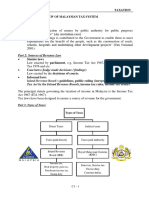

Chapter 1 Introduction To Taxation BKAT2013

Chapter 1 Introduction To Taxation BKAT2013

You might also like

- Chap 1 Basis of Malaysian Income Tax 2022Document7 pagesChap 1 Basis of Malaysian Income Tax 2022Jasne OczyNo ratings yet

- GST Impact On Indian Textile IndustryDocument33 pagesGST Impact On Indian Textile IndustryHarsh Gautam100% (6)

- Introduction To Malaysian Taxation SystemDocument25 pagesIntroduction To Malaysian Taxation Systemhrtn.100% (1)

- Resource Collection Model of The GovernmentDocument18 pagesResource Collection Model of The GovernmentSarita BhandariNo ratings yet

- Intro To Msian Taxation - 2023 (Week 1)Document13 pagesIntro To Msian Taxation - 2023 (Week 1)leery-wb22No ratings yet

- GST FrameworkDocument21 pagesGST FrameworkExecutive EngineerNo ratings yet

- Input Tax Credit-Cp8Document118 pagesInput Tax Credit-Cp8Shipra SonaliNo ratings yet

- 2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesDocument972 pages2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesRadhakrishnaraja RameshNo ratings yet

- Suraj Sir 1Document8 pagesSuraj Sir 1Avinash YadavNo ratings yet

- GST Questions and ConceptsDocument52 pagesGST Questions and ConceptsShefali TailorNo ratings yet

- Why Invest in PY - March - 23Document13 pagesWhy Invest in PY - March - 23Ana GarridoNo ratings yet

- 4 Chapter04Document40 pages4 Chapter04Kalkidan ZerihunNo ratings yet

- Concept of Input Tax Credit: © Indirect Taxes Committee, ICAIDocument35 pagesConcept of Input Tax Credit: © Indirect Taxes Committee, ICAIyennamNo ratings yet

- Ey Budget 2023 Technology SectorDocument6 pagesEy Budget 2023 Technology SectorAditya BajoriaNo ratings yet

- 6 ItcDocument114 pages6 ItcRAUNAQ SHARMANo ratings yet

- 66519bos53752 cp6Document100 pages66519bos53752 cp6Aditya ThesiaNo ratings yet

- Chapter 1 - Introduction To GST: Applicability of Utgst ActDocument7 pagesChapter 1 - Introduction To GST: Applicability of Utgst ActSoul of honeyNo ratings yet

- HAC - Tax Memorandum 2022-23-FinalDocument18 pagesHAC - Tax Memorandum 2022-23-FinalAsad ZahidNo ratings yet

- 18 GSTDocument1,042 pages18 GSTSwetaNo ratings yet

- GST NotesDocument62 pagesGST NotesSHANKAR GUDDADNo ratings yet

- Inpu T Tax CRE Dit!: Week 6Document39 pagesInpu T Tax CRE Dit!: Week 6himeesha dhiliwalNo ratings yet

- Miss. Dipti Dipak Patil: Taxation As A Significant Tool For Economic DevelopmentDocument70 pagesMiss. Dipti Dipak Patil: Taxation As A Significant Tool For Economic DevelopmentGKNo ratings yet

- Quarterly Report March 2020 1Document16 pagesQuarterly Report March 2020 1Meera KhanNo ratings yet

- Fasd 2012 2016 Firs ReportDocument9 pagesFasd 2012 2016 Firs Reporthabibaamin951No ratings yet

- Bangladesh Tax Guide 2023 Second Edition 110923Document44 pagesBangladesh Tax Guide 2023 Second Edition 110923jahidulislam53062No ratings yet

- Pratical Tax Guide 2022Document19 pagesPratical Tax Guide 2022levis BilossiNo ratings yet

- Finance Act Era Critical Evaluation 1 1Document22 pagesFinance Act Era Critical Evaluation 1 1Folawiyo AgbokeNo ratings yet

- Indirect Tax Revision Notes-CS Exe June 23 Lyst3130Document56 pagesIndirect Tax Revision Notes-CS Exe June 23 Lyst3130tskpestsolutions.chennaiNo ratings yet

