Practice Manual PDFPankaj PandeyNo ratings yet

- AGibson 13E Ch10Document24 pagesAGibson 13E Ch10finance tutorNo ratings yet

- Week 6Document29 pagesWeek 6Lovepreet malhiNo ratings yet

- Capital Budgeting Techniques SlidesDocument36 pagesCapital Budgeting Techniques SlidesAryan ShahNo ratings yet

- PK14 NotesDocument22 pagesPK14 NotesContessa PetriniNo ratings yet

- FSA Ch10 Cashflow StatementDocument26 pagesFSA Ch10 Cashflow StatementazzaNo ratings yet

- Working Capital ManagementDocument45 pagesWorking Capital Managementvini2710No ratings yet

- TM5 Small Business ManagementDocument39 pagesTM5 Small Business ManagementHilyah Hana KeyNo ratings yet

- Dirección Financiera - Semana 2Document8 pagesDirección Financiera - Semana 2yessNo ratings yet

- Part 3 - Understanding Financial Statements and ReportsDocument7 pagesPart 3 - Understanding Financial Statements and ReportsJeanrey AlcantaraNo ratings yet

- Financial Statement Analysis: Charles H. GibsonDocument38 pagesFinancial Statement Analysis: Charles H. GibsonmohamedNo ratings yet

- EFM4, CH 17, Slides, 07-02-18Document34 pagesEFM4, CH 17, Slides, 07-02-18Nicholas Malvin SaputraNo ratings yet

- Week 12 13Document36 pagesWeek 12 13shani2010No ratings yet

- Chap 1Document32 pagesChap 1Trần Lê NaNo ratings yet

- 01-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesDocument60 pages01-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesThanh ThùyNo ratings yet

- 82 Working Capital ManagementDocument25 pages82 Working Capital ManagementPrashant SharmaNo ratings yet

- Sesi 12-Working Capital ManagementDocument33 pagesSesi 12-Working Capital Managementdias khairunnisaNo ratings yet

- Principles of Working CapitalDocument24 pagesPrinciples of Working CapitalAnuj VyasNo ratings yet

- Introduction and Working Capital ManagementDocument4 pagesIntroduction and Working Capital Managementmh bachooNo ratings yet

- FMP Lecture - Working CapitalDocument31 pagesFMP Lecture - Working CapitalFatima ZehraNo ratings yet

- Financial Statement Analysis: Charles H. GibsonDocument26 pagesFinancial Statement Analysis: Charles H. GibsonGud BooyNo ratings yet

- Working Capital ManagementDocument22 pagesWorking Capital Managementkelvin pogiNo ratings yet

- Working Capital ManagementDocument20 pagesWorking Capital ManagementHaardik GandhiNo ratings yet

- CH 2Document42 pagesCH 2koukifou4No ratings yet

- Working Capital ManagementDocument34 pagesWorking Capital ManagementAnna WilliamsNo ratings yet

- Chapter-3 - Working Capital MGTDocument57 pagesChapter-3 - Working Capital MGTRaunak YadavNo ratings yet

- AGibson 13E Ch10Document24 pagesAGibson 13E Ch10finance tutorNo ratings yet

- Financial ProjectDocument8 pagesFinancial ProjectShekibaNo ratings yet

- Module 1-1Document6 pagesModule 1-1shejal naikNo ratings yet

- AGibson 13E Ch10Document25 pagesAGibson 13E Ch10Ihab Al-AnabousiNo ratings yet

- Exploring The World of Business and EconomicsDocument53 pagesExploring The World of Business and EconomicsLalaNo ratings yet

- Ifrs15 Are You Good To Go ConstructionDocument19 pagesIfrs15 Are You Good To Go ConstructionbatuchemNo ratings yet

- Financial Accounting Module 6 SummaryDocument6 pagesFinancial Accounting Module 6 SummaryKashika LathNo ratings yet

- Liquidity of Short-Term Assets - Related Debt-Paying AbilityDocument48 pagesLiquidity of Short-Term Assets - Related Debt-Paying AbilityJuan LeonardoNo ratings yet

- Working Capital ManagementDocument20 pagesWorking Capital Managementsmwanginet7No ratings yet

- FSA - Ch06 - Liquidity of Short-Term Assets Related Debt-Paying AbilityDocument46 pagesFSA - Ch06 - Liquidity of Short-Term Assets Related Debt-Paying AbilityAmine AbdesmadNo ratings yet

- FM Week 13Document35 pagesFM Week 13shaikhsafwan7788No ratings yet

- Business FinanceDocument10 pagesBusiness FinanceLisaNo ratings yet

- Mergers & Acquisitions Basics: IFLP Boot Camp May 16, 2018Document59 pagesMergers & Acquisitions Basics: IFLP Boot Camp May 16, 2018Soumya KesharwaniNo ratings yet

- Financial Analysis Using RatiosDocument12 pagesFinancial Analysis Using Ratiossamar RamadanNo ratings yet

- Financial Statement Analysis: by Uditha JayasingheDocument19 pagesFinancial Statement Analysis: by Uditha JayasinghesanjuladasanNo ratings yet

