Download as pptx, pdf, or txt

You might also like

- Digital Marketing Project @HDFCDocument145 pagesDigital Marketing Project @HDFCQuikk Loan67% (3)

- Venture Capital 101 PDFDocument38 pagesVenture Capital 101 PDFPhuong Chi Nguyen100% (3)

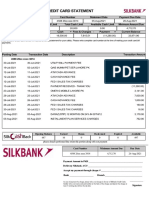

- Credit Card StatementDocument3 pagesCredit Card StatementSaifullah Saifi0% (1)

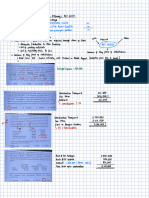

- Good InformationDocument3 pagesGood InformationHoshen MollaNo ratings yet

- Edelweiss Capital: July 2010Document41 pagesEdelweiss Capital: July 2010Piyush SharmaNo ratings yet

- Consolidation Entries Debi T Cred ItDocument4 pagesConsolidation Entries Debi T Cred ItsafqwfNo ratings yet

- Conny & Co II V6 - ShortDocument32 pagesConny & Co II V6 - ShortRandalNo ratings yet

- IAVC - Venture Capital Training PDFDocument77 pagesIAVC - Venture Capital Training PDFvikasNo ratings yet

- Investment Calculator - SmartAssetDocument1 pageInvestment Calculator - SmartAssetSulemanNo ratings yet

- JP Morgan The Maltese Falcoin 1644068844Document31 pagesJP Morgan The Maltese Falcoin 1644068844Christian Gazzetta Mancini100% (1)

- Group 10 - Capital FloatDocument19 pagesGroup 10 - Capital FloatAnonymous V2hyzY1axNo ratings yet

- Bryce Start Up Space 2021Document26 pagesBryce Start Up Space 2021rebate182No ratings yet

- KTrade - Startup Funding Report 2021Document51 pagesKTrade - Startup Funding Report 2021UsaidMandvia100% (1)

- Vietnam Startup Investment Insight:: 2017 in SnapshotDocument8 pagesVietnam Startup Investment Insight:: 2017 in Snapshothungnguyen2332No ratings yet

- Mike Beveridge - Doing Business Under The OceanDocument18 pagesMike Beveridge - Doing Business Under The OceanGiacomo CalligarisNo ratings yet

- Project Owner ModuleDocument41 pagesProject Owner ModuleGaurav KhannaNo ratings yet

- Financial Performance Kpi Powerpoint PPT Template BundlesDocument12 pagesFinancial Performance Kpi Powerpoint PPT Template Bundlesovie100% (2)

- African Startup Funding Landscape 2020 - Startuplist AfricaDocument21 pagesAfrican Startup Funding Landscape 2020 - Startuplist Africaace1870% (1)

- Crowd Real Estate Site TrackingDocument56 pagesCrowd Real Estate Site TrackingahgonzalezpNo ratings yet

- Building A Solid Financial FoundationDocument2 pagesBuilding A Solid Financial Foundationapi-25884993No ratings yet

- What Power Dividens HaveDocument12 pagesWhat Power Dividens HaveAlin UngureanuNo ratings yet

- 2024 MGB Group 06 v1Document5 pages2024 MGB Group 06 v1sakshisingh0712No ratings yet

- Ginny's Restaurant Case StudyDocument5 pagesGinny's Restaurant Case StudyМенчеВучковаNo ratings yet

- Ross 7 Ech 04 AppendixDocument11 pagesRoss 7 Ech 04 AppendixEndah DipoyantiNo ratings yet

- Empact Global, Homestrings Diaspora Bond ProgramDocument23 pagesEmpact Global, Homestrings Diaspora Bond ProgramADBI EventsNo ratings yet

- Balance Sheet of FinanceDocument17 pagesBalance Sheet of FinanceManish TayadeNo ratings yet

- Financial Accounting Chapter 1 - 3: By: Stefanie (125180444) Angela (125180447) Yuvina (125180464)Document20 pagesFinancial Accounting Chapter 1 - 3: By: Stefanie (125180444) Angela (125180447) Yuvina (125180464)Elafan storeNo ratings yet

- Ozone III Investor Deck OpportunitydB Pitch Day 11.3.21Document50 pagesOzone III Investor Deck OpportunitydB Pitch Day 11.3.21Capital AdvisorNo ratings yet

- ICC Trade Now AsiaDocument4 pagesICC Trade Now AsiaducvaNo ratings yet

- ONDK BAML TMT Conf FINAL 060315Document33 pagesONDK BAML TMT Conf FINAL 060315Yves-donald MakoumbouNo ratings yet

