Download as pptx, pdf, or txt

You might also like

- Gold Business Account 82Document1 pageGold Business Account 82nicole.philippsNo ratings yet

- Nelnet Statement GuideDocument2 pagesNelnet Statement Guideetrye77No ratings yet

- Financial Analysis For Selected NBFCDocument51 pagesFinancial Analysis For Selected NBFCAnil Makvana85% (13)

- Shriram Finace Sip ReportDocument64 pagesShriram Finace Sip Reportshiv khillari75% (4)

- A Project Report OnDocument109 pagesA Project Report Onpiyu211sarawagigmail50% (2)

- BNK 211 Banking Law: by Ghana Shyam ShresthaDocument10 pagesBNK 211 Banking Law: by Ghana Shyam ShresthaghanaNo ratings yet

- Nageen Gul REG. NO. MBAR191006 Business Finance Submitted To: Ma'Am Rabia Habib Assignment No. 2 Long Term Financing in PakistanDocument8 pagesNageen Gul REG. NO. MBAR191006 Business Finance Submitted To: Ma'Am Rabia Habib Assignment No. 2 Long Term Financing in PakistanKainatNo ratings yet

- Banking Law & Regulation (BBA 8th Sem) PDFDocument115 pagesBanking Law & Regulation (BBA 8th Sem) PDFsuresh pathakNo ratings yet

- 1.2. Types of Bank: Dhruba Koirala National Law CollegeDocument38 pages1.2. Types of Bank: Dhruba Koirala National Law CollegeMadan ShresthaNo ratings yet

- Banking OmbudsmanDocument66 pagesBanking Ombudsmanmrchavan143No ratings yet

- Blackbook FinalDocument86 pagesBlackbook Finalgunesh somayaNo ratings yet

- NBFC and Its Registration ProcessDocument3 pagesNBFC and Its Registration ProcessShubhamNo ratings yet

- Micro-Finance Micro Finance Institutions: Session-7Document23 pagesMicro-Finance Micro Finance Institutions: Session-7Ayush SrivastavaNo ratings yet

- Banking Financial Services Management - Unit 1: Overview of Indian Banking SystemDocument64 pagesBanking Financial Services Management - Unit 1: Overview of Indian Banking SystemtkashvinNo ratings yet

- DTMFI Operational Guidelines - Draft For CommentsDocument49 pagesDTMFI Operational Guidelines - Draft For CommentsselwynmadyaNo ratings yet

- Pf-2-Term 5-BKFSDocument41 pagesPf-2-Term 5-BKFSAasif KhanNo ratings yet

- Banking Law PYQDocument11 pagesBanking Law PYQxakij19914No ratings yet

- Current Affairs: 01st March 2022 To 10th March 2022 CADocument84 pagesCurrent Affairs: 01st March 2022 To 10th March 2022 CAShubhendu VermaNo ratings yet

- BAFIADocument11 pagesBAFIAsuman nepalNo ratings yet

- Analysis of Role of Reserve Bank of India and The Banking Sector in IndiaDocument13 pagesAnalysis of Role of Reserve Bank of India and The Banking Sector in IndiaAnkit BohraNo ratings yet

- Banking and Insurance - 2 MARKSDocument13 pagesBanking and Insurance - 2 MARKSkirandegol18No ratings yet

- Main Objects of The BankDocument23 pagesMain Objects of The BankNishant GroverNo ratings yet

- Banking Notes 1) Define Banking?Document5 pagesBanking Notes 1) Define Banking?2067 SARAN.MNo ratings yet

- Group 7 Za BLKL MakalahDocument25 pagesGroup 7 Za BLKL MakalahAudrey ArivianaNo ratings yet

- Bank LicencingDocument28 pagesBank LicencingxyzNo ratings yet

- A Report On Trends in Banking & Retail BankingDocument5 pagesA Report On Trends in Banking & Retail BankingJyothi SahuNo ratings yet

- Module 2 2020Document87 pagesModule 2 2020Hariprasad bhatNo ratings yet

- BANKING: Corporate and Investment: Group 7Document18 pagesBANKING: Corporate and Investment: Group 7Sohraab SarinNo ratings yet

- Role of Banking System in IndiaDocument29 pagesRole of Banking System in IndiaarjunNo ratings yet

- MA0044Document8 pagesMA0044Tushar AhujaNo ratings yet

- Arrangement of Sections: National Housing Fund ActDocument11 pagesArrangement of Sections: National Housing Fund ActJoseph JosefNo ratings yet