- Input Tax Credit Under GSTDocument4 pagesInput Tax Credit Under GSTharshadaphandge165No ratings yet

- EY Tax Bulletin Apr 2014Document15 pagesEY Tax Bulletin Apr 2014Mobile LegendsNo ratings yet

- Taxflash 2023 01Document8 pagesTaxflash 2023 01Kasuma YeniNo ratings yet

- Ukat2023 Taxation I: Topic 1: Scope & Basis of Malaysian TaxationDocument62 pagesUkat2023 Taxation I: Topic 1: Scope & Basis of Malaysian TaxationEileen WongNo ratings yet

- Adobe Scan Oct 11, 2023Document9 pagesAdobe Scan Oct 11, 2023Amir HamzaNo ratings yet

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- Inter GST Chart Book Nov2022Document41 pagesInter GST Chart Book Nov2022Aastha ChauhanNo ratings yet

- Income Tax - Income Tax Guide 2023, Latest NewsDocument34 pagesIncome Tax - Income Tax Guide 2023, Latest NewsnandiniNo ratings yet

- Taxation ProjectDocument70 pagesTaxation ProjectMantsha SayyedNo ratings yet

- Business PlanDocument14 pagesBusiness PlanghadaNo ratings yet

- GST Charts by CA Deep Jain SirDocument41 pagesGST Charts by CA Deep Jain SirVINAY SHARMANo ratings yet

- PWC Vietnam PTB 2020 enDocument60 pagesPWC Vietnam PTB 2020 enaNo ratings yet

- WorkDocument8 pagesWorkGuerrero MetrashNo ratings yet

- Intouch Issue 3 2022Document21 pagesIntouch Issue 3 2022Shermadurai VNo ratings yet

- Taxation-Reforms PRESENTATIONDocument17 pagesTaxation-Reforms PRESENTATIONRaman KumarNo ratings yet

- Indirect TaxDocument14 pagesIndirect TaxAzulfa Sultan.No ratings yet

- GTU Tax UpdatesDocument30 pagesGTU Tax UpdatesNelson StarkNo ratings yet

- Laws and Practices of Income TaxDocument34 pagesLaws and Practices of Income TaxNibir RahmanNo ratings yet

- GST Notes Semester 6Document39 pagesGST Notes Semester 6Bhanu DangNo ratings yet

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- Tax Memorandum 2012 FinalDocument58 pagesTax Memorandum 2012 FinalAzka KhalidNo ratings yet

- PWC Vietnam PTB 2020 enDocument60 pagesPWC Vietnam PTB 2020 enngoba_cuongNo ratings yet

- Countries Enter Into Double Taxation TreatiesDocument1 pageCountries Enter Into Double Taxation TreatiesavsharikaNo ratings yet

- Flash NewsDocument3 pagesFlash Newslingesh1892No ratings yet

- 74822bos60500 cp13Document48 pages74822bos60500 cp13Looney ApacheNo ratings yet

- Goods and Services Tax - 2021Document43 pagesGoods and Services Tax - 2021gsvighneshnairNo ratings yet

- FOURTH SEMESTER GSTDocument6 pagesFOURTH SEMESTER GSTKenny PhilipsNo ratings yet

- CITN On Taxes Oil & GasDocument91 pagesCITN On Taxes Oil & GasEfosaUwaifoNo ratings yet

- Chapter 1 Overview of Malaysian Tax SystemDocument11 pagesChapter 1 Overview of Malaysian Tax SystemLOO YU HUANGNo ratings yet

- By Damodar Agrawal & Associates: Damodar06@yahoo - Co.inDocument374 pagesBy Damodar Agrawal & Associates: Damodar06@yahoo - Co.inNiteshNo ratings yet

- EY Tax Alert - Finance ActDocument8 pagesEY Tax Alert - Finance ActMarie Thomas AllenNo ratings yet

- PWC Vietnam Pocket Tax Book 2019 enDocument64 pagesPWC Vietnam Pocket Tax Book 2019 enBudsakorn SuwaphanwattanaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- GST NotesDocument156 pagesGST NotesNishthaNo ratings yet

