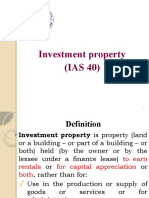

MFRS 140 Investment Property

MFRS 140 Investment Property

You might also like

- Eco AssignmentDocument9 pagesEco AssignmentCIAO TRAVELNo ratings yet

- Walmart Around The WorldDocument7 pagesWalmart Around The WorldSuraj KumarNo ratings yet

- Investment PropertyDocument26 pagesInvestment PropertyLovemore ChigwandaNo ratings yet

- FARAP-4406C: Investment Property & Other InvestmentsDocument10 pagesFARAP-4406C: Investment Property & Other InvestmentsLei PangilinanNo ratings yet

- 06C Investment Property & Other InvestmentsDocument8 pages06C Investment Property & Other Investmentsrandomlungs121223No ratings yet

- Module 5 Investment PropertyDocument16 pagesModule 5 Investment PropertyJenilyn CalaraNo ratings yet

- Summary NAS 40Document6 pagesSummary NAS 40sitoulamanish100No ratings yet

- Ias 40 - Investment PropertyDocument4 pagesIas 40 - Investment PropertyTope JohnNo ratings yet

- 01 RESA FAR 4210 Investment Property Other Fund Investments PDFDocument5 pages01 RESA FAR 4210 Investment Property Other Fund Investments PDFby ScribdNo ratings yet

- Investment Property: By:-Yohannes Negatu (Acca, DipifrDocument31 pagesInvestment Property: By:-Yohannes Negatu (Acca, DipifrEshetie Mekonene AmareNo ratings yet

- Investment Property: By:-Yohannes Negatu (Acca, DipifrDocument31 pagesInvestment Property: By:-Yohannes Negatu (Acca, DipifrEshetie Mekonene AmareNo ratings yet

- IA2.102 Investment PropertyDocument10 pagesIA2.102 Investment PropertyPaul BandolaNo ratings yet

- Ias 40 Investment Property by A Deel SaleemDocument12 pagesIas 40 Investment Property by A Deel SaleemFalah Ud Din Sheryar100% (1)

- Topic 1 Part 5 Impairment of Investment PropertyDocument10 pagesTopic 1 Part 5 Impairment of Investment Propertynaufal hazimNo ratings yet

- FAR 4310 Investment Property Other Fund InvestmentsDocument5 pagesFAR 4310 Investment Property Other Fund InvestmentsATHALIAH LUNA MERCADEJASNo ratings yet

- FAR-4210 Investment Property & Other Fund Investments: - T R S A ResaDocument4 pagesFAR-4210 Investment Property & Other Fund Investments: - T R S A ResaEllyssa Ann MorenoNo ratings yet

- Investment Property: Investment Property - Is Land And/or Building Held To Earn Rentals or Capital Appreciation or BothDocument9 pagesInvestment Property: Investment Property - Is Land And/or Building Held To Earn Rentals or Capital Appreciation or BothJustine Verallo100% (1)

- Chapter 2 Izan - MFRS140 - IP 2Document41 pagesChapter 2 Izan - MFRS140 - IP 2MUHAMMAD AMIR HAMZAH NURZAFILNo ratings yet

- 21 - Investment PropertyDocument7 pages21 - Investment PropertyYudna YuNo ratings yet

- Ias-40 - Investment PropertyDocument16 pagesIas-40 - Investment PropertyPue Das100% (2)

- Pas 40 Investment PropertyDocument6 pagesPas 40 Investment PropertyElaiza Jane CruzNo ratings yet

- #16 Investment PropertyDocument4 pages#16 Investment PropertyClaudine DuhapaNo ratings yet

- 6902 PPT Materials For UploadDocument13 pages6902 PPT Materials For UploadAljur SalamedaNo ratings yet

- Investment Property Is Defined As Property (Land and Building of Part of A Building or Both) HeldDocument11 pagesInvestment Property Is Defined As Property (Land and Building of Part of A Building or Both) HeldRNo ratings yet

- Investment Property InventoriesDocument11 pagesInvestment Property InventorieshemantbaidNo ratings yet

