Download as ppt, pdf, or txt

You might also like

- Solution Manual For Foundations of Financial Management Block Hirt Danielsen 15th EditionDocument37 pagesSolution Manual For Foundations of Financial Management Block Hirt Danielsen 15th Editionabatisretroactl5z6100% (30)

- Fundamentals of Corporate Finance 9th Edition by Brealey Myers Marcus ISBN Solution ManualDocument35 pagesFundamentals of Corporate Finance 9th Edition by Brealey Myers Marcus ISBN Solution Manualmatthew100% (27)

- Day 1Document11 pagesDay 1Abdullah EjazNo ratings yet

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Corporate Financial Distress, Restructuring, and Bankruptcy: Analyze Leveraged Finance, Distressed Debt, and BankruptcyFrom EverandCorporate Financial Distress, Restructuring, and Bankruptcy: Analyze Leveraged Finance, Distressed Debt, and BankruptcyNo ratings yet

- WACC Case StudyDocument2 pagesWACC Case StudyMuhammad AdeelNo ratings yet

- Investments: Financial Accounting, Seventh EditionDocument39 pagesInvestments: Financial Accounting, Seventh EditionCaroline NguyenNo ratings yet

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument71 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeRizki NurwikanNo ratings yet

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument78 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeSiyedong Ardi100% (1)

- CH 12Document71 pagesCH 12Sahar YehiaNo ratings yet

- CH 16Document46 pagesCH 16Hasan AzmiNo ratings yet

- ch16, Accounting PrinciplesDocument47 pagesch16, Accounting PrinciplesH.R. Robin100% (1)

- Chapter 12 PowerPointDocument55 pagesChapter 12 PowerPointcheuleee100% (1)

- Statement of Cash Flows: Kimmel Weygandt Kieso Accounting, Sixth EditionDocument43 pagesStatement of Cash Flows: Kimmel Weygandt Kieso Accounting, Sixth EditionJoonasNo ratings yet

- Accounting Principles: Second Canadian EditionDocument25 pagesAccounting Principles: Second Canadian EditionEshetieNo ratings yet

- Reporting and Interpreting Investments in Other CorporationsDocument40 pagesReporting and Interpreting Investments in Other Corporationsfmj6687No ratings yet

- Accounting For LiabilitiesDocument58 pagesAccounting For LiabilitiesMizumi IshiharaNo ratings yet

- Ch13 InvestmentsDocument29 pagesCh13 InvestmentsJemal SeidNo ratings yet

- Chapter 3 InvestmentsDocument44 pagesChapter 3 Investmentssamuel hailuNo ratings yet

- AccoutingDocument22 pagesAccoutingmeisi anastasiaNo ratings yet

- BUS 120: Financial Accounting Chapter 13: Investments: Dr. Al TacconeDocument21 pagesBUS 120: Financial Accounting Chapter 13: Investments: Dr. Al TacconeSanjib PaulNo ratings yet

- Ceilli 2011Document242 pagesCeilli 2011Peter YowNo ratings yet

- Chapter 1 Introduction To FSADocument11 pagesChapter 1 Introduction To FSALuu Nhat MinhNo ratings yet

- Intermediate Accounting Solutions ch1Document62 pagesIntermediate Accounting Solutions ch1laminuNo ratings yet

- Accounting PrinciplesDocument25 pagesAccounting PrinciplesEshetieNo ratings yet

- Corporations: Organization, Share Transactions, Dividends, and Retained EarningsDocument32 pagesCorporations: Organization, Share Transactions, Dividends, and Retained EarningsSusanNo ratings yet

- Financial Management 2Document6 pagesFinancial Management 2Julie R. UgsodNo ratings yet

- 1 Session 2 - Cash, Receivables, PSAK 71Document84 pages1 Session 2 - Cash, Receivables, PSAK 71melva vionaNo ratings yet

- FA1 BPP Chapter 2 Assets, Liabilities & Accounting EquationDocument19 pagesFA1 BPP Chapter 2 Assets, Liabilities & Accounting EquationS RaihanNo ratings yet