- Financial Services & Institutions - An IntroductionDocument11 pagesFinancial Services & Institutions - An IntroductionMayank KumarNo ratings yet

- 'CC (CCC" CCC CCCCCCDocument14 pages'CC (CCC" CCC CCCCCCGopi KrishnaNo ratings yet

- Chap 3 Programs and PoliciesDocument5 pagesChap 3 Programs and PoliciesJenalyn floresNo ratings yet

- Unit II Registration of Bank and Insurance CompaniesDocument35 pagesUnit II Registration of Bank and Insurance CompaniesgenazvaliNo ratings yet

- Module 6 - NBFCDocument31 pagesModule 6 - NBFCSonali JagathNo ratings yet

- Chap 3 PPEDevtDocument5 pagesChap 3 PPEDevtJenalyn floresNo ratings yet

- LMS 5Document13 pagesLMS 5prabakar1No ratings yet

- Para Banking Services With Reference To HDFC BankDocument90 pagesPara Banking Services With Reference To HDFC Bankcharu100% (1)

- Operational Guidelines For NBFCsDocument34 pagesOperational Guidelines For NBFCssakshigulati2508No ratings yet

- SR - No Table of Content NODocument53 pagesSR - No Table of Content NONeha AhireNo ratings yet

- Axis Bank Ltd. Policy For Lending To Micro Small & Medium Enterprises (Msmes)Document5 pagesAxis Bank Ltd. Policy For Lending To Micro Small & Medium Enterprises (Msmes)hiteshmohakar15No ratings yet

- Chapter-1: 1.1 Overview of The IndustryDocument47 pagesChapter-1: 1.1 Overview of The IndustryJasmine KaurNo ratings yet

- C MMM MMDocument8 pagesC MMM MMHaroon ArshadNo ratings yet

- Bank, Banking and Banking Regulations PresentationDocument7 pagesBank, Banking and Banking Regulations PresentationApekshaNo ratings yet

- Economics-1 BALLB-207 Non - Banking Financial Institutions: Ms. Lavi VatsDocument15 pagesEconomics-1 BALLB-207 Non - Banking Financial Institutions: Ms. Lavi VatsjinNo ratings yet

- Introduction of Banking Industry - Draft 1Document1 pageIntroduction of Banking Industry - Draft 1Rajdeep RoyNo ratings yet

- What Are The Objectives & Achievements of Bank Nationalization in India?Document32 pagesWhat Are The Objectives & Achievements of Bank Nationalization in India?rakesh4888No ratings yet

- The Micro Finance Institutions (Development and Regulation) Bill, 2011 A BillDocument36 pagesThe Micro Finance Institutions (Development and Regulation) Bill, 2011 A BillMandeep Kaur KhalsaNo ratings yet

- Industry Profile: Non Banking Financial CompaniesDocument77 pagesIndustry Profile: Non Banking Financial CompaniesIMAM JAVOORNo ratings yet

- Banking LawsDocument24 pagesBanking LawsPrankyJellyNo ratings yet

- Industry Analysis - Banking: SIBM BangaloreDocument20 pagesIndustry Analysis - Banking: SIBM BangaloreAshu ManuNo ratings yet

- Anjali - Banking Management - AssignmentDocument7 pagesAnjali - Banking Management - AssignmentAnjali PaneruNo ratings yet

- Banking-Law Notes11Document66 pagesBanking-Law Notes11BharatNo ratings yet

- 10 - Chapter 3Document41 pages10 - Chapter 3jitendra kumarNo ratings yet

- Meaning of Banking: 1. Central BanksDocument6 pagesMeaning of Banking: 1. Central BanksMuskanNo ratings yet

- C CCCCC CDocument2 pagesC CCCCC CVinubela BelaNo ratings yet

- Universal Banking in IndiaDocument60 pagesUniversal Banking in IndiaPratik GosaviNo ratings yet

- Housing Finance: Presented by Sulekha Beri I.D.NO .43847Document46 pagesHousing Finance: Presented by Sulekha Beri I.D.NO .43847mehakdadwalNo ratings yet

- Punjab & Maharashtra Co-Operative Bank LTD Invites Expression of Interest (Eoi)Document11 pagesPunjab & Maharashtra Co-Operative Bank LTD Invites Expression of Interest (Eoi)SimranNo ratings yet