- Jawaban UTS MK Capital BudgetingDocument2 pagesJawaban UTS MK Capital BudgetingAnugerah AgungNo ratings yet

- Equidam Valuation Report SampleDocument25 pagesEquidam Valuation Report SampleRelin Ganda SaputraNo ratings yet

- Net Present Value: First Principles of Finance: Mcgraw-Hill/Irwin Corporate Finance, 7/EDocument11 pagesNet Present Value: First Principles of Finance: Mcgraw-Hill/Irwin Corporate Finance, 7/EAntora HoqueNo ratings yet

- Investments and Fair Value SolutionsDocument32 pagesInvestments and Fair Value Solutionssarah zahid100% (1)

- Rate Buydown FlyerDocument1 pageRate Buydown FlyerKen CaianiNo ratings yet

- The Deal Full Year 2016: UK Equity InvestmentDocument44 pagesThe Deal Full Year 2016: UK Equity InvestmentCrowdfundInsider100% (1)

- Debenture of Market of The: ValueDocument5 pagesDebenture of Market of The: ValueRishabh jainNo ratings yet

- Answers No.1: Muaja, Mita Bella Lovely Virta Business Finance1 Assignment #01 Chapter 02Document2 pagesAnswers No.1: Muaja, Mita Bella Lovely Virta Business Finance1 Assignment #01 Chapter 02saya siapa?No ratings yet

- Chapter 1 - 4Document27 pagesChapter 1 - 4Joyce Dela CruzNo ratings yet

- Module 2 - Merger & AcquisitionDocument3 pagesModule 2 - Merger & AcquisitionkarmaudeNo ratings yet

- Why Choosing Spac Over IpoDocument6 pagesWhy Choosing Spac Over IpoNNo ratings yet

- Handbook For Series B & C FundraisingDocument28 pagesHandbook For Series B & C Fundraisingmac phoNo ratings yet

- Accounts ReceivableDocument3 pagesAccounts ReceivableJocel CaoNo ratings yet

- Jason's Farm Budget For 2021/22Document2 pagesJason's Farm Budget For 2021/22喜び エイプリルジョイNo ratings yet

- Deliveroo IPO 10 March 2021Document21 pagesDeliveroo IPO 10 March 2021juNo ratings yet

- Aud1 022424 LectureDocument1 pageAud1 022424 LectureJessie PaterezNo ratings yet

- Decision Tree ExampleDocument2 pagesDecision Tree Examplemuhammad saadNo ratings yet

- Merchandising ACTIVITY 2Document17 pagesMerchandising ACTIVITY 2Nermeen C. AlapaNo ratings yet

- Assignment 3 Module 3Document3 pagesAssignment 3 Module 3Andrea Joyce V. ClaveriaNo ratings yet

- 2020 Investor DayDocument19 pages2020 Investor Dayzl972098576No ratings yet

- Companies: Formation and Operations Companies: Formation and OperationsDocument35 pagesCompanies: Formation and Operations Companies: Formation and Operationsagrawalrohit_228384No ratings yet

- Kev 2Document11 pagesKev 2adam burdNo ratings yet

- TECHFWDocument13 pagesTECHFWHarry SprattNo ratings yet

- Teladoc Health, Inc. (TDOC) : Truist SecuritiesDocument8 pagesTeladoc Health, Inc. (TDOC) : Truist SecuritiesPramod BeriNo ratings yet

- Project Charter Example New ProductDocument5 pagesProject Charter Example New ProductKhushbu IndreshNo ratings yet

- Real Time Billionaires - Nigeria - 2024-04-24Document3 pagesReal Time Billionaires - Nigeria - 2024-04-24Mr JNo ratings yet

- Whistler Blackcomb Sell PitchDocument8 pagesWhistler Blackcomb Sell Pitchawesomeamy071No ratings yet

- The Maltese FalcoinDocument31 pagesThe Maltese FalcoinJustusvdMerweNo ratings yet

- Sinch 2020Q3 PresentationDocument32 pagesSinch 2020Q3 PresentationShivanandNo ratings yet

- Liquidation of PartnershipDocument10 pagesLiquidation of PartnershipCrislyn DacdacNo ratings yet

- Money - December 2015 VK Com EnglishmagazinesDocument92 pagesMoney - December 2015 VK Com EnglishmagazinesshyamsailusNo ratings yet

- s2 EthereumDocument62 pagess2 EthereummisfitsldswNo ratings yet

- s4 DeFiDocument44 pagess4 DeFimisfitsldswNo ratings yet

- DL2.1 - AIQC - Chapter2 Case Study - US Vs PRCDocument49 pagesDL2.1 - AIQC - Chapter2 Case Study - US Vs PRCmisfitsldswNo ratings yet

