Download as pptx, pdf, or txt

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- 7 Percentage TaxesDocument38 pages7 Percentage Taxesqaz qwertyNo ratings yet

- Contract 2 MCQDocument8 pagesContract 2 MCQSumit Bhardwaj60% (5)

- Cpar Tax Problems ReviewerDocument8 pagesCpar Tax Problems ReviewerAnonymous swtSOYwLrMNo ratings yet

- Percentage TaxesDocument8 pagesPercentage TaxesTokha YatsurugiNo ratings yet

- BUSTAX Notes M4-5Document12 pagesBUSTAX Notes M4-5Rosette TuazonNo ratings yet

- Lecture 7 - Other Percentage TaxDocument3 pagesLecture 7 - Other Percentage TaxJeffrey BionaNo ratings yet

- Lecture 7 - Other Percentage TaxDocument3 pagesLecture 7 - Other Percentage TaxJohn Felix Morelos DoldolNo ratings yet

- 23.+Other+Percentage+Tax-REVISED+2023-classroom+discussion - Students 2Document55 pages23.+Other+Percentage+Tax-REVISED+2023-classroom+discussion - Students 2Aristeia NotesNo ratings yet

- Other Percentage TaxesDocument40 pagesOther Percentage TaxesKay Hanalee Villanueva NorioNo ratings yet

- Percentage TaxDocument17 pagesPercentage TaxPrincess Jay NacorNo ratings yet

- Percentage Tax and VATDocument15 pagesPercentage Tax and VATanyonghasayu30No ratings yet

- Other Percentage Taxes (OPT)Document56 pagesOther Percentage Taxes (OPT)Vince ManahanNo ratings yet

- Tax Table-Individuals-2022Document2 pagesTax Table-Individuals-2022Xandredg Sumpt LatogNo ratings yet

- Input Vat Credits, Refunds and Mixed Business TransactionsDocument4 pagesInput Vat Credits, Refunds and Mixed Business Transactionssara sibumaNo ratings yet

- Percentage Taxes UstDocument5 pagesPercentage Taxes UstGabriel PonceNo ratings yet

- Non Resident CitizensDocument3 pagesNon Resident CitizensJessa Belle EubionNo ratings yet

- Forecast in Taxation Law: Atty. Raegan L. CapunoDocument47 pagesForecast in Taxation Law: Atty. Raegan L. CapunoFrance SanchezNo ratings yet

- TAX - Individual TaxationDocument40 pagesTAX - Individual TaxationErika Mae LegaspiNo ratings yet

- Percentage Tax Description: Under Sections 116 To 126 of The Tax Code, As AmendedDocument4 pagesPercentage Tax Description: Under Sections 116 To 126 of The Tax Code, As AmendedAndrea TanNo ratings yet

- HumRes TaxDocument3 pagesHumRes TaxJob Noel BernardoNo ratings yet

- Train LawDocument41 pagesTrain LawJoana Lyn GalisimNo ratings yet

- Business Tax SummaryDocument10 pagesBusiness Tax SummaryJohn Raymond MarzanNo ratings yet

- Other Percentage Tax DraftDocument9 pagesOther Percentage Tax Draftbeadineros8No ratings yet

- Other Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateDocument18 pagesOther Percentage Tax Summary of Other Percentage Tax Rates: Coverage Taxable Base Tax RateZaaavnn VannnnnNo ratings yet

- O o o O: Percentage Tax DescriptionDocument3 pagesO o o O: Percentage Tax Descriptionscartoneros_1No ratings yet

- Classification of Individual Taxpayers:: Income Tax RatesDocument21 pagesClassification of Individual Taxpayers:: Income Tax RatesAngelica E. RefuerzoNo ratings yet

- Summary of Final Tax Under The Nirc, As Amended Individual Citizen AlienDocument16 pagesSummary of Final Tax Under The Nirc, As Amended Individual Citizen AlienXiaoyu KensameNo ratings yet

- Inclusion in Gross IncomeDocument3 pagesInclusion in Gross IncomeHi HelloNo ratings yet

- What Is TRAIN?: Tax ReformDocument10 pagesWhat Is TRAIN?: Tax ReformZyki Zamora LacdaoNo ratings yet

- Module 3 Percentage TaxDocument10 pagesModule 3 Percentage TaxDay DreamNo ratings yet