- Mepco Online BillDocument1 pageMepco Online Billdes121dtNo ratings yet

- Research Paper On Tax System in PakistanDocument6 pagesResearch Paper On Tax System in Pakistanafeavbrpd100% (2)

- VILGST - SGST - High Court Cases - 2023-VIL-360-CALDocument6 pagesVILGST - SGST - High Court Cases - 2023-VIL-360-CALBhanuprakash GuptaNo ratings yet

- Ca Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTDocument7 pagesCa Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTkinnar2013No ratings yet

- Economic Survey 2018 Vol 1Document137 pagesEconomic Survey 2018 Vol 1bhargavNo ratings yet

- Idt Vol-1 May Nov 2021 Exam PDFDocument616 pagesIdt Vol-1 May Nov 2021 Exam PDFSri Pavan100% (1)

- GST Working May 2022Document20 pagesGST Working May 2022Chandrashekar BNo ratings yet

- Resume Harun RashidDocument2 pagesResume Harun RashidHARUN RASHIDNo ratings yet

- Application Form: Gurgaon Greens, Sector 102, GurugramDocument16 pagesApplication Form: Gurgaon Greens, Sector 102, GurugramsumitNo ratings yet

- Tnvat Form WW Fy 15-16Document30 pagesTnvat Form WW Fy 15-16samaadhuNo ratings yet

- List of Topics GST - IDocument7 pagesList of Topics GST - IArnav GargNo ratings yet

- Report ON Impact of GST On Logistics Industry in India Project Report Submitted in Partial Fulfillment For The Award of Degree ofDocument31 pagesReport ON Impact of GST On Logistics Industry in India Project Report Submitted in Partial Fulfillment For The Award of Degree ofakshara pradeepNo ratings yet

- DL018 Dharmaj Zee24K May 23-24Document1 pageDL018 Dharmaj Zee24K May 23-24onlyhitmanNo ratings yet

- Chapter 3 Charge Under GSTDocument10 pagesChapter 3 Charge Under GSTabhay javiyaNo ratings yet

- Impact of GST On E-CommerceDocument4 pagesImpact of GST On E-CommerceIJAERS JOURNALNo ratings yet

- Residence: Architectural Design ProposalDocument15 pagesResidence: Architectural Design ProposalAditi AgrawalNo ratings yet

- Goods and Service TaxDocument14 pagesGoods and Service TaxkejkarNo ratings yet

- Auto TestDocument3 pagesAuto TestMaree AlShehriNo ratings yet

- Draft - GO - 26 - 10 - 2017 - English - Final 2017 PDFDocument38 pagesDraft - GO - 26 - 10 - 2017 - English - Final 2017 PDFAnuj AroraNo ratings yet

- Chart of AccountDocument7 pagesChart of Accountacahalim1103No ratings yet

- GST Booklet KutchDocument34 pagesGST Booklet KutchBhavik MehtaNo ratings yet

- FoodnhotelDocument24 pagesFoodnhotelHoward TeowNo ratings yet

- LUT Cover LetterDocument2 pagesLUT Cover LetterJanhvi Kishori ThakkarNo ratings yet

- Skills Assessment Fees For Professional Occupations - VETASSESSDocument12 pagesSkills Assessment Fees For Professional Occupations - VETASSESSjeff665547No ratings yet

- Adobe Scan 26 Apr 2023Document2 pagesAdobe Scan 26 Apr 2023Shranish KarNo ratings yet

- Palkesh Asawa - S Answer To How Is GST Beneficial For The Country - How Would It Help To Improve The Country - S Economy - QuoraDocument3 pagesPalkesh Asawa - S Answer To How Is GST Beneficial For The Country - How Would It Help To Improve The Country - S Economy - QuoraAshit AgarwalNo ratings yet

- ReceiptDocument2 pagesReceiptshaikh rehmanNo ratings yet

- CA Final Vsi Jaipur IDT ABC Analysis For Nov 2023Document4 pagesCA Final Vsi Jaipur IDT ABC Analysis For Nov 2023Dharani SsNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Chap 1 Basis of Malaysian Income Tax 2022Document7 pagesChap 1 Basis of Malaysian Income Tax 2022Jasne OczyNo ratings yet