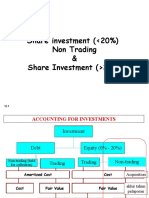

- 12.2 Share Investment Non Trading & Share Invesment Lebih 20%Document18 pages12.2 Share Investment Non Trading & Share Invesment Lebih 20%TIFFANNY SHELIANo ratings yet

- Ch02. Accounting EquationDocument22 pagesCh02. Accounting EquationHải TrầnNo ratings yet

- Chapter 16 1Document42 pagesChapter 16 1HEM CHEANo ratings yet

- ObligasiDocument118 pagesObligasifaizah aini100% (1)

- Ias 7Document33 pagesIas 7mohedNo ratings yet

- Financial Management Module 6Document17 pagesFinancial Management Module 6Armand Robles100% (1)

- Chapter 2 LectureDocument60 pagesChapter 2 LectureAlex Lau100% (1)

- 2 Understanding Financial Information-1Document32 pages2 Understanding Financial Information-1Tijana DjurdjevicNo ratings yet

- CH 13Document85 pagesCH 13Sahar YehiaNo ratings yet

- 12.1 Bond Investment & Share Investment TradingDocument19 pages12.1 Bond Investment & Share Investment TradingTIFFANNY SHELIANo ratings yet

- Equity: Learning ObjectivesDocument32 pagesEquity: Learning ObjectivesAASNo ratings yet

- The Recording Process - Bisnis A - B 2014Document52 pagesThe Recording Process - Bisnis A - B 2014Hansel AddisonNo ratings yet

- Wealth Managment 1Document73 pagesWealth Managment 1dashashutosh87No ratings yet

- Financial Statement AnalysisDocument82 pagesFinancial Statement AnalysisHeisen LukeNo ratings yet

- Chapter 6 - Financial Statement AnalysisDocument22 pagesChapter 6 - Financial Statement AnalysisRameinor TambuliNo ratings yet

- Tugas 13 InvestmentDocument6 pagesTugas 13 InvestmentLenrik AbcNo ratings yet

- Statement of Cash Flows: Learning ObjectivesDocument44 pagesStatement of Cash Flows: Learning ObjectivesMD. Barkat ullah BijoyNo ratings yet

- Laporan Arus KasDocument20 pagesLaporan Arus KasSyuhadakAl-FasuruniNo ratings yet

- CH 07Document104 pagesCH 07Brian CrisNo ratings yet

- CH 07Document103 pagesCH 07Amit SarkarNo ratings yet

- Topic 2 Financial Statements AnalysisDocument84 pagesTopic 2 Financial Statements AnalysisTommyYapNo ratings yet

- A Further Look at Financial StatementsDocument56 pagesA Further Look at Financial StatementsLê Thanh HàNo ratings yet

- ACC307 1 Material Unit 4Document58 pagesACC307 1 Material Unit 4Umaid FaisalNo ratings yet

- WorkbookDocument72 pagesWorkbookMbalenhle NdlovuNo ratings yet

- Rinconada - ProjectDocument29 pagesRinconada - ProjectRINCONADA ReynalynNo ratings yet

- CH 07Document104 pagesCH 07ranniaNo ratings yet

- ch07 - Intermediate Acc IFRS (Cash and Receivable)Document104 pagesch07 - Intermediate Acc IFRS (Cash and Receivable)irma cahyani kawiNo ratings yet

- CH 17Document121 pagesCH 17diva4khrist06100% (1)

- CH 17Document122 pagesCH 17SIMAD UniversityNo ratings yet

- Financial Accounting: The Recording ProcessDocument20 pagesFinancial Accounting: The Recording Processlilyc3105No ratings yet

- Financial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersFrom EverandFinancial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Yang Zhao Vita 0608Document4 pagesYang Zhao Vita 0608api-394139778No ratings yet

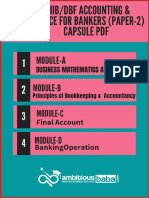

- JAIJAIIB Paper 2 CAPSULE PDF 2.O Accounting Finance For Bankers by Ambitious BabaDocument159 pagesJAIJAIIB Paper 2 CAPSULE PDF 2.O Accounting Finance For Bankers by Ambitious BabaSaurabhNo ratings yet

