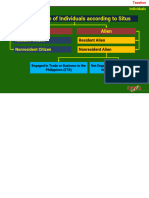

Classification of Tax Payers

Classification of Tax Payers

You might also like

- Reviewer Chapter 2Document6 pagesReviewer Chapter 2Ken NavarroNo ratings yet

- Income Taxation Lecture Notes.5.Classifications of Individual TaxpayersDocument5 pagesIncome Taxation Lecture Notes.5.Classifications of Individual Taxpayerseinel dc100% (1)

- Lesson 2 Taxation of IndividualsDocument40 pagesLesson 2 Taxation of IndividualsQuenie De la CruzNo ratings yet

- Income Recognition, Measurement and Reporting and Taxpayer ClassificationsDocument27 pagesIncome Recognition, Measurement and Reporting and Taxpayer ClassificationsAries Queencel Bernante BocarNo ratings yet

- Basergo, Lovers Mae B. General Classification of Individual TaxpayersDocument2 pagesBasergo, Lovers Mae B. General Classification of Individual Taxpayerslavender kayeNo ratings yet

- Introduction To Income Taxation - 625041052Document21 pagesIntroduction To Income Taxation - 625041052ANGELA JOY FLORESNo ratings yet

- InTax Unit 2Document3 pagesInTax Unit 2ElleNo ratings yet

- Handout TaxationDocument2 pagesHandout TaxationJohn Oicemen RocaNo ratings yet

- Types of Income Tax PayersDocument3 pagesTypes of Income Tax PayersAce Fati-igNo ratings yet

- (TAX) Income Taxation Updated Jan 9 2022Document133 pages(TAX) Income Taxation Updated Jan 9 2022Reginald ValenciaNo ratings yet

- Train Individual INCOME TAXDocument48 pagesTrain Individual INCOME TAXMeireen Ann100% (2)

- Individual Taxpayers (Ordinary Income and Fringe Benefits)Document86 pagesIndividual Taxpayers (Ordinary Income and Fringe Benefits)ipbsalanguitNo ratings yet

- Introduction To Individual Income Taxation Chapter Overview and ObjectivesDocument25 pagesIntroduction To Individual Income Taxation Chapter Overview and ObjectivesMatta, Jherrie MaeNo ratings yet

- Classification of Individual Taxpayers - AlienDocument32 pagesClassification of Individual Taxpayers - AlienMarria FrancezcaNo ratings yet

- Template Taxation Unit IIDocument29 pagesTemplate Taxation Unit IINacion, Jaime G.No ratings yet

- What Are The Kinds of TaxpayersDocument4 pagesWhat Are The Kinds of TaxpayersALee Bud100% (1)

- Prelim Income TaxationDocument55 pagesPrelim Income TaxationclytemnestraNo ratings yet

- Taxation of IndividualsDocument49 pagesTaxation of IndividualsAnastasha Grey100% (1)

- Taxation Ass 2Document1 pageTaxation Ass 2Jazon GotanghoNo ratings yet

- Gross Income (Classification of Taxpayers)Document12 pagesGross Income (Classification of Taxpayers)Michael Thom MacabuhayNo ratings yet

- MODULE 5 Individual TaxationDocument3 pagesMODULE 5 Individual TaxationCEDRICK MARX ABRIGARNo ratings yet

- 2 Classification of Individual TaxpayersDocument2 pages2 Classification of Individual TaxpayersDiana SheineNo ratings yet

- TAX-5.0 - Individual Income TaxDocument65 pagesTAX-5.0 - Individual Income TaxCharmaine RosalesNo ratings yet

- TAX Reviewer FINALSDocument9 pagesTAX Reviewer FINALSLalaine SantiagoNo ratings yet

- Inroduction To Income TaxationDocument20 pagesInroduction To Income TaxationW-304-Bautista,PreciousNo ratings yet

- Intax ExerciseDocument26 pagesIntax ExerciseJosh CruzNo ratings yet

- TAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S ADocument12 pagesTAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S AVaughn TheoNo ratings yet

- Types of TaxpayerDocument23 pagesTypes of TaxpayerReina Rose LebrillaNo ratings yet

- Features of Philippine Income Tax SystemDocument9 pagesFeatures of Philippine Income Tax SystemPATRICIA ANGELICA VINUYANo ratings yet

