Download as ppt, pdf, or txt

You might also like

- Rotschild - Valuation and Modeling PDFDocument440 pagesRotschild - Valuation and Modeling PDFPaola Verdi100% (6)

- A Premium For Good GovernanceDocument5 pagesA Premium For Good GovernancelaloasisNo ratings yet

- AS 6 Depreciation Accounts ProjectDocument25 pagesAS 6 Depreciation Accounts Projectmansikothari198980% (15)

- Corporate GovernanceDocument43 pagesCorporate Governancem_dattaias100% (1)

- Corporate Governance and EtihcsDocument85 pagesCorporate Governance and EtihcsNeil GuptaNo ratings yet

- Lecture 4Document22 pagesLecture 4zaitul ubhNo ratings yet

- Good Governance: Key To Sustainability: Better Companies, Better SocietiesDocument26 pagesGood Governance: Key To Sustainability: Better Companies, Better SocietiessizziNo ratings yet

- S9 HandoutDocument12 pagesS9 Handoutshubham solankiNo ratings yet

- Corporate Governance Country Assessment PakistanDocument88 pagesCorporate Governance Country Assessment PakistanHannah RoseNo ratings yet

- Introduction To GCGDocument9 pagesIntroduction To GCG670620No ratings yet

- ACGS - PPT Materials - FINAL - 120519Document101 pagesACGS - PPT Materials - FINAL - 120519Tri WahyuniNo ratings yet

- Business Environment PPDocument10 pagesBusiness Environment PPChau VuongNo ratings yet

- 1 Introduction To Corporate GovernanceDocument66 pages1 Introduction To Corporate GovernanceAnh Nguyen Le HongNo ratings yet

- Ar 2010Document272 pagesAr 2010Shehani ThilakshikaNo ratings yet

- ICICI Securities Ltd. Campus Placement - FY 24Document15 pagesICICI Securities Ltd. Campus Placement - FY 24Ritik vermaNo ratings yet

- Capital Markets Governance of CorporatesDocument23 pagesCapital Markets Governance of CorporatesJonathan WenNo ratings yet

- 2012Document304 pages2012FaridmarufNo ratings yet

- Strategic Management BBA3254 0 Lecture 8 Stakeholders 1Document18 pagesStrategic Management BBA3254 0 Lecture 8 Stakeholders 1CCSB CCSBNo ratings yet

- Indian CG Scorecard PDFDocument91 pagesIndian CG Scorecard PDFJill MehtaNo ratings yet

- Deloitte Uk Gif Internal Control and The Board November 2019Document8 pagesDeloitte Uk Gif Internal Control and The Board November 2019ahamidianNo ratings yet

- Pitchbook - CompleteDocument28 pagesPitchbook - CompleteDee100% (1)

- Chapter 1 Governance - Ballada-MergedDocument94 pagesChapter 1 Governance - Ballada-MergedUnnamed homosapienNo ratings yet

- Corporate Governance - Support Slides FINALDocument28 pagesCorporate Governance - Support Slides FINALAbdullah ZakariyyaNo ratings yet

- E2A Business Models and Value CreationDocument30 pagesE2A Business Models and Value Creationnthabikoena118No ratings yet

- Man IndustriesDocument53 pagesMan IndustriesAnirudhNo ratings yet

- 5 Corporate GovernanceDocument29 pages5 Corporate GovernanceAlok SinghNo ratings yet

- Chapter 2 (Developing Marketing Strategies and Plans)Document29 pagesChapter 2 (Developing Marketing Strategies and Plans)Magued MamdouhNo ratings yet

- Corporate Governance: 2021 Faculty of Business ManagementDocument66 pagesCorporate Governance: 2021 Faculty of Business ManagementPhuong ThanhNo ratings yet

- SM Chapter 3 Key Words - PDFDocument48 pagesSM Chapter 3 Key Words - PDFVikramNo ratings yet

- Deepanshucv & RDocument15 pagesDeepanshucv & RDeepanshu PathakNo ratings yet

- Corporate Entrepreneurship & Innovation: Michael H. Morris Donald F. Kuratko Jeffrey G. CovinDocument24 pagesCorporate Entrepreneurship & Innovation: Michael H. Morris Donald F. Kuratko Jeffrey G. Covinsarbaz0003No ratings yet

- Figure 1: Enterprises Studied by SurveyDocument2 pagesFigure 1: Enterprises Studied by SurveyVasu PatelNo ratings yet