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2021 Volume III: Digitalizing Microfinance in Bangladesh: Findings from the Baseline SurveyFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2021 Volume III: Digitalizing Microfinance in Bangladesh: Findings from the Baseline SurveyNo ratings yet

- Internship Report-181010036 (FIN)Document50 pagesInternship Report-181010036 (FIN)Immanuel MondolNo ratings yet

- Cash ManagementDocument11 pagesCash ManagementSurya Setipanol100% (1)

- FEB Internet BillDocument1 pageFEB Internet Billlabhesh797No ratings yet

- Union Bank: Personal BankingDocument3 pagesUnion Bank: Personal BankingBryan ParkerNo ratings yet

- Transcript of Charlie Rose's Interview With John J. MackDocument27 pagesTranscript of Charlie Rose's Interview With John J. MackDealBook100% (2)

- Banking and Money VocabularyDocument5 pagesBanking and Money VocabularygustavoragaNo ratings yet

- 03 Special Types of Customers of A Bank CasesDocument4 pages03 Special Types of Customers of A Bank CasesVikashKumarNo ratings yet

- Internship Affiliation Report On Bank AsiaDocument42 pagesInternship Affiliation Report On Bank AsiaJāfri Wāhid100% (1)

- Untitled DocumentDocument7 pagesUntitled Documentlilieth shayNo ratings yet

- My State Bank Terms and TariffDocument23 pagesMy State Bank Terms and Tariffkefiyalew BNo ratings yet

- BookDocument6 pagesBookj.sanchez2730No ratings yet

- Fee Structure 2021-22Document4 pagesFee Structure 2021-22harsh bhargavaNo ratings yet

- Internship Report On Credit Risk ManagemDocument78 pagesInternship Report On Credit Risk Managemmd shadab zaman RahatNo ratings yet

- Block 5Document123 pagesBlock 5Shreya PansariNo ratings yet

- Bank Statement For Ebesun Company (Nigeria) LTD, UBA 2021-2Document2 pagesBank Statement For Ebesun Company (Nigeria) LTD, UBA 2021-2Chidinma NnoliNo ratings yet

- Chapter 4 Balance Sheet CompleteDocument27 pagesChapter 4 Balance Sheet CompleteNael Nasir ChiraghNo ratings yet

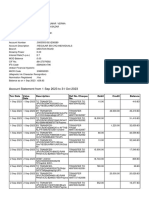

- Account Statement From 1 Sep 2023 To 31 Oct 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 1 Sep 2023 To 31 Oct 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceprnali.vflNo ratings yet

- An Overview of The Economic Causes and Effects of Dollarisation: Case of ZimbabweDocument5 pagesAn Overview of The Economic Causes and Effects of Dollarisation: Case of ZimbabweParth VijayNo ratings yet

- Comparative Analysis of The Performance of Selected Co-Operative Banks in Pune DistrictDocument34 pagesComparative Analysis of The Performance of Selected Co-Operative Banks in Pune DistrictMarshall CountyNo ratings yet

- Blackbook Project On Modernization in Banking System in India - 163418955Document81 pagesBlackbook Project On Modernization in Banking System in India - 163418955Varun ParekhNo ratings yet

- Kap 1 Workbook Se CH 9Document26 pagesKap 1 Workbook Se CH 9Zsadist20No ratings yet

- Rbi Ifsc Code ListDocument3 pagesRbi Ifsc Code Listramawatar agarwalNo ratings yet

- Statement 517000057 86377450 17 07 2023 17 09 2023Document6 pagesStatement 517000057 86377450 17 07 2023 17 09 2023katsergey12No ratings yet

- SWOT of Indian Banking SectorDocument10 pagesSWOT of Indian Banking SectorRashi AroraNo ratings yet

- ANUJADocument51 pagesANUJAThe Nepal ParadiseNo ratings yet

- Comparative Study of Financial Products (Casa) in Banking IndustryDocument17 pagesComparative Study of Financial Products (Casa) in Banking Industrypolakisagar0% (1)

- Money: Money Is Any Object That Is Generally Accepted As Payment For Goods and Services and Repayment ofDocument50 pagesMoney: Money Is Any Object That Is Generally Accepted As Payment For Goods and Services and Repayment ofChetan Ganesh RautNo ratings yet

- Credit Creation by Commercial Banks HandoutsDocument5 pagesCredit Creation by Commercial Banks HandoutsMahnoor AabidNo ratings yet