- Mary Joy P. Junio, Cpa Notre Dame of Midsayap College Midsayap, CotabatoDocument8 pagesMary Joy P. Junio, Cpa Notre Dame of Midsayap College Midsayap, CotabatoJonathan JunioNo ratings yet

- 03 Individuals. Study Notes. LectureDocument54 pages03 Individuals. Study Notes. Lecturemarvin.cpa.cmaNo ratings yet

- Quickie PreFi Tax PDFDocument12 pagesQuickie PreFi Tax PDFJoesil Dianne Sempron100% (1)

- PreFi Tax PDFDocument21 pagesPreFi Tax PDFJoesil Dianne SempronNo ratings yet

- Income Tax For IndividualsDocument90 pagesIncome Tax For IndividualsRubyjane Kim100% (1)

- Kinds of Taxpayers and Situs of IncomeDocument2 pagesKinds of Taxpayers and Situs of IncomeMelanie SamsonaNo ratings yet

- HO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Document5 pagesHO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Erine ContranoNo ratings yet

- BAC103A-02a Income Tax For IndividualsDocument8 pagesBAC103A-02a Income Tax For IndividualsNovelyn Duyogan100% (1)

- 3 - Income Tax On IndividualsDocument22 pages3 - Income Tax On IndividualsRylleMatthanCorderoNo ratings yet

- Income Taxation IndividualsDocument19 pagesIncome Taxation IndividualsJenniNo ratings yet

- Tax601 Individual Itx Lecture Notes 122Document12 pagesTax601 Individual Itx Lecture Notes 122Justine JaymaNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErvin Ray FernandezNo ratings yet

- M2u Classification Individual Taxation P1Document30 pagesM2u Classification Individual Taxation P1Xehdrickke FernandezNo ratings yet

- Classification of Individual TaxpayerDocument31 pagesClassification of Individual TaxpayerPatrick BituinNo ratings yet

- Income Taxation Week 3Document20 pagesIncome Taxation Week 3Hannah Rae ChingNo ratings yet

- Income Tax On Individuals PDFDocument20 pagesIncome Tax On Individuals PDFKaren Joy MagsayoNo ratings yet

- Taxation Week 3Document8 pagesTaxation Week 3Jurian Jaan PeligroNo ratings yet

- Individual TaxpayerDocument10 pagesIndividual TaxpayerLL. yangzNo ratings yet

- Tax 601Document11 pagesTax 601C.J. Clarisse FranciscoNo ratings yet

- Taxation of IndividualsDocument22 pagesTaxation of IndividualsTurksNo ratings yet

- Taxation of IndividualsDocument9 pagesTaxation of IndividualsBrielle GabNo ratings yet

- Module 2 - Income Taxes For Individuals - Lecture NotesDocument52 pagesModule 2 - Income Taxes For Individuals - Lecture NotesRina Bico Advincula100% (1)

- 2nd Semester Income Taxation Module 5 Classification of TaxpayersDocument5 pages2nd Semester Income Taxation Module 5 Classification of TaxpayersMaryrose SumulongNo ratings yet

- Income Tax ConDocument2 pagesIncome Tax ConMaricon EstradaNo ratings yet

- Lesson 5 Inclusions Exclusions From Gi Final TaxDocument17 pagesLesson 5 Inclusions Exclusions From Gi Final TaxOrduna Mae AnnNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErwin TorresNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- Share Taxpayer and Elements of Gross IncomeDocument24 pagesShare Taxpayer and Elements of Gross IncomeJessa Mae IgotNo ratings yet

- ACC311 3rd Exam CoverageDocument108 pagesACC311 3rd Exam CoverageHilarie JeanNo ratings yet

- Deductions From Gross Income - 020807Document9 pagesDeductions From Gross Income - 020807Hilarie JeanNo ratings yet

- Computation of Corporate Tax PayersDocument14 pagesComputation of Corporate Tax PayersHilarie JeanNo ratings yet

- Practice ACC 311 Competency ExamDocument2 pagesPractice ACC 311 Competency ExamHilarie JeanNo ratings yet

- ACCExpanded Opportunity Part 1Document4 pagesACCExpanded Opportunity Part 1Hilarie JeanNo ratings yet

- SM07 4thExamReview 054702Document4 pagesSM07 4thExamReview 054702Hilarie JeanNo ratings yet

- Corpuz vs. Sto. TomasDocument3 pagesCorpuz vs. Sto. TomasSarah Monique Nicole Antoinette GolezNo ratings yet