- Tax Reform For Acceleration and Inclusion (Train Law) : Republic Act No. 10963Document41 pagesTax Reform For Acceleration and Inclusion (Train Law) : Republic Act No. 10963maricrisandem100% (2)

- Graduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeDocument9 pagesGraduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeKyle SubidoNo ratings yet

- Frequency of ReportingDocument5 pagesFrequency of ReportingNeriza maningasNo ratings yet

- Business Tax: Francis Ysabella S. BalagtasDocument6 pagesBusiness Tax: Francis Ysabella S. BalagtasFrancis Ysabella BalagtasNo ratings yet

- Regular Income Tax: (As Amended by TRAIN LAW)Document32 pagesRegular Income Tax: (As Amended by TRAIN LAW)Elle VernezNo ratings yet

- Percentage Tax Excise Tax Documentary Stamp: Taxation LawDocument23 pagesPercentage Tax Excise Tax Documentary Stamp: Taxation LawB-an Javelosa100% (1)

- Reviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%Document7 pagesReviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%LeeshNo ratings yet

- Pa Tax Brief - March 2018Document11 pagesPa Tax Brief - March 2018Teresita TibayanNo ratings yet

- Module 4 Optional Tax Rate For Self EmployedDocument7 pagesModule 4 Optional Tax Rate For Self EmployedJam HailNo ratings yet

- Chapter 9 Other Percentage TaxesDocument56 pagesChapter 9 Other Percentage TaxesKarylle BartolayNo ratings yet

- BIR Form 2551Q: Quarterly Percentage TaxDocument8 pagesBIR Form 2551Q: Quarterly Percentage TaxAngelyn SamandeNo ratings yet

- BAC103A-02c Income Tax For Individuals Week 8Document4 pagesBAC103A-02c Income Tax For Individuals Week 8Novelyn Degones DuyoganNo ratings yet

- Taxes 1Document2 pagesTaxes 1HappyPurpleNo ratings yet

- TAXATION - Value-Added TaxDocument10 pagesTAXATION - Value-Added TaxJohn Mahatma Agripa100% (2)

- Copy Individual Income TaxDocument10 pagesCopy Individual Income TaxMari Louis Noriell MejiaNo ratings yet

- Withholding TaxDocument20 pagesWithholding TaxAngela CanayaNo ratings yet

- Types of Income and Corresponding Tax RatesDocument13 pagesTypes of Income and Corresponding Tax RatesJessa Belle EubionNo ratings yet

- Module 7 Tax On IndividualsDocument25 pagesModule 7 Tax On IndividualsAbegail Jenn Elis MulderNo ratings yet

- Transfer and Business Taxation - MIDTERMDocument14 pagesTransfer and Business Taxation - MIDTERMYvette Pauline JovenNo ratings yet

- Taxation Reviewer - Percentage TaxDocument3 pagesTaxation Reviewer - Percentage TaxDaphne BarceNo ratings yet

- RC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeDocument7 pagesRC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeGwyneth GloriaNo ratings yet

- Tax ExhibitsDocument4 pagesTax ExhibitsJM BermudoNo ratings yet

- CH10 Pecentage TaxDocument16 pagesCH10 Pecentage Taxwilma olivoNo ratings yet

- Enotes 10 Percentage TaxDocument12 pagesEnotes 10 Percentage TaxIrish Gracielle Dela CruzNo ratings yet

- Percentage Tax CTBDocument16 pagesPercentage Tax CTBDon CabasiNo ratings yet

- Percentage Tax: Percentage Tax Is A Business Tax Imposed On Persons, Entities, or TransactionsDocument16 pagesPercentage Tax: Percentage Tax Is A Business Tax Imposed On Persons, Entities, or TransactionsDon CabasiNo ratings yet

- Graduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeDocument9 pagesGraduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeFrancis Kyle Cagalingan SubidoNo ratings yet

- Quarterly Percentage Tax Rates Table: Taxable Base Tax RateDocument4 pagesQuarterly Percentage Tax Rates Table: Taxable Base Tax RateKathrine CruzNo ratings yet

- Business and Transfer TaxationDocument5 pagesBusiness and Transfer TaxationElizabeth OlaNo ratings yet