- Nptel AssignmentsDocument83 pagesNptel AssignmentsVaibhav ShahNo ratings yet

- Original Presentation by Hamza ShahDocument56 pagesOriginal Presentation by Hamza ShahHamza BukhariNo ratings yet

- CMA ExamDocument34 pagesCMA Examtimmy457No ratings yet

- Citibank India: Expatriate Indian Programme: Trailer (A Look at Philosophy)Document20 pagesCitibank India: Expatriate Indian Programme: Trailer (A Look at Philosophy)Vipul BhattNo ratings yet

- TCS BaNCS Research Journal Issue 3 0713 1Document52 pagesTCS BaNCS Research Journal Issue 3 0713 1Poovana Kokkalera PNo ratings yet

- Facing InterviewDocument358 pagesFacing InterviewPramod Kumar SrivastavaNo ratings yet

- The Impact of Financial Literacy On Budgeting Management Among Abm StudentsDocument12 pagesThe Impact of Financial Literacy On Budgeting Management Among Abm StudentsDatu Abdullah Sangki MpsNo ratings yet

- CFA Level III Mock Exam 4 - Questions (PM)Document34 pagesCFA Level III Mock Exam 4 - Questions (PM)Munkhbaatar SanjaasurenNo ratings yet

- QFR 03-March 2022 LDocument70 pagesQFR 03-March 2022 LNapolean DynamiteNo ratings yet

- FIZZ 2001 Annual - ReportDocument38 pagesFIZZ 2001 Annual - ReportSteveMastersNo ratings yet

- Chapter 16 Managing Bond Portfolios: Multiple Choice QuestionsDocument29 pagesChapter 16 Managing Bond Portfolios: Multiple Choice Questionsleam37No ratings yet

- Uppsala Papers in Economic History: 1993 Working Paper No 10Document40 pagesUppsala Papers in Economic History: 1993 Working Paper No 10Michalis RizosNo ratings yet

- Understanding CVA FVA XVADocument21 pagesUnderstanding CVA FVA XVAparora2No ratings yet

- Brunswick County Feasibility Report-2nd Draft 9-16-19Document48 pagesBrunswick County Feasibility Report-2nd Draft 9-16-19Johanna Ferebee StillNo ratings yet

- Debentures and BondsDocument3 pagesDebentures and Bondsremruata rascalralteNo ratings yet

- Final Output Chapter 25-26Document27 pagesFinal Output Chapter 25-26Syrell Nabor100% (4)

- Aud Prob Part 1Document106 pagesAud Prob Part 1Ma. Hazel Donita DiazNo ratings yet

- Financial Markets and Institutions: Ninth Edition, Global EditionDocument34 pagesFinancial Markets and Institutions: Ninth Edition, Global Editiondara moralezNo ratings yet

- Lcture 3 and 4 Risk and ReturnDocument8 pagesLcture 3 and 4 Risk and Returnmuhammad hasanNo ratings yet

- Sources of FinanceDocument16 pagesSources of FinanceVinay CHNo ratings yet

- File Annual 5e1598221bf66Document118 pagesFile Annual 5e1598221bf66Mayang Siti MasyitohNo ratings yet

- Auditing Problem Final Exam With Answer Only, No SolutionDocument23 pagesAuditing Problem Final Exam With Answer Only, No SolutionRheu Reyes100% (1)

- Saunders 8e PPT Chapter05Document33 pagesSaunders 8e PPT Chapter05sdgdfs sdfsfNo ratings yet

- GSIS vs. CA DigestDocument1 pageGSIS vs. CA DigestCaitlin Kintanar100% (1)

- Solved Problems in Engineering Economy & AccountingDocument10 pagesSolved Problems in Engineering Economy & AccountingMiko F. Rodriguez0% (2)

- Capital MarketDocument106 pagesCapital MarketJayar DimaculanganNo ratings yet