- Slides - CF01-010 Corporate Governance and ESG - Corporate Governance Overview and Stakeholder GroupsDocument19 pagesSlides - CF01-010 Corporate Governance and ESG - Corporate Governance Overview and Stakeholder GroupsbiaNo ratings yet

- Investment Banking Pitchbook TemplateDocument27 pagesInvestment Banking Pitchbook TemplateElie Yabroudi100% (1)

- Deloitte Uk Audit Internal Controls Whats All The Fuss About June 2021Document8 pagesDeloitte Uk Audit Internal Controls Whats All The Fuss About June 2021Anand RajNo ratings yet

- Presentation - 29 Sep 10 Jar v4Document28 pagesPresentation - 29 Sep 10 Jar v4Jarren LimNo ratings yet

- Chapter 1 Introduction Corporate GovernanceDocument14 pagesChapter 1 Introduction Corporate GovernanceHM.No ratings yet

- Day 1 3wb Busuioc EngDocument33 pagesDay 1 3wb Busuioc EngmodoumsNo ratings yet

- SCNL Investor PPT - Q2 FY20Document69 pagesSCNL Investor PPT - Q2 FY20fghjmkNo ratings yet

- Cgri Quick Guide 01 Introduction Corporate GovernanceDocument13 pagesCgri Quick Guide 01 Introduction Corporate GovernanceJonathan KakombohiNo ratings yet

- FGV Berhad-Annual Integrated Report 2022Document100 pagesFGV Berhad-Annual Integrated Report 2022Noriyuki TanakaNo ratings yet

- 23 Annual Report 2021-22Document196 pages23 Annual Report 2021-22Akshat Sharma Roll no 21No ratings yet

- Corporate Governance & Capital Markets: Augustues P. LambinoDocument74 pagesCorporate Governance & Capital Markets: Augustues P. LambinoAnn Gloghienette Orais PerezNo ratings yet

- BNL 42nd Annual Report 2076 77Document184 pagesBNL 42nd Annual Report 2076 77amatyaadibeshNo ratings yet

- Comprehansive Process. TamerDocument2 pagesComprehansive Process. TamerMarco IbrahimNo ratings yet

- Problem Solving PresDocument121 pagesProblem Solving Presaishah farahNo ratings yet

- Private Equity and Venture Capital in Europe Marke... - (Part 4 Managing A Private Equity Investment)Document14 pagesPrivate Equity and Venture Capital in Europe Marke... - (Part 4 Managing A Private Equity Investment)94umerbashirNo ratings yet

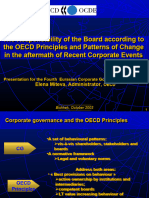

- The Responsibility of The Board According To The OECD Principles and Patterns of Change in The Aftermath of Recent Corporate EventsDocument16 pagesThe Responsibility of The Board According To The OECD Principles and Patterns of Change in The Aftermath of Recent Corporate Eventsgi4615No ratings yet

- Course-Outline Special Topics in FMDocument4 pagesCourse-Outline Special Topics in FMYca BlchNo ratings yet

- Tamim Fund Global High Conviction - Summary 2021Document3 pagesTamim Fund Global High Conviction - Summary 2021dkatzNo ratings yet

- Orientation To Management StudyDocument6 pagesOrientation To Management StudyDương Ngọc TrânNo ratings yet

- Corporate Governance OverviewDocument16 pagesCorporate Governance OverviewBie RenNo ratings yet

- The Operations Function Is Fashionable!: The Consultancy Services Market % of World Revenues of 40 Largest FirmsDocument16 pagesThe Operations Function Is Fashionable!: The Consultancy Services Market % of World Revenues of 40 Largest FirmsRahul BiswasNo ratings yet

- Process: For Institutional One-On-One Use OnlyDocument16 pagesProcess: For Institutional One-On-One Use OnlyABermNo ratings yet

- Chapter 1-Introduction To Corporate GovernanceDocument14 pagesChapter 1-Introduction To Corporate GovernanceflamNo ratings yet

- AnnualReport2021 AVIA Att1Document268 pagesAnnualReport2021 AVIA Att1Kusuma AntaraNo ratings yet

- Beyond Governance: Creating Corporate Value through Performance, Conformance and ResponsibilityFrom EverandBeyond Governance: Creating Corporate Value through Performance, Conformance and ResponsibilityNo ratings yet

- Braced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationFrom EverandBraced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationNo ratings yet