- Transcript Req ProseDocument2 pagesTranscript Req ProseMasterReader99No ratings yet

- Gorospe Vs People - HomicideDocument4 pagesGorospe Vs People - HomicidegeorjalynjoyNo ratings yet

- Works of Defence Act 1903 1Document21 pagesWorks of Defence Act 1903 1Eighteenth JulyNo ratings yet

- Answers EvidenceDocument5 pagesAnswers EvidenceAmiza Abd KaharNo ratings yet

- 7.1lao v. Yao Bio Lim20210423-12-1v6ji2vDocument16 pages7.1lao v. Yao Bio Lim20210423-12-1v6ji2vSeok Gyeong KangNo ratings yet

- Philippine Airlines V NLRCDocument2 pagesPhilippine Airlines V NLRCCedricNo ratings yet

- HOW DOD, VA, and Military Industrial Complex (Deep State) : Lock Acceptable Claims in The Army & DOD's Safe ServerDocument172 pagesHOW DOD, VA, and Military Industrial Complex (Deep State) : Lock Acceptable Claims in The Army & DOD's Safe ServeradaadvocatesuebozgozNo ratings yet

- Declaration Form FINALDocument1 pageDeclaration Form FINALAnonymous TlYmhkNo ratings yet

- Opening Brief 22CA77 Emily Cohen AppealDocument54 pagesOpening Brief 22CA77 Emily Cohen AppealEmily CohenNo ratings yet

- 1740 CRPC Project SubmissionDocument12 pages1740 CRPC Project SubmissionMEHULANo ratings yet

- People v. Serrano G.R. No. L 7973Document2 pagesPeople v. Serrano G.R. No. L 7973Tootsie GuzmaNo ratings yet

- Substantive and Procedural LawDocument8 pagesSubstantive and Procedural LawNaif OmarNo ratings yet

- OCA Circular No. 01-2024Document7 pagesOCA Circular No. 01-2024RTC FortetoNo ratings yet

- Case LawDocument10 pagesCase LawKirti DNo ratings yet

- Defendant's Motion To Disqualify Judge Edward L. ScottDocument42 pagesDefendant's Motion To Disqualify Judge Edward L. ScottNeil GillespieNo ratings yet

- Chronological Case Summary Trenton-Ivy WIDocument1 pageChronological Case Summary Trenton-Ivy WIGrizzly DocsNo ratings yet

- 823 F.2d 548 Unpublished Disposition: United States Court of Appeals, Fourth CircuitDocument6 pages823 F.2d 548 Unpublished Disposition: United States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- Rule 58 Preliminary InjunctionDocument77 pagesRule 58 Preliminary InjunctionJan Igor GalinatoNo ratings yet

- Fencing and Anti-Carnapping Case DigestsDocument16 pagesFencing and Anti-Carnapping Case DigestsCarla January OngNo ratings yet

- (Day 29) (Final) The Hindu Minority and Guardianship Act, 1956Document4 pages(Day 29) (Final) The Hindu Minority and Guardianship Act, 1956Deb DasNo ratings yet

- Rivera V ChuaDocument2 pagesRivera V ChuaLarraine FallongNo ratings yet

- 196-737-1-PB-Malaysia Case Study PDFDocument16 pages196-737-1-PB-Malaysia Case Study PDFGM KendraNo ratings yet

- Andamo Vs IACDocument6 pagesAndamo Vs IACArmen MagbitangNo ratings yet

- Okeke v. INS, 4th Cir. (1996)Document6 pagesOkeke v. INS, 4th Cir. (1996)Scribd Government DocsNo ratings yet

- Kilosbayan Vs MoratoDocument3 pagesKilosbayan Vs MoratoRmLyn MclnaoNo ratings yet

- Alternative Dispute ResolutionDocument27 pagesAlternative Dispute ResolutionAnil Patel100% (1)

- A.M. No. 99-10-05-0 Procedure in Extra-Judicial Foreclosure of MortgageDocument2 pagesA.M. No. 99-10-05-0 Procedure in Extra-Judicial Foreclosure of Mortgagechill21ggNo ratings yet

- Chua Vs CA PolidoDocument2 pagesChua Vs CA PolidoJohnde MartinezNo ratings yet

- Witness Cannot Be Added As An Accused Even If His Statements Are Inculpatory: Supreme CourtDocument36 pagesWitness Cannot Be Added As An Accused Even If His Statements Are Inculpatory: Supreme CourtLive Law100% (1)