- KM Investment PropertyDocument4 pagesKM Investment Propertynikhilmandlecha6142No ratings yet

- IFA I, Chapter 6Document29 pagesIFA I, Chapter 6kqk07829No ratings yet

- I. Objective: Property Held Under An Operating LeaseDocument5 pagesI. Objective: Property Held Under An Operating Leasemusic niNo ratings yet

- Chapter 9 Investment PropertyDocument4 pagesChapter 9 Investment Propertymaria isabellaNo ratings yet

- PAS 40investment PropertyDocument3 pagesPAS 40investment PropertyJoshua Kadatar Chinalpan IINo ratings yet

- IAS 40 Investment Property (S)Document16 pagesIAS 40 Investment Property (S)Given RefilweNo ratings yet

- Chapter 22 - Investment Property and Cash Surrender Value PDFDocument16 pagesChapter 22 - Investment Property and Cash Surrender Value PDFTurksNo ratings yet

- Investment Property NotesDocument2 pagesInvestment Property NotesGian CalaNo ratings yet

- Investment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldDocument7 pagesInvestment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldMark Anthony SivaNo ratings yet

- BORROWING COSTS-WPS OfficeDocument4 pagesBORROWING COSTS-WPS OfficeagentnicNo ratings yet

- Module 2 Investment Property and FundsDocument6 pagesModule 2 Investment Property and FundsCharice Anne VillamarinNo ratings yet

- Section 16Document20 pagesSection 16Abata BageyuNo ratings yet

- Investment PropertyDocument10 pagesInvestment PropertyPrudentNo ratings yet

- Investment Property: DefinitionsDocument17 pagesInvestment Property: Definitionssamit shresthaNo ratings yet

- IAS 40 Investment PropertyDocument12 pagesIAS 40 Investment PropertyIrfan AhmedNo ratings yet

- Investment PropertyDocument23 pagesInvestment PropertyErica AcunaNo ratings yet

- CFAS PAS 40 Q and ADocument2 pagesCFAS PAS 40 Q and AJoseph Andrei BunadoNo ratings yet

- Investment PropertyDocument8 pagesInvestment PropertyNoella Marie BaronNo ratings yet

- Week 07 - 01 - Module 016 - Accounting For InventoriesDocument9 pagesWeek 07 - 01 - Module 016 - Accounting For Inventories지마리No ratings yet

- Department of Accountancy: Holy Angel University Intermediate Accounting 1Document22 pagesDepartment of Accountancy: Holy Angel University Intermediate Accounting 1Krisha G.100% (1)

- PAS 40, 41 and 37Document10 pagesPAS 40, 41 and 37Olive Jean TiuNo ratings yet

- FAR - Investment Property - StudentDocument3 pagesFAR - Investment Property - StudentEdel Kristen BarcarseNo ratings yet

- Module 15 PAS 40Document5 pagesModule 15 PAS 40Jan JanNo ratings yet

- Chapter 4 Investment PropertiesDocument2 pagesChapter 4 Investment PropertiesHui XianNo ratings yet

- Pas 40Document2 pagesPas 40Beverly UrbaseNo ratings yet

- 07 Investment PropertyDocument3 pages07 Investment PropertyPat RFNo ratings yet

- Pas 40 Investment PropertyDocument4 pagesPas 40 Investment PropertykristineNo ratings yet

- SMEs For Investment PropertyDocument23 pagesSMEs For Investment PropertyGleah Rose Bulaquiña LimNo ratings yet

- Lecture Notes - IAS 40Document5 pagesLecture Notes - IAS 40Muhammed NaqiNo ratings yet

- B2 &C1 Ias 40 Investment PropertyDocument32 pagesB2 &C1 Ias 40 Investment Propertyabuumgweno1803No ratings yet

- Investment PropertyDocument16 pagesInvestment PropertyTsegay ArayaNo ratings yet

- 161 16 PAS 40 Investment PropertyDocument4 pages161 16 PAS 40 Investment PropertyRegina Gregoria SalasNo ratings yet

- Intacc Ass 3Document2 pagesIntacc Ass 3Pixie CanaveralNo ratings yet

- Chapter 2 - Investment Property (MFRS 140)Document35 pagesChapter 2 - Investment Property (MFRS 140)SITI NUR WARDINA WAFI ROMLINo ratings yet

- Corporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDocument12 pagesCorporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDev ShahNo ratings yet

- Securitized Real Estate and 1031 ExchangesFrom EverandSecuritized Real Estate and 1031 ExchangesNo ratings yet

- World Footwear Business Conditions Survey: 2 SemesterDocument14 pagesWorld Footwear Business Conditions Survey: 2 SemesterYasir NasimNo ratings yet

- Choice of WordsDocument101 pagesChoice of WordsLê Thanh Ngần Trường THPT Phương SơnNo ratings yet

- Descriptive SituationsDocument9 pagesDescriptive SituationsRiya PandeyNo ratings yet

- The Intelligent Investor Chapter 9Document3 pagesThe Intelligent Investor Chapter 9Michael Pullman100% (1)

- Small Scale Organic Rankine Cycle (ORC) A Techno-Economic ReviewDocument26 pagesSmall Scale Organic Rankine Cycle (ORC) A Techno-Economic ReviewJoao MinhoNo ratings yet

- giBriL's System ManualDocument1 pagegiBriL's System Manualhacker fxNo ratings yet

- PaymentDocument1 pagePaymentM SotanNo ratings yet

- The Utility Function and Indifference CurvesDocument1 pageThe Utility Function and Indifference CurvescaptivatingmukNo ratings yet

- History of Commerce NotesDocument3 pagesHistory of Commerce NotesMatthew John PaceNo ratings yet

- Principles of MarketingDocument9 pagesPrinciples of MarketingNazrinaazAhmadNo ratings yet

- Government Finance Statistics (GFSX) : Valuation of TransactionsDocument2 pagesGovernment Finance Statistics (GFSX) : Valuation of TransactionsKhenneth BalcetaNo ratings yet

- Thrift by Smiles, Samuel, 1812-1904Document224 pagesThrift by Smiles, Samuel, 1812-1904Gutenberg.orgNo ratings yet

- Manacc Online QuizDocument3 pagesManacc Online QuizJoshuaTagayunaNo ratings yet

- Week 11 Tutorial SolutionsDocument6 pagesWeek 11 Tutorial SolutionsMiss SlayerNo ratings yet

- 7 THDocument2 pages7 THUsama AhmedNo ratings yet

- Lab 1Document5 pagesLab 1Nguyen Phung Thinh K17 HLNo ratings yet

- Economics I 1005Document23 pagesEconomics I 1005meetwithsanjay100% (1)

- Bureau of Local Government Finance Opinion: Mr. Genestor E. CruzDocument3 pagesBureau of Local Government Finance Opinion: Mr. Genestor E. CruzNash Ortiz LuisNo ratings yet

- Syllabus Grouping of Subjects and Scheme of ExaminationDocument29 pagesSyllabus Grouping of Subjects and Scheme of ExaminationAbhisek AgrawalNo ratings yet

- Formulae and Discount Tables: Professional Level Examination Financial ManagementDocument2 pagesFormulae and Discount Tables: Professional Level Examination Financial ManagementClaudine CjNo ratings yet

- Grace Hesketh Is The Owner of An Extremely Successful DressDocument2 pagesGrace Hesketh Is The Owner of An Extremely Successful DressAmit PandeyNo ratings yet

- Cost Sheet 1Document6 pagesCost Sheet 1Tamilselvi ANo ratings yet

- Republic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Document24 pagesRepublic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Johayra AbbasNo ratings yet

- Global Oil and Gas IndustryDocument23 pagesGlobal Oil and Gas IndustryYash Agarwal100% (1)

- Estimates OF State Domestic Product, Odisha: (Both at Basic Prices and Market Prices)Document24 pagesEstimates OF State Domestic Product, Odisha: (Both at Basic Prices and Market Prices)naina saxenaNo ratings yet

- AUDI in ChinaDocument11 pagesAUDI in ChinaSen PrashantNo ratings yet

- Supply Takeout Data PDFDocument1 pageSupply Takeout Data PDFActive88No ratings yet