- DL2.3 - TTP and FTX DiscussionsDocument5 pagesDL2.3 - TTP and FTX DiscussionsmisfitsldswNo ratings yet

- 3b Asyraf Wajdi DusukiDocument21 pages3b Asyraf Wajdi DusukispucilbrozNo ratings yet

- Tsys Mpa With Logo 1Document6 pagesTsys Mpa With Logo 1api-503333470No ratings yet

- TD New AWC at Ambedkar NagarDocument134 pagesTD New AWC at Ambedkar NagarAbu MariamNo ratings yet

- The Nazi Fiscal CliffDocument22 pagesThe Nazi Fiscal CliffpipeburstNo ratings yet

- Bank Recon and PCFDocument2 pagesBank Recon and PCFAiza Ordoño0% (1)

- Cedacri International C P: Ompany RofileDocument26 pagesCedacri International C P: Ompany RofilegicucalanceaNo ratings yet

- How Bank Makes MoneyDocument2 pagesHow Bank Makes MoneyudaykumarNo ratings yet

- Coop. Project - Doc12Document78 pagesCoop. Project - Doc12PriyankaThakurNo ratings yet

- Hban 2018 AraDocument180 pagesHban 2018 AraMoinul HasanNo ratings yet

- 3 Calcul Coc Level III - 2 (Yetesera)Document6 pages3 Calcul Coc Level III - 2 (Yetesera)rabbirraabullooNo ratings yet

- Florentina Bautista-Spille v. Nicorp Management and International Exchange Bank, GR No. 214057, Octoberr 19, 2015Document9 pagesFlorentina Bautista-Spille v. Nicorp Management and International Exchange Bank, GR No. 214057, Octoberr 19, 2015Cza PeñaNo ratings yet

- Chapter 27 - Cash ManagementDocument35 pagesChapter 27 - Cash Managementmalek99No ratings yet

- Amit Sadhukhan.: CONTACT NO.: 9830671718 E-MAIL: Amit - Sadhukhan2005@yahoo - Co.inDocument3 pagesAmit Sadhukhan.: CONTACT NO.: 9830671718 E-MAIL: Amit - Sadhukhan2005@yahoo - Co.inAmit171984No ratings yet

- Lecture 3 - Banks and Other Financial InstitutionsDocument33 pagesLecture 3 - Banks and Other Financial Institutionsn nNo ratings yet

- Boards and Shareholders in European Listed Companies PDFDocument454 pagesBoards and Shareholders in European Listed Companies PDFМилена СпасовскаNo ratings yet

- A Project Report On Financial Performance Based On Ratios at HDFC BankDocument75 pagesA Project Report On Financial Performance Based On Ratios at HDFC Banksudam merya100% (1)

- Adani Green Energy Limited - Information Memorandum PDFDocument379 pagesAdani Green Energy Limited - Information Memorandum PDFRAKESH BABUNo ratings yet

- Error Messages EngDocument4,954 pagesError Messages EngVanitha raoNo ratings yet

- Work Life Balance of Employees and Its Effect On Work Related Factors in Nationalized BanksDocument8 pagesWork Life Balance of Employees and Its Effect On Work Related Factors in Nationalized BanksPrakaash RaajNo ratings yet

- 3Q18 Atlanta LARDocument4 pages3Q18 Atlanta LARAnonymous Feglbx5No ratings yet

- Issue of Capital Rules 2001Document3 pagesIssue of Capital Rules 2001Al NahiyanNo ratings yet

- Polikanti Goutham Krishna Cloud Data Engineer - Aws Certified DeveloperDocument4 pagesPolikanti Goutham Krishna Cloud Data Engineer - Aws Certified DeveloperPolikanti GouthamNo ratings yet

- Working in Transition To A Kinder WorldDocument93 pagesWorking in Transition To A Kinder Worldkaren hudesNo ratings yet

- Document Checklist: Joint Venture / Sole-Proprietor / Unincorporated BodyDocument20 pagesDocument Checklist: Joint Venture / Sole-Proprietor / Unincorporated BodyEDWARD LEENo ratings yet

- 128450-1993-Philippine National Bank v. Court of AppealsDocument9 pages128450-1993-Philippine National Bank v. Court of AppealsJulius ManaloNo ratings yet

- Shouryapuram vs. Mohit Kumar Arora ComplaintDocument17 pagesShouryapuram vs. Mohit Kumar Arora Complaintzuhaib habib100% (1)

- ToyworldDocument3 pagesToyworldVinay MohanNo ratings yet

- Audit of Liabilities MCQDocument7 pagesAudit of Liabilities MCQEISEN BELWIGANNo ratings yet