Download as pptx, pdf, or txt

You might also like

- Full Download Ebook Ebook PDF Microeconomics 10th Edition by William Boyes PDFDocument41 pagesFull Download Ebook Ebook PDF Microeconomics 10th Edition by William Boyes PDFdanny.wainer321100% (44)

- Revolut Stay and Spend LetterDocument2 pagesRevolut Stay and Spend LetterJonathan KeaneNo ratings yet

- CEDocument1 pageCEMirela-Elena PopaNo ratings yet

- KF) V/F Ljt/0F S) GB - : CF J @) &%÷& Jflif (S LdiffDocument16 pagesKF) V/F Ljt/0F S) GB - : CF J @) &%÷& Jflif (S LdiffNikeshManandharNo ratings yet

- Wheat - Performance Review FY 2019-20Document12 pagesWheat - Performance Review FY 2019-20Harsh WardhanNo ratings yet

- Regional-Provincial-Agri Profile (Rizal) - As of March 3, 2023Document53 pagesRegional-Provincial-Agri Profile (Rizal) - As of March 3, 2023Gamel DeanNo ratings yet

- AR Equity PDFDocument6 pagesAR Equity PDFnani reddyNo ratings yet

- Entretien Split Résidence DDPDocument2 pagesEntretien Split Résidence DDPyvandim19No ratings yet

- Iluka Resources Limited: Interim ReportDocument38 pagesIluka Resources Limited: Interim ReportTimBarrowsNo ratings yet

- EIA - Energy Consumption by SectorDocument21 pagesEIA - Energy Consumption by SectorBORJANo ratings yet

- Overview of National Grid's Balancing Services: Lilian Macleod, Strategy and Policy, Market Operation, National GridDocument9 pagesOverview of National Grid's Balancing Services: Lilian Macleod, Strategy and Policy, Market Operation, National GridroyclhorNo ratings yet

- Havells India Limited June 2018Document26 pagesHavells India Limited June 2018srishti sharma.ayush1995No ratings yet

- Fy20 Agm PresentationDocument21 pagesFy20 Agm PresentationVinay BNo ratings yet

- Alkyl AminesDocument8 pagesAlkyl AminesSriram RanganathanNo ratings yet

- HOPE Summary: Finance & Logistics DeptDocument11 pagesHOPE Summary: Finance & Logistics Dept오승환No ratings yet

- General 481 BSES Yamuna DISCOM 0Document35 pagesGeneral 481 BSES Yamuna DISCOM 0shashank chawdharyNo ratings yet

- 2021 Presentation Eng FinalDocument20 pages2021 Presentation Eng FinalShambavaNo ratings yet

- Wa0007.Document19 pagesWa0007.Anu SinghNo ratings yet

- Business Plan Car DealershipDocument1 pageBusiness Plan Car DealershipGirish SalujaNo ratings yet

- Peru: Sample Size Definition For Phone Screen and Face-To-Face InterviewsDocument2 pagesPeru: Sample Size Definition For Phone Screen and Face-To-Face InterviewsMauricio PizarroNo ratings yet

- United Tractors (UNTR IJ) : Regional Morning NotesDocument5 pagesUnited Tractors (UNTR IJ) : Regional Morning NotesAmirul AriffNo ratings yet

- Stock Decoder - Skipper Ltd-202402261647087215913Document1 pageStock Decoder - Skipper Ltd-202402261647087215913patelankurrhpmNo ratings yet

- Havells India Limited Oct 2018Document26 pagesHavells India Limited Oct 2018Raghav BhatnagarNo ratings yet

- Research Report ITC LTD PDFDocument8 pagesResearch Report ITC LTD PDFPriyanashi JainNo ratings yet

- SIMP-InvestorNewsletter 062022Document1 pageSIMP-InvestorNewsletter 062022reynaldo.beatNo ratings yet

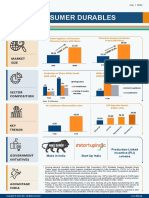

- Consumer Durables Infographic July 2021Document1 pageConsumer Durables Infographic July 2021HIMANSHU RAWATNo ratings yet

- Organisation: Cesu at A Glance As On 31.03.2010Document4 pagesOrganisation: Cesu at A Glance As On 31.03.2010havejsnjNo ratings yet

- Kalabai Laxman SapkaleDocument2 pagesKalabai Laxman SapkalePankaj AmaleNo ratings yet

- Untr 20190725Document5 pagesUntr 20190725endjoy_adjaNo ratings yet

- Premium After NCB: Class of VehicleDocument1 pagePremium After NCB: Class of VehicleSamaNo ratings yet

- Pdffile 1700758477537Document19 pagesPdffile 17007584775379tkpvc46rgNo ratings yet

- BulgariaDocument2 pagesBulgarialeonardbr05No ratings yet

- Webinar Vehicle To GridDocument28 pagesWebinar Vehicle To GridProvocateur SamaraNo ratings yet