- 罗兰贝格-To become a leading brand in the water heater market in China(Bosch Thermotechnik Discussion paperII)Document42 pages罗兰贝格-To become a leading brand in the water heater market in China(Bosch Thermotechnik Discussion paperII)Jonathan WenNo ratings yet

- 罗兰贝格-To become a leading brand in the water heater market in China(Bosch Thermotechnik Discussion paperIII)Document56 pages罗兰贝格-To become a leading brand in the water heater market in China(Bosch Thermotechnik Discussion paperIII)Jonathan WenNo ratings yet

- 罗兰贝格-To become a leading brand of the water heater market in China(Bosch Thernotechnik Discussion paper I)Document32 pages罗兰贝格-To become a leading brand of the water heater market in China(Bosch Thernotechnik Discussion paper I)Jonathan WenNo ratings yet

- Build an enterprise solution sales forceDocument77 pagesBuild an enterprise solution sales forceJonathan WenNo ratings yet

- PMIIssue3cDocument31 pagesPMIIssue3cJonathan WenNo ratings yet

- 加入WTO后中国汽车十大趋势Document89 pages加入WTO后中国汽车十大趋势Jonathan WenNo ratings yet

- Banking in The Supply Chain - WeissDocument31 pagesBanking in The Supply Chain - WeissJonathan WenNo ratings yet

- Day 2_12.00_McKinsey & CoDocument43 pagesDay 2_12.00_McKinsey & CoJonathan WenNo ratings yet

- SCP ModelDocument17 pagesSCP ModelJonathan WenNo ratings yet

- Effective Capacity Building Nonprofit OrganizationsDocument24 pagesEffective Capacity Building Nonprofit OrganizationsJonathan WenNo ratings yet

- ZXG779 Auto-Assembly 1-Daydx 6 011502Document27 pagesZXG779 Auto-Assembly 1-Daydx 6 011502Jonathan WenNo ratings yet

- Capacity Optimization WPDocument2 pagesCapacity Optimization WPJonathan WenNo ratings yet

- Capital Expenditure ReductionDocument7 pagesCapital Expenditure ReductionJonathan WenNo ratings yet

- Bain Health CareDocument41 pagesBain Health CareJonathan WenNo ratings yet

- Profit Hunt FrameworkDocument8 pagesProfit Hunt FrameworkJonathan WenNo ratings yet

- 5 WhyDocument2 pages5 WhyJonathan WenNo ratings yet

- What: Dos:: PA-6-PD-GB-TOOL KIT-990421-OCDocument7 pagesWhat: Dos:: PA-6-PD-GB-TOOL KIT-990421-OCJonathan WenNo ratings yet

- CONFLICTRESOLUTIONDocument4 pagesCONFLICTRESOLUTIONJonathan WenNo ratings yet

- Relative Competitor EconomicsDocument16 pagesRelative Competitor EconomicsJonathan WenNo ratings yet

- BOC TradeFinanceApproachDocument78 pagesBOC TradeFinanceApproachJonathan WenNo ratings yet

- Root Cause AnalysisDocument25 pagesRoot Cause AnalysisJonathan WenNo ratings yet

- A4. Product Strategy - Vertical Solutions - EDocument11 pagesA4. Product Strategy - Vertical Solutions - EJonathan WenNo ratings yet

- Reengineering CookbookDocument38 pagesReengineering CookbookJonathan WenNo ratings yet

- Overhead Optimization WPDocument2 pagesOverhead Optimization WPJonathan WenNo ratings yet

- STRATEGYDEVELOPMENTDocument7 pagesSTRATEGYDEVELOPMENTJonathan WenNo ratings yet

- ORDERTOCASHDocument17 pagesORDERTOCASHJonathan WenNo ratings yet

- CPRLEADERSHIPSTRUCTUREDocument4 pagesCPRLEADERSHIPSTRUCTUREJonathan WenNo ratings yet

- SHOULDBEFACTBOOKDocument57 pagesSHOULDBEFACTBOOKJonathan WenNo ratings yet

- APPROVALPROCESSDocument9 pagesAPPROVALPROCESSJonathan WenNo ratings yet

- REDESIGNEXPERTNOTESDocument19 pagesREDESIGNEXPERTNOTESJonathan WenNo ratings yet

- DR Reddy Lab 5 Year DataDocument4 pagesDR Reddy Lab 5 Year Datashishir5087No ratings yet