- Working Capital ManagementDocument34 pagesWorking Capital ManagementNirmal ShresthaNo ratings yet

- Module 3 P1&2 Evol. of Intl. Business Gfd23Document30 pagesModule 3 P1&2 Evol. of Intl. Business Gfd23Kristian UyNo ratings yet

- Businessfinance12 q3 Mod4 FINAL PDFDocument13 pagesBusinessfinance12 q3 Mod4 FINAL PDFJoyce Anne ManzanilloNo ratings yet

- Financial Statement Analysis Using RatiosDocument11 pagesFinancial Statement Analysis Using RatiosRobin LlagunoNo ratings yet

- Working CapitalDocument111 pagesWorking Capitalshehjadi918No ratings yet

- Working Capital Management: Dr. Gurendra Nath BhardwajDocument48 pagesWorking Capital Management: Dr. Gurendra Nath BhardwajPrashant TyagiNo ratings yet

- Super7 Operations: The Next Step for Lean in Financial ServicesFrom EverandSuper7 Operations: The Next Step for Lean in Financial ServicesNo ratings yet

- Digital Banking - ISEI - 210722Document38 pagesDigital Banking - ISEI - 210722nora lizaNo ratings yet

- Global Money Dispatch: WarnedDocument4 pagesGlobal Money Dispatch: WarnedViolin_Man100% (1)

- 2017-07-01 10.02PM Email Trent To Schneider Re. PMT.Document3 pages2017-07-01 10.02PM Email Trent To Schneider Re. PMT.larry-612445No ratings yet

- Working Capital Management-Accounts Payable and Receivable: Margarita KouloumbriDocument30 pagesWorking Capital Management-Accounts Payable and Receivable: Margarita KouloumbriInga ȚîgaiNo ratings yet

- IFC History Book Second EditionDocument144 pagesIFC History Book Second EditionMinh Binh PhamNo ratings yet

- F 39343900 ngs0404 30-11-2022 30112022 134801Document1 pageF 39343900 ngs0404 30-11-2022 30112022 134801Reta BulardaNo ratings yet

- Fundamental Accounting Principles 24th Edition Wild Solutions ManualDocument10 pagesFundamental Accounting Principles 24th Edition Wild Solutions Manualeffigiesbuffoonmwve9100% (29)

- 16 MB Liquidity Ratio'sDocument22 pages16 MB Liquidity Ratio'sKrrishna Rajesh TOKARAWATNo ratings yet

- Personal Finance SyllabusDocument3 pagesPersonal Finance SyllabusLigia LandowNo ratings yet

- Chapter 2 AccountingDocument12 pagesChapter 2 Accountingmoon loverNo ratings yet

- Delegation of Loaning Powers in UbiDocument2 pagesDelegation of Loaning Powers in UbiShradha KhandareNo ratings yet

- Origin of TransactionDocument7 pagesOrigin of TransactionrudraNo ratings yet

- Business Banking Price ListDocument15 pagesBusiness Banking Price ListSARFRAZ ALINo ratings yet

- T24 System Build - Core V1.0Document30 pagesT24 System Build - Core V1.0Quoc Dat TranNo ratings yet

- BankingLaws BEQDocument7 pagesBankingLaws BEQAnastasia ZaitsevNo ratings yet

- Secrecy of Bank Deposits ActDocument7 pagesSecrecy of Bank Deposits ActJohn Churchill Gil SaducosNo ratings yet

- BSA 3-4 - Quiz 1 - Group 3Document7 pagesBSA 3-4 - Quiz 1 - Group 3Jornel MandiaNo ratings yet

- Faqs On Internet Banking Services (Ibs) For NrisDocument2 pagesFaqs On Internet Banking Services (Ibs) For NrisABMNo ratings yet

- DATA ANALYSIS AND INTERPRETATION of Rain Bow PipesDocument10 pagesDATA ANALYSIS AND INTERPRETATION of Rain Bow Pipesarmeena falakNo ratings yet

- Credit Card StatementDocument3 pagesCredit Card StatementSayan GhoshNo ratings yet

- Handbook On CTS Clearing For BranchesDocument30 pagesHandbook On CTS Clearing For BranchesparthaNo ratings yet

- Danta Health Bank Statement 06.30.10Document7 pagesDanta Health Bank Statement 06.30.10Md. Mahabubur rahamanNo ratings yet

- Statement 2022 8Document4 pagesStatement 2022 8wconceptouNo ratings yet

- Shriram Transport Finance Company Ltd. - Initiating Coverage - 30032021Document12 pagesShriram Transport Finance Company Ltd. - Initiating Coverage - 30032021Devarsh VakilNo ratings yet

- Standard Chartered PLC Is A British Multinational BankingDocument8 pagesStandard Chartered PLC Is A British Multinational Bankingaditya saiNo ratings yet

- Strawman DeceptionDocument11 pagesStrawman DeceptionGrey WolfNo ratings yet

- What Is A Bank Identification Number (BIN), and HDocument1 pageWhat Is A Bank Identification Number (BIN), and HYogeshwaran.sNo ratings yet