Download as pptx, pdf, or txt

You might also like

- Reviewer Chapter 2Document6 pagesReviewer Chapter 2Ken NavarroNo ratings yet

- Income Taxation Lecture Notes.5.Classifications of Individual TaxpayersDocument5 pagesIncome Taxation Lecture Notes.5.Classifications of Individual Taxpayerseinel dc100% (1)

- Lesson 2 Taxation of IndividualsDocument40 pagesLesson 2 Taxation of IndividualsQuenie De la CruzNo ratings yet

- Income Recognition, Measurement and Reporting and Taxpayer ClassificationsDocument27 pagesIncome Recognition, Measurement and Reporting and Taxpayer ClassificationsAries Queencel Bernante BocarNo ratings yet

- Basergo, Lovers Mae B. General Classification of Individual TaxpayersDocument2 pagesBasergo, Lovers Mae B. General Classification of Individual Taxpayerslavender kayeNo ratings yet

- Introduction To Income Taxation - 625041052Document21 pagesIntroduction To Income Taxation - 625041052ANGELA JOY FLORESNo ratings yet

- InTax Unit 2Document3 pagesInTax Unit 2ElleNo ratings yet

- Handout TaxationDocument2 pagesHandout TaxationJohn Oicemen RocaNo ratings yet

- Types of Income Tax PayersDocument3 pagesTypes of Income Tax PayersAce Fati-igNo ratings yet

- (TAX) Income Taxation Updated Jan 9 2022Document133 pages(TAX) Income Taxation Updated Jan 9 2022Reginald ValenciaNo ratings yet

- Train Individual INCOME TAXDocument48 pagesTrain Individual INCOME TAXMeireen Ann100% (2)

- Individual Taxpayers (Ordinary Income and Fringe Benefits)Document86 pagesIndividual Taxpayers (Ordinary Income and Fringe Benefits)ipbsalanguitNo ratings yet

- Introduction To Individual Income Taxation Chapter Overview and ObjectivesDocument25 pagesIntroduction To Individual Income Taxation Chapter Overview and ObjectivesMatta, Jherrie MaeNo ratings yet

- Classification of Individual Taxpayers - AlienDocument32 pagesClassification of Individual Taxpayers - AlienMarria FrancezcaNo ratings yet

- Template Taxation Unit IIDocument29 pagesTemplate Taxation Unit IINacion, Jaime G.No ratings yet

- What Are The Kinds of TaxpayersDocument4 pagesWhat Are The Kinds of TaxpayersALee Bud100% (1)

- Prelim Income TaxationDocument55 pagesPrelim Income TaxationclytemnestraNo ratings yet

- Taxation of IndividualsDocument49 pagesTaxation of IndividualsAnastasha Grey100% (1)

- Taxation Ass 2Document1 pageTaxation Ass 2Jazon GotanghoNo ratings yet

- Gross Income (Classification of Taxpayers)Document12 pagesGross Income (Classification of Taxpayers)Michael Thom MacabuhayNo ratings yet

- MODULE 5 Individual TaxationDocument3 pagesMODULE 5 Individual TaxationCEDRICK MARX ABRIGARNo ratings yet

- 2 Classification of Individual TaxpayersDocument2 pages2 Classification of Individual TaxpayersDiana SheineNo ratings yet

- TAX-5.0 - Individual Income TaxDocument65 pagesTAX-5.0 - Individual Income TaxCharmaine RosalesNo ratings yet

- TAX Reviewer FINALSDocument9 pagesTAX Reviewer FINALSLalaine SantiagoNo ratings yet

- Inroduction To Income TaxationDocument20 pagesInroduction To Income TaxationW-304-Bautista,PreciousNo ratings yet

- Intax ExerciseDocument26 pagesIntax ExerciseJosh CruzNo ratings yet

- TAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S ADocument12 pagesTAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S AVaughn TheoNo ratings yet

- Types of TaxpayerDocument23 pagesTypes of TaxpayerReina Rose LebrillaNo ratings yet

- Features of Philippine Income Tax SystemDocument9 pagesFeatures of Philippine Income Tax SystemPATRICIA ANGELICA VINUYANo ratings yet

- Mary Joy P. Junio, Cpa Notre Dame of Midsayap College Midsayap, CotabatoDocument8 pagesMary Joy P. Junio, Cpa Notre Dame of Midsayap College Midsayap, CotabatoJonathan JunioNo ratings yet