- GST Impact On Indian Textile IndustryDocument33 pagesGST Impact On Indian Textile IndustryHarsh Gautam100% (6)

- Introduction To Malaysian Taxation SystemDocument25 pagesIntroduction To Malaysian Taxation Systemhrtn.100% (1)

- Resource Collection Model of The GovernmentDocument18 pagesResource Collection Model of The GovernmentSarita BhandariNo ratings yet

- Intro To Msian Taxation - 2023 (Week 1)Document13 pagesIntro To Msian Taxation - 2023 (Week 1)leery-wb22No ratings yet

- GST FrameworkDocument21 pagesGST FrameworkExecutive EngineerNo ratings yet

- Input Tax Credit-Cp8Document118 pagesInput Tax Credit-Cp8Shipra SonaliNo ratings yet

- 2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesDocument972 pages2.2016 Syllabus Paper-18 - Jan21 Indirect Tax Laws & Practice Study NotesRadhakrishnaraja RameshNo ratings yet

- Suraj Sir 1Document8 pagesSuraj Sir 1Avinash YadavNo ratings yet

- GST Questions and ConceptsDocument52 pagesGST Questions and ConceptsShefali TailorNo ratings yet

- Why Invest in PY - March - 23Document13 pagesWhy Invest in PY - March - 23Ana GarridoNo ratings yet

- 4 Chapter04Document40 pages4 Chapter04Kalkidan ZerihunNo ratings yet

- Concept of Input Tax Credit: © Indirect Taxes Committee, ICAIDocument35 pagesConcept of Input Tax Credit: © Indirect Taxes Committee, ICAIyennamNo ratings yet

- Ey Budget 2023 Technology SectorDocument6 pagesEy Budget 2023 Technology SectorAditya BajoriaNo ratings yet

- 6 ItcDocument114 pages6 ItcRAUNAQ SHARMANo ratings yet

- 66519bos53752 cp6Document100 pages66519bos53752 cp6Aditya ThesiaNo ratings yet

- Chapter 1 - Introduction To GST: Applicability of Utgst ActDocument7 pagesChapter 1 - Introduction To GST: Applicability of Utgst ActSoul of honeyNo ratings yet

- HAC - Tax Memorandum 2022-23-FinalDocument18 pagesHAC - Tax Memorandum 2022-23-FinalAsad ZahidNo ratings yet

- 18 GSTDocument1,042 pages18 GSTSwetaNo ratings yet

- GST NotesDocument62 pagesGST NotesSHANKAR GUDDADNo ratings yet

- Inpu T Tax CRE Dit!: Week 6Document39 pagesInpu T Tax CRE Dit!: Week 6himeesha dhiliwalNo ratings yet

- Miss. Dipti Dipak Patil: Taxation As A Significant Tool For Economic DevelopmentDocument70 pagesMiss. Dipti Dipak Patil: Taxation As A Significant Tool For Economic DevelopmentGKNo ratings yet

- Quarterly Report March 2020 1Document16 pagesQuarterly Report March 2020 1Meera KhanNo ratings yet

- Fasd 2012 2016 Firs ReportDocument9 pagesFasd 2012 2016 Firs Reporthabibaamin951No ratings yet

- Bangladesh Tax Guide 2023 Second Edition 110923Document44 pagesBangladesh Tax Guide 2023 Second Edition 110923jahidulislam53062No ratings yet

- Pratical Tax Guide 2022Document19 pagesPratical Tax Guide 2022levis BilossiNo ratings yet

- Finance Act Era Critical Evaluation 1 1Document22 pagesFinance Act Era Critical Evaluation 1 1Folawiyo AgbokeNo ratings yet

- Indirect Tax Revision Notes-CS Exe June 23 Lyst3130Document56 pagesIndirect Tax Revision Notes-CS Exe June 23 Lyst3130tskpestsolutions.chennaiNo ratings yet