- A Case Study On Starbucks - PpsDocument78 pagesA Case Study On Starbucks - PpsNiravNo ratings yet

- Glorvina Constant InformationDocument4 pagesGlorvina Constant Informationmtuccitto100% (1)

- ERM PresentationDocument12 pagesERM PresentationRao ArsalanNo ratings yet

- Supreme Court: Vicente R. Layawen For Petitioner. Lawrence L. Fernandez & Associates For Private RespondentDocument5 pagesSupreme Court: Vicente R. Layawen For Petitioner. Lawrence L. Fernandez & Associates For Private RespondentPebs DrlieNo ratings yet

- Form 1: Basic Living Trust For One PersonDocument12 pagesForm 1: Basic Living Trust For One PersonNonProphetInc100% (1)

- 121000006-891204055639 - Product Disclosure SheetDocument10 pages121000006-891204055639 - Product Disclosure Sheetarvinp89No ratings yet

- Analysis of Insurance Sector With The Special Reference To Bajaj Allianz Life Insurance Co. by Ajay Singh Mertiya (Rathore)Document107 pagesAnalysis of Insurance Sector With The Special Reference To Bajaj Allianz Life Insurance Co. by Ajay Singh Mertiya (Rathore)Ajay Singh Rathore100% (3)

- Interim Kaiser Kern Admin AgreementDocument61 pagesInterim Kaiser Kern Admin AgreementUFCW770No ratings yet

- FepcDocument339 pagesFepcAnkur Dubey0% (1)

- Cashless Consent FormDocument1 pageCashless Consent FormM/s Microtech100% (1)

- InvoiceDocument2 pagesInvoicesravani ReddyNo ratings yet

- Resumen de Cuenta: Lorenzo Hernan Manuel Alberto Alberdi 754Document2 pagesResumen de Cuenta: Lorenzo Hernan Manuel Alberto Alberdi 754exuz27No ratings yet

- CGT 1Document96 pagesCGT 1UmbBNo ratings yet

- Unit 2Document3 pagesUnit 2Анна ОборочануNo ratings yet

- Project SellingDocument6 pagesProject SellingventuristaNo ratings yet

- Tata Consultancy PayslipDocument2 pagesTata Consultancy PayslipSitharth VkrNo ratings yet

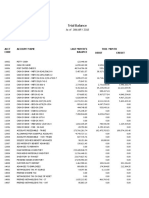

- ABC Co. Trial BalanceDocument10 pagesABC Co. Trial BalanceGraceeyNo ratings yet

- Cost To BritainDocument32 pagesCost To BritainShahzaibUsmanNo ratings yet

- Course Name: Marketing Management Topics: Types of Demand: AssignmentDocument6 pagesCourse Name: Marketing Management Topics: Types of Demand: AssignmentHasibur RahmanNo ratings yet

- Internship Report of Ayesha NiazDocument57 pagesInternship Report of Ayesha NiazNiaz ArainNo ratings yet

- CM2 Mock 7 Paper ADocument6 pagesCM2 Mock 7 Paper AVishva ThombareNo ratings yet

- Marsh Power Course October 2017Document2 pagesMarsh Power Course October 2017khurram95103No ratings yet

- California Department of Health Care Services: Strategic Plan 2013-2017Document13 pagesCalifornia Department of Health Care Services: Strategic Plan 2013-2017LailaTannoorNo ratings yet

- CROP Loan: B. Post-Harvest ExpensesDocument9 pagesCROP Loan: B. Post-Harvest ExpensesRuchi ChaudharyNo ratings yet

- Tax Rates Card 2023 GC - 220819 - 230837Document5 pagesTax Rates Card 2023 GC - 220819 - 230837smnomanNo ratings yet

- About Our Insurance Services: Who Are We? Who Regulates UsDocument3 pagesAbout Our Insurance Services: Who Are We? Who Regulates UsSian MilesNo ratings yet

- ScheduleofCost PractiseQuestionDocument3 pagesScheduleofCost PractiseQuestionbharteshdas100% (2)

- Tutorial Week 3 QuestionsDocument2 pagesTutorial Week 3 Questionsadri kusnoNo ratings yet

- Offer Letter Sasken Nancharaiah GudavalliDocument3 pagesOffer Letter Sasken Nancharaiah GudavalliNancharaiah SandyNo ratings yet