- 03 Individuals. Study Notes. LectureDocument54 pages03 Individuals. Study Notes. Lecturemarvin.cpa.cmaNo ratings yet

- Quickie PreFi Tax PDFDocument12 pagesQuickie PreFi Tax PDFJoesil Dianne Sempron100% (1)

- PreFi Tax PDFDocument21 pagesPreFi Tax PDFJoesil Dianne SempronNo ratings yet

- Income Tax For IndividualsDocument90 pagesIncome Tax For IndividualsRubyjane Kim100% (1)

- Kinds of Taxpayers and Situs of IncomeDocument2 pagesKinds of Taxpayers and Situs of IncomeMelanie SamsonaNo ratings yet

- HO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Document5 pagesHO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Erine ContranoNo ratings yet

- BAC103A-02a Income Tax For IndividualsDocument8 pagesBAC103A-02a Income Tax For IndividualsNovelyn Duyogan100% (1)

- 3 - Income Tax On IndividualsDocument22 pages3 - Income Tax On IndividualsRylleMatthanCorderoNo ratings yet

- Income Taxation IndividualsDocument19 pagesIncome Taxation IndividualsJenniNo ratings yet

- Tax601 Individual Itx Lecture Notes 122Document12 pagesTax601 Individual Itx Lecture Notes 122Justine JaymaNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErvin Ray FernandezNo ratings yet

- M2u Classification Individual Taxation P1Document30 pagesM2u Classification Individual Taxation P1Xehdrickke FernandezNo ratings yet

- Classification of Individual TaxpayerDocument31 pagesClassification of Individual TaxpayerPatrick BituinNo ratings yet

- Income Taxation Week 3Document20 pagesIncome Taxation Week 3Hannah Rae ChingNo ratings yet

- Income Tax On Individuals PDFDocument20 pagesIncome Tax On Individuals PDFKaren Joy MagsayoNo ratings yet

- Taxation Week 3Document8 pagesTaxation Week 3Jurian Jaan PeligroNo ratings yet

- Individual TaxpayerDocument10 pagesIndividual TaxpayerLL. yangzNo ratings yet

- Tax 601Document11 pagesTax 601C.J. Clarisse FranciscoNo ratings yet

- Taxation of IndividualsDocument22 pagesTaxation of IndividualsTurksNo ratings yet

- Taxation of IndividualsDocument9 pagesTaxation of IndividualsBrielle GabNo ratings yet

- Module 2 - Income Taxes For Individuals - Lecture NotesDocument52 pagesModule 2 - Income Taxes For Individuals - Lecture NotesRina Bico Advincula100% (1)

- 2nd Semester Income Taxation Module 5 Classification of TaxpayersDocument5 pages2nd Semester Income Taxation Module 5 Classification of TaxpayersMaryrose SumulongNo ratings yet

- Income Tax ConDocument2 pagesIncome Tax ConMaricon EstradaNo ratings yet

- Lesson 5 Inclusions Exclusions From Gi Final TaxDocument17 pagesLesson 5 Inclusions Exclusions From Gi Final TaxOrduna Mae AnnNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErwin TorresNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- Share Taxpayer and Elements of Gross IncomeDocument24 pagesShare Taxpayer and Elements of Gross IncomeJessa Mae IgotNo ratings yet

- ACC311 3rd Exam CoverageDocument108 pagesACC311 3rd Exam CoverageHilarie JeanNo ratings yet

- Deductions From Gross Income - 020807Document9 pagesDeductions From Gross Income - 020807Hilarie JeanNo ratings yet

- Computation of Corporate Tax PayersDocument14 pagesComputation of Corporate Tax PayersHilarie JeanNo ratings yet

- Practice ACC 311 Competency ExamDocument2 pagesPractice ACC 311 Competency ExamHilarie JeanNo ratings yet

- ACCExpanded Opportunity Part 1Document4 pagesACCExpanded Opportunity Part 1Hilarie JeanNo ratings yet

- SM07 4thExamReview 054702Document4 pagesSM07 4thExamReview 054702Hilarie JeanNo ratings yet

- Corpuz vs. Sto. TomasDocument3 pagesCorpuz vs. Sto. TomasSarah Monique Nicole Antoinette GolezNo ratings yet

- Transcript Req ProseDocument2 pagesTranscript Req ProseMasterReader99No ratings yet