- Input Tax Credit Under GSTDocument4 pagesInput Tax Credit Under GSTharshadaphandge165No ratings yet

- EY Tax Bulletin Apr 2014Document15 pagesEY Tax Bulletin Apr 2014Mobile LegendsNo ratings yet

- Taxflash 2023 01Document8 pagesTaxflash 2023 01Kasuma YeniNo ratings yet

- Ukat2023 Taxation I: Topic 1: Scope & Basis of Malaysian TaxationDocument62 pagesUkat2023 Taxation I: Topic 1: Scope & Basis of Malaysian TaxationEileen WongNo ratings yet

- Adobe Scan Oct 11, 2023Document9 pagesAdobe Scan Oct 11, 2023Amir HamzaNo ratings yet

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- Inter GST Chart Book Nov2022Document41 pagesInter GST Chart Book Nov2022Aastha ChauhanNo ratings yet

- Income Tax - Income Tax Guide 2023, Latest NewsDocument34 pagesIncome Tax - Income Tax Guide 2023, Latest NewsnandiniNo ratings yet

- Taxation ProjectDocument70 pagesTaxation ProjectMantsha SayyedNo ratings yet

- Business PlanDocument14 pagesBusiness PlanghadaNo ratings yet

- GST Charts by CA Deep Jain SirDocument41 pagesGST Charts by CA Deep Jain SirVINAY SHARMANo ratings yet

- PWC Vietnam PTB 2020 enDocument60 pagesPWC Vietnam PTB 2020 enaNo ratings yet

- WorkDocument8 pagesWorkGuerrero MetrashNo ratings yet

- Intouch Issue 3 2022Document21 pagesIntouch Issue 3 2022Shermadurai VNo ratings yet

- Taxation-Reforms PRESENTATIONDocument17 pagesTaxation-Reforms PRESENTATIONRaman KumarNo ratings yet

- Indirect TaxDocument14 pagesIndirect TaxAzulfa Sultan.No ratings yet

- GTU Tax UpdatesDocument30 pagesGTU Tax UpdatesNelson StarkNo ratings yet

- Laws and Practices of Income TaxDocument34 pagesLaws and Practices of Income TaxNibir RahmanNo ratings yet

- GST Notes Semester 6Document39 pagesGST Notes Semester 6Bhanu DangNo ratings yet

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- Tax Memorandum 2012 FinalDocument58 pagesTax Memorandum 2012 FinalAzka KhalidNo ratings yet

- PWC Vietnam PTB 2020 enDocument60 pagesPWC Vietnam PTB 2020 enngoba_cuongNo ratings yet

- Countries Enter Into Double Taxation TreatiesDocument1 pageCountries Enter Into Double Taxation TreatiesavsharikaNo ratings yet

- Flash NewsDocument3 pagesFlash Newslingesh1892No ratings yet

- 74822bos60500 cp13Document48 pages74822bos60500 cp13Looney ApacheNo ratings yet

- Goods and Services Tax - 2021Document43 pagesGoods and Services Tax - 2021gsvighneshnairNo ratings yet

- FOURTH SEMESTER GSTDocument6 pagesFOURTH SEMESTER GSTKenny PhilipsNo ratings yet

- CITN On Taxes Oil & GasDocument91 pagesCITN On Taxes Oil & GasEfosaUwaifoNo ratings yet

- Chapter 1 Overview of Malaysian Tax SystemDocument11 pagesChapter 1 Overview of Malaysian Tax SystemLOO YU HUANGNo ratings yet

- By Damodar Agrawal & Associates: Damodar06@yahoo - Co.inDocument374 pagesBy Damodar Agrawal & Associates: Damodar06@yahoo - Co.inNiteshNo ratings yet

- EY Tax Alert - Finance ActDocument8 pagesEY Tax Alert - Finance ActMarie Thomas AllenNo ratings yet

- PWC Vietnam Pocket Tax Book 2019 enDocument64 pagesPWC Vietnam Pocket Tax Book 2019 enBudsakorn SuwaphanwattanaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- GST NotesDocument156 pagesGST NotesNishthaNo ratings yet