- Final Exam Set A MafDocument6 pagesFinal Exam Set A MafZeyad Tareq Al SaroriNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Eco AssignmentDocument9 pagesEco AssignmentCIAO TRAVELNo ratings yet

- Walmart Around The WorldDocument7 pagesWalmart Around The WorldSuraj KumarNo ratings yet

- Investment PropertyDocument26 pagesInvestment PropertyLovemore ChigwandaNo ratings yet

- FARAP-4406C: Investment Property & Other InvestmentsDocument10 pagesFARAP-4406C: Investment Property & Other InvestmentsLei PangilinanNo ratings yet

- 06C Investment Property & Other InvestmentsDocument8 pages06C Investment Property & Other Investmentsrandomlungs121223No ratings yet

- Module 5 Investment PropertyDocument16 pagesModule 5 Investment PropertyJenilyn CalaraNo ratings yet

- Summary NAS 40Document6 pagesSummary NAS 40sitoulamanish100No ratings yet

- Ias 40 - Investment PropertyDocument4 pagesIas 40 - Investment PropertyTope JohnNo ratings yet

- 01 RESA FAR 4210 Investment Property Other Fund Investments PDFDocument5 pages01 RESA FAR 4210 Investment Property Other Fund Investments PDFby ScribdNo ratings yet

- Investment Property: By:-Yohannes Negatu (Acca, DipifrDocument31 pagesInvestment Property: By:-Yohannes Negatu (Acca, DipifrEshetie Mekonene AmareNo ratings yet

- Investment Property: By:-Yohannes Negatu (Acca, DipifrDocument31 pagesInvestment Property: By:-Yohannes Negatu (Acca, DipifrEshetie Mekonene AmareNo ratings yet

- IA2.102 Investment PropertyDocument10 pagesIA2.102 Investment PropertyPaul BandolaNo ratings yet

- Ias 40 Investment Property by A Deel SaleemDocument12 pagesIas 40 Investment Property by A Deel SaleemFalah Ud Din Sheryar100% (1)

- Topic 1 Part 5 Impairment of Investment PropertyDocument10 pagesTopic 1 Part 5 Impairment of Investment Propertynaufal hazimNo ratings yet

- FAR 4310 Investment Property Other Fund InvestmentsDocument5 pagesFAR 4310 Investment Property Other Fund InvestmentsATHALIAH LUNA MERCADEJASNo ratings yet

- FAR-4210 Investment Property & Other Fund Investments: - T R S A ResaDocument4 pagesFAR-4210 Investment Property & Other Fund Investments: - T R S A ResaEllyssa Ann MorenoNo ratings yet

- Investment Property: Investment Property - Is Land And/or Building Held To Earn Rentals or Capital Appreciation or BothDocument9 pagesInvestment Property: Investment Property - Is Land And/or Building Held To Earn Rentals or Capital Appreciation or BothJustine Verallo100% (1)

- Chapter 2 Izan - MFRS140 - IP 2Document41 pagesChapter 2 Izan - MFRS140 - IP 2MUHAMMAD AMIR HAMZAH NURZAFILNo ratings yet

- 21 - Investment PropertyDocument7 pages21 - Investment PropertyYudna YuNo ratings yet

- Ias-40 - Investment PropertyDocument16 pagesIas-40 - Investment PropertyPue Das100% (2)

- Pas 40 Investment PropertyDocument6 pagesPas 40 Investment PropertyElaiza Jane CruzNo ratings yet

- #16 Investment PropertyDocument4 pages#16 Investment PropertyClaudine DuhapaNo ratings yet

- 6902 PPT Materials For UploadDocument13 pages6902 PPT Materials For UploadAljur SalamedaNo ratings yet

- Investment Property Is Defined As Property (Land and Building of Part of A Building or Both) HeldDocument11 pagesInvestment Property Is Defined As Property (Land and Building of Part of A Building or Both) HeldRNo ratings yet

- Investment Property InventoriesDocument11 pagesInvestment Property InventorieshemantbaidNo ratings yet

- KM Investment PropertyDocument4 pagesKM Investment Propertynikhilmandlecha6142No ratings yet