- Gorospe Vs People - HomicideDocument4 pagesGorospe Vs People - HomicidegeorjalynjoyNo ratings yet

- Works of Defence Act 1903 1Document21 pagesWorks of Defence Act 1903 1Eighteenth JulyNo ratings yet

- Answers EvidenceDocument5 pagesAnswers EvidenceAmiza Abd KaharNo ratings yet

- 7.1lao v. Yao Bio Lim20210423-12-1v6ji2vDocument16 pages7.1lao v. Yao Bio Lim20210423-12-1v6ji2vSeok Gyeong KangNo ratings yet

- Philippine Airlines V NLRCDocument2 pagesPhilippine Airlines V NLRCCedricNo ratings yet

- HOW DOD, VA, and Military Industrial Complex (Deep State) : Lock Acceptable Claims in The Army & DOD's Safe ServerDocument172 pagesHOW DOD, VA, and Military Industrial Complex (Deep State) : Lock Acceptable Claims in The Army & DOD's Safe ServeradaadvocatesuebozgozNo ratings yet

- Declaration Form FINALDocument1 pageDeclaration Form FINALAnonymous TlYmhkNo ratings yet

- Opening Brief 22CA77 Emily Cohen AppealDocument54 pagesOpening Brief 22CA77 Emily Cohen AppealEmily CohenNo ratings yet

- 1740 CRPC Project SubmissionDocument12 pages1740 CRPC Project SubmissionMEHULANo ratings yet

- People v. Serrano G.R. No. L 7973Document2 pagesPeople v. Serrano G.R. No. L 7973Tootsie GuzmaNo ratings yet

- Substantive and Procedural LawDocument8 pagesSubstantive and Procedural LawNaif OmarNo ratings yet

- OCA Circular No. 01-2024Document7 pagesOCA Circular No. 01-2024RTC FortetoNo ratings yet

- Case LawDocument10 pagesCase LawKirti DNo ratings yet

- Defendant's Motion To Disqualify Judge Edward L. ScottDocument42 pagesDefendant's Motion To Disqualify Judge Edward L. ScottNeil GillespieNo ratings yet

- Chronological Case Summary Trenton-Ivy WIDocument1 pageChronological Case Summary Trenton-Ivy WIGrizzly DocsNo ratings yet

- 823 F.2d 548 Unpublished Disposition: United States Court of Appeals, Fourth CircuitDocument6 pages823 F.2d 548 Unpublished Disposition: United States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- Rule 58 Preliminary InjunctionDocument77 pagesRule 58 Preliminary InjunctionJan Igor GalinatoNo ratings yet

- Fencing and Anti-Carnapping Case DigestsDocument16 pagesFencing and Anti-Carnapping Case DigestsCarla January OngNo ratings yet

- (Day 29) (Final) The Hindu Minority and Guardianship Act, 1956Document4 pages(Day 29) (Final) The Hindu Minority and Guardianship Act, 1956Deb DasNo ratings yet

- Rivera V ChuaDocument2 pagesRivera V ChuaLarraine FallongNo ratings yet

- 196-737-1-PB-Malaysia Case Study PDFDocument16 pages196-737-1-PB-Malaysia Case Study PDFGM KendraNo ratings yet

- Andamo Vs IACDocument6 pagesAndamo Vs IACArmen MagbitangNo ratings yet

- Okeke v. INS, 4th Cir. (1996)Document6 pagesOkeke v. INS, 4th Cir. (1996)Scribd Government DocsNo ratings yet

- Kilosbayan Vs MoratoDocument3 pagesKilosbayan Vs MoratoRmLyn MclnaoNo ratings yet

- Alternative Dispute ResolutionDocument27 pagesAlternative Dispute ResolutionAnil Patel100% (1)

- A.M. No. 99-10-05-0 Procedure in Extra-Judicial Foreclosure of MortgageDocument2 pagesA.M. No. 99-10-05-0 Procedure in Extra-Judicial Foreclosure of Mortgagechill21ggNo ratings yet

- Chua Vs CA PolidoDocument2 pagesChua Vs CA PolidoJohnde MartinezNo ratings yet

- Witness Cannot Be Added As An Accused Even If His Statements Are Inculpatory: Supreme CourtDocument36 pagesWitness Cannot Be Added As An Accused Even If His Statements Are Inculpatory: Supreme CourtLive Law100% (1)