- Mepco Online BillDocument1 pageMepco Online Billdes121dtNo ratings yet

- Research Paper On Tax System in PakistanDocument6 pagesResearch Paper On Tax System in Pakistanafeavbrpd100% (2)

- VILGST - SGST - High Court Cases - 2023-VIL-360-CALDocument6 pagesVILGST - SGST - High Court Cases - 2023-VIL-360-CALBhanuprakash GuptaNo ratings yet

- Ca Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTDocument7 pagesCa Suraj Satija Ssguru GST Amendment: Introduction To GST Charge of GSTkinnar2013No ratings yet

- Economic Survey 2018 Vol 1Document137 pagesEconomic Survey 2018 Vol 1bhargavNo ratings yet

- Idt Vol-1 May Nov 2021 Exam PDFDocument616 pagesIdt Vol-1 May Nov 2021 Exam PDFSri Pavan100% (1)

- GST Working May 2022Document20 pagesGST Working May 2022Chandrashekar BNo ratings yet

- Resume Harun RashidDocument2 pagesResume Harun RashidHARUN RASHIDNo ratings yet

- Application Form: Gurgaon Greens, Sector 102, GurugramDocument16 pagesApplication Form: Gurgaon Greens, Sector 102, GurugramsumitNo ratings yet

- Tnvat Form WW Fy 15-16Document30 pagesTnvat Form WW Fy 15-16samaadhuNo ratings yet

- List of Topics GST - IDocument7 pagesList of Topics GST - IArnav GargNo ratings yet

- Report ON Impact of GST On Logistics Industry in India Project Report Submitted in Partial Fulfillment For The Award of Degree ofDocument31 pagesReport ON Impact of GST On Logistics Industry in India Project Report Submitted in Partial Fulfillment For The Award of Degree ofakshara pradeepNo ratings yet

- DL018 Dharmaj Zee24K May 23-24Document1 pageDL018 Dharmaj Zee24K May 23-24onlyhitmanNo ratings yet

- Chapter 3 Charge Under GSTDocument10 pagesChapter 3 Charge Under GSTabhay javiyaNo ratings yet

- Impact of GST On E-CommerceDocument4 pagesImpact of GST On E-CommerceIJAERS JOURNALNo ratings yet

- Residence: Architectural Design ProposalDocument15 pagesResidence: Architectural Design ProposalAditi AgrawalNo ratings yet

- Goods and Service TaxDocument14 pagesGoods and Service TaxkejkarNo ratings yet

- Auto TestDocument3 pagesAuto TestMaree AlShehriNo ratings yet

- Draft - GO - 26 - 10 - 2017 - English - Final 2017 PDFDocument38 pagesDraft - GO - 26 - 10 - 2017 - English - Final 2017 PDFAnuj AroraNo ratings yet

- Chart of AccountDocument7 pagesChart of Accountacahalim1103No ratings yet

- GST Booklet KutchDocument34 pagesGST Booklet KutchBhavik MehtaNo ratings yet

- FoodnhotelDocument24 pagesFoodnhotelHoward TeowNo ratings yet

- LUT Cover LetterDocument2 pagesLUT Cover LetterJanhvi Kishori ThakkarNo ratings yet

- Skills Assessment Fees For Professional Occupations - VETASSESSDocument12 pagesSkills Assessment Fees For Professional Occupations - VETASSESSjeff665547No ratings yet

- Adobe Scan 26 Apr 2023Document2 pagesAdobe Scan 26 Apr 2023Shranish KarNo ratings yet

- Palkesh Asawa - S Answer To How Is GST Beneficial For The Country - How Would It Help To Improve The Country - S Economy - QuoraDocument3 pagesPalkesh Asawa - S Answer To How Is GST Beneficial For The Country - How Would It Help To Improve The Country - S Economy - QuoraAshit AgarwalNo ratings yet

- ReceiptDocument2 pagesReceiptshaikh rehmanNo ratings yet

- CA Final Vsi Jaipur IDT ABC Analysis For Nov 2023Document4 pagesCA Final Vsi Jaipur IDT ABC Analysis For Nov 2023Dharani SsNo ratings yet