- IFA I, Chapter 6Document29 pagesIFA I, Chapter 6kqk07829No ratings yet

- I. Objective: Property Held Under An Operating LeaseDocument5 pagesI. Objective: Property Held Under An Operating Leasemusic niNo ratings yet

- Chapter 9 Investment PropertyDocument4 pagesChapter 9 Investment Propertymaria isabellaNo ratings yet

- PAS 40investment PropertyDocument3 pagesPAS 40investment PropertyJoshua Kadatar Chinalpan IINo ratings yet

- IAS 40 Investment Property (S)Document16 pagesIAS 40 Investment Property (S)Given RefilweNo ratings yet

- Chapter 22 - Investment Property and Cash Surrender Value PDFDocument16 pagesChapter 22 - Investment Property and Cash Surrender Value PDFTurksNo ratings yet

- Investment Property NotesDocument2 pagesInvestment Property NotesGian CalaNo ratings yet

- Investment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldDocument7 pagesInvestment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldMark Anthony SivaNo ratings yet

- BORROWING COSTS-WPS OfficeDocument4 pagesBORROWING COSTS-WPS OfficeagentnicNo ratings yet

- Module 2 Investment Property and FundsDocument6 pagesModule 2 Investment Property and FundsCharice Anne VillamarinNo ratings yet

- Section 16Document20 pagesSection 16Abata BageyuNo ratings yet

- Investment PropertyDocument10 pagesInvestment PropertyPrudentNo ratings yet

- Investment Property: DefinitionsDocument17 pagesInvestment Property: Definitionssamit shresthaNo ratings yet

- IAS 40 Investment PropertyDocument12 pagesIAS 40 Investment PropertyIrfan AhmedNo ratings yet

- Investment PropertyDocument23 pagesInvestment PropertyErica AcunaNo ratings yet

- CFAS PAS 40 Q and ADocument2 pagesCFAS PAS 40 Q and AJoseph Andrei BunadoNo ratings yet

- Investment PropertyDocument8 pagesInvestment PropertyNoella Marie BaronNo ratings yet

- Week 07 - 01 - Module 016 - Accounting For InventoriesDocument9 pagesWeek 07 - 01 - Module 016 - Accounting For Inventories지마리No ratings yet

- Department of Accountancy: Holy Angel University Intermediate Accounting 1Document22 pagesDepartment of Accountancy: Holy Angel University Intermediate Accounting 1Krisha G.100% (1)

- PAS 40, 41 and 37Document10 pagesPAS 40, 41 and 37Olive Jean TiuNo ratings yet

- FAR - Investment Property - StudentDocument3 pagesFAR - Investment Property - StudentEdel Kristen BarcarseNo ratings yet

- Module 15 PAS 40Document5 pagesModule 15 PAS 40Jan JanNo ratings yet

- Chapter 4 Investment PropertiesDocument2 pagesChapter 4 Investment PropertiesHui XianNo ratings yet

- Pas 40Document2 pagesPas 40Beverly UrbaseNo ratings yet

- 07 Investment PropertyDocument3 pages07 Investment PropertyPat RFNo ratings yet

- Pas 40 Investment PropertyDocument4 pagesPas 40 Investment PropertykristineNo ratings yet

- SMEs For Investment PropertyDocument23 pagesSMEs For Investment PropertyGleah Rose Bulaquiña LimNo ratings yet

- Lecture Notes - IAS 40Document5 pagesLecture Notes - IAS 40Muhammed NaqiNo ratings yet

- B2 &C1 Ias 40 Investment PropertyDocument32 pagesB2 &C1 Ias 40 Investment Propertyabuumgweno1803No ratings yet

- Investment PropertyDocument16 pagesInvestment PropertyTsegay ArayaNo ratings yet

- 161 16 PAS 40 Investment PropertyDocument4 pages161 16 PAS 40 Investment PropertyRegina Gregoria SalasNo ratings yet

- Intacc Ass 3Document2 pagesIntacc Ass 3Pixie CanaveralNo ratings yet

- Chapter 2 - Investment Property (MFRS 140)Document35 pagesChapter 2 - Investment Property (MFRS 140)SITI NUR WARDINA WAFI ROMLINo ratings yet

- Corporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDocument12 pagesCorporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDev ShahNo ratings yet

- Securitized Real Estate and 1031 ExchangesFrom EverandSecuritized Real Estate and 1031 ExchangesNo ratings yet

- World Footwear Business Conditions Survey: 2 SemesterDocument14 pagesWorld Footwear Business Conditions Survey: 2 SemesterYasir NasimNo ratings yet

- Choice of WordsDocument101 pagesChoice of WordsLê Thanh Ngần Trường THPT Phương SơnNo ratings yet

- Descriptive SituationsDocument9 pagesDescriptive SituationsRiya PandeyNo ratings yet

- The Intelligent Investor Chapter 9Document3 pagesThe Intelligent Investor Chapter 9Michael Pullman100% (1)

- Small Scale Organic Rankine Cycle (ORC) A Techno-Economic ReviewDocument26 pagesSmall Scale Organic Rankine Cycle (ORC) A Techno-Economic ReviewJoao MinhoNo ratings yet

- giBriL's System ManualDocument1 pagegiBriL's System Manualhacker fxNo ratings yet

- PaymentDocument1 pagePaymentM SotanNo ratings yet

- The Utility Function and Indifference CurvesDocument1 pageThe Utility Function and Indifference CurvescaptivatingmukNo ratings yet

- History of Commerce NotesDocument3 pagesHistory of Commerce NotesMatthew John PaceNo ratings yet

- Principles of MarketingDocument9 pagesPrinciples of MarketingNazrinaazAhmadNo ratings yet

- Government Finance Statistics (GFSX) : Valuation of TransactionsDocument2 pagesGovernment Finance Statistics (GFSX) : Valuation of TransactionsKhenneth BalcetaNo ratings yet

- Thrift by Smiles, Samuel, 1812-1904Document224 pagesThrift by Smiles, Samuel, 1812-1904Gutenberg.orgNo ratings yet

- Manacc Online QuizDocument3 pagesManacc Online QuizJoshuaTagayunaNo ratings yet

- Week 11 Tutorial SolutionsDocument6 pagesWeek 11 Tutorial SolutionsMiss SlayerNo ratings yet

- 7 THDocument2 pages7 THUsama AhmedNo ratings yet

- Lab 1Document5 pagesLab 1Nguyen Phung Thinh K17 HLNo ratings yet

- Economics I 1005Document23 pagesEconomics I 1005meetwithsanjay100% (1)

- Bureau of Local Government Finance Opinion: Mr. Genestor E. CruzDocument3 pagesBureau of Local Government Finance Opinion: Mr. Genestor E. CruzNash Ortiz LuisNo ratings yet

- Syllabus Grouping of Subjects and Scheme of ExaminationDocument29 pagesSyllabus Grouping of Subjects and Scheme of ExaminationAbhisek AgrawalNo ratings yet

- Formulae and Discount Tables: Professional Level Examination Financial ManagementDocument2 pagesFormulae and Discount Tables: Professional Level Examination Financial ManagementClaudine CjNo ratings yet

- Grace Hesketh Is The Owner of An Extremely Successful DressDocument2 pagesGrace Hesketh Is The Owner of An Extremely Successful DressAmit PandeyNo ratings yet

- Cost Sheet 1Document6 pagesCost Sheet 1Tamilselvi ANo ratings yet

- Republic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Document24 pagesRepublic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Johayra AbbasNo ratings yet

- Global Oil and Gas IndustryDocument23 pagesGlobal Oil and Gas IndustryYash Agarwal100% (1)

- Estimates OF State Domestic Product, Odisha: (Both at Basic Prices and Market Prices)Document24 pagesEstimates OF State Domestic Product, Odisha: (Both at Basic Prices and Market Prices)naina saxenaNo ratings yet

- AUDI in ChinaDocument11 pagesAUDI in ChinaSen PrashantNo ratings yet

- Supply Takeout Data PDFDocument1 pageSupply Takeout Data PDFActive88No ratings yet

- Final Exam Set A MafDocument6 pagesFinal Exam Set A MafZeyad Tareq Al SaroriNo ratings yet