- Format of Cash Flow StatementDocument3 pagesFormat of Cash Flow StatementMoses Fernandes100% (1)

- Calculating Incremental ROIC's: Corner of Berkshire & Fairfax - NYC Meetup October 14, 2017Document19 pagesCalculating Incremental ROIC's: Corner of Berkshire & Fairfax - NYC Meetup October 14, 2017Anil GowdaNo ratings yet

- Study On Equity Diversified Mutual Fund Schemes in IndiaDocument16 pagesStudy On Equity Diversified Mutual Fund Schemes in IndiaShashwat ShrivastavaNo ratings yet

- Polycab India Limited PDFDocument659 pagesPolycab India Limited PDFpooja100% (1)

- Capital StructureDocument91 pagesCapital StructureAman PoddarNo ratings yet

- Level 1 - Pratham - Introduction To Financial Planning - 0Document29 pagesLevel 1 - Pratham - Introduction To Financial Planning - 0Pulipaka NimeshikaNo ratings yet

- UltraTech Cement LTD Financial AnalysisDocument26 pagesUltraTech Cement LTD Financial AnalysisSayon DasNo ratings yet

- 1.1 Introduction To TopicDocument55 pages1.1 Introduction To Topickunal bankheleNo ratings yet

- Capital Letter Mar10Document4 pagesCapital Letter Mar10satish kumarNo ratings yet

- MBA 511 Final ReportDocument13 pagesMBA 511 Final ReportSifatShoaebNo ratings yet

- Real Estate Finance Presentation PDFDocument10 pagesReal Estate Finance Presentation PDFEsther LeeNo ratings yet

- LAPD-CGT-G01 - Comprehensive Guide To Capital Gains Tax PDFDocument938 pagesLAPD-CGT-G01 - Comprehensive Guide To Capital Gains Tax PDFKriben RaoNo ratings yet

- PFRS 9Document1 pagePFRS 9Ella MaeNo ratings yet

- Safal Niveshak Stock Analysis Excel Ver 50 How To Use This Spreadsheet PDF FreeDocument49 pagesSafal Niveshak Stock Analysis Excel Ver 50 How To Use This Spreadsheet PDF Freeraj110100% (1)

- Module 1 Monetary System and Financial System OverviewDocument4 pagesModule 1 Monetary System and Financial System OverviewShaira Leyson MaturanNo ratings yet

- Key Investor Information: Class A Accumulation Units The HL Multi-Manager Balanced Managed Trust ("The Fund")Document2 pagesKey Investor Information: Class A Accumulation Units The HL Multi-Manager Balanced Managed Trust ("The Fund")Merabharat BharatNo ratings yet

- ETF Portfolio Details - Saxo Bank - Balanced Portfolio Description 2013Document8 pagesETF Portfolio Details - Saxo Bank - Balanced Portfolio Description 2013Bruno Dias da CostaNo ratings yet

- Mergers and Acquisitions in Pharmaceutical IndustryDocument13 pagesMergers and Acquisitions in Pharmaceutical IndustryMuhammad sabir shahzadNo ratings yet

- WRTNM 0001Document1 pageWRTNM 0001p srivastavaNo ratings yet

- The City Bank Ltd.Document34 pagesThe City Bank Ltd.Shamsuddin AhmedNo ratings yet

- Financial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreDocument18 pagesFinancial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreAnirban Roy ChowdhuryNo ratings yet

- Investment Analysis of Marginal FieldsDocument39 pagesInvestment Analysis of Marginal FieldssegunoyesNo ratings yet

- Women InvestorsDocument9 pagesWomen InvestorsAngel ChopraNo ratings yet

- Australian Corporate Tax Rate: Local Income TaxesDocument35 pagesAustralian Corporate Tax Rate: Local Income TaxesNadine DiamanteNo ratings yet

- Fama French PDFDocument8 pagesFama French PDFMonzer ShkeirNo ratings yet

- Introduction To Partnership AccountingDocument16 pagesIntroduction To Partnership Accountingmachelle franciscoNo ratings yet

- PT Pandawa Prima Lestari PT Pandawa Prima Lestari: Executive SummaryDocument14 pagesPT Pandawa Prima Lestari PT Pandawa Prima Lestari: Executive SummaryikaspuspasariNo ratings yet

- (Slivap - Ru) 10winning - Strategies PDFDocument45 pages(Slivap - Ru) 10winning - Strategies PDFPetr TsesarNo ratings yet