- KPPAS May24 - Trading Biz - To PG - To CommentsDocument7 pagesKPPAS May24 - Trading Biz - To PG - To CommentsPg ChongNo ratings yet

- DISCOMs PresentationDocument17 pagesDISCOMs PresentationR&I HVPN0% (1)

- KEPCODocument27 pagesKEPCOToVanNo ratings yet

- Iex 20200831 Mosl Ic PG038Document38 pagesIex 20200831 Mosl Ic PG038Jagannath DNo ratings yet

- BUS 5010 Final ProjectDocument40 pagesBUS 5010 Final ProjectDEENo ratings yet

- Sylvia FurtadoDocument42 pagesSylvia Furtadokrishna PatelNo ratings yet

- 2020 Power Situation Report As of 09 September 2021Document52 pages2020 Power Situation Report As of 09 September 2021Mark Jaworski CadayongNo ratings yet

- Goodyear India 19-03-2021 IciciDocument6 pagesGoodyear India 19-03-2021 IcicianjugaduNo ratings yet

- Development Perspectives of The Natural Gas Industry: Superintendência de Infraestrutura e Movimentação-SIMDocument19 pagesDevelopment Perspectives of The Natural Gas Industry: Superintendência de Infraestrutura e Movimentação-SIMRuan Duarte Jales AnselmoNo ratings yet

- Brief Tank Sessions Águila 0 - 0Document44 pagesBrief Tank Sessions Águila 0 - 0Daniel MoraNo ratings yet

- Sun Pharma - EQuity Reserch ReportDocument6 pagesSun Pharma - EQuity Reserch ReportsmitNo ratings yet

- Q1FY24Document10 pagesQ1FY24DarrylNo ratings yet

- Leong Hup International BHD: TP: RM0.84Document4 pagesLeong Hup International BHD: TP: RM0.84KeyaNo ratings yet

- Market AnalysisDocument11 pagesMarket Analysissatya ghoshNo ratings yet

- Axis Detailed Report - May 2020 PDFDocument118 pagesAxis Detailed Report - May 2020 PDFRohan AdlakhaNo ratings yet

- L&T Technology Services LTDDocument40 pagesL&T Technology Services LTDCatAsticNo ratings yet

- IFB Industries-3QFY18 Result Update-8 February 2018Document8 pagesIFB Industries-3QFY18 Result Update-8 February 2018Simi GuptaNo ratings yet

- Final Payment / Reimbursment Voucher For Supply of Mi SystemDocument7 pagesFinal Payment / Reimbursment Voucher For Supply of Mi Systemdilip jotavaNo ratings yet

- Lonsum Highlights FY23Document1 pageLonsum Highlights FY23William ArdianNo ratings yet

- MSEDCL - Bill Info - PDF 788Document4 pagesMSEDCL - Bill Info - PDF 788Mahesh MirajkarNo ratings yet

- Investor Presentation: Bharti Airtel Limited Bharti Airtel LimitedDocument29 pagesInvestor Presentation: Bharti Airtel Limited Bharti Airtel LimitedArijit ChakrabortyNo ratings yet

- CCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Document29 pagesCCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Amit PatelNo ratings yet

- Bartronics Update 16 Oct. 2009Document7 pagesBartronics Update 16 Oct. 2009achopra14No ratings yet

- Bell Peppers JVDocument1 pageBell Peppers JVSara CooperNo ratings yet

- 6 Energy ComsumptionDocument20 pages6 Energy ComsumptionGregório marcos massinaNo ratings yet

- Investor Presentation 2019 PDFDocument34 pagesInvestor Presentation 2019 PDFPranabKumarGoswamiNo ratings yet

- Corporate Valuation: Industry: Plastic Pipe IndustryDocument12 pagesCorporate Valuation: Industry: Plastic Pipe IndustrySufy SaabNo ratings yet

- MARCH2020finalDocument37 pagesMARCH2020finalRohit AggarwalNo ratings yet

- IFFCO Tokio General Insurance Co. LTDDocument8 pagesIFFCO Tokio General Insurance Co. LTDAnonymous Ov4vr2ZSlVNo ratings yet

- Magnet Wire World Summary: Market Sector Values & Financials by CountryFrom EverandMagnet Wire World Summary: Market Sector Values & Financials by CountryNo ratings yet

- DS ProjectsDocument6 pagesDS ProjectsChairman PUNo ratings yet

- IAS Trainee 20.01.2023Document42 pagesIAS Trainee 20.01.2023Chairman PUNo ratings yet

- SLDCDocument1 pageSLDCChairman PUNo ratings yet

- Haryana Civil Services Pay RulesDocument66 pagesHaryana Civil Services Pay RulesChairman PUNo ratings yet

- Rfa 2011 en Us38144g8042Document228 pagesRfa 2011 en Us38144g8042Thái NguyễnNo ratings yet

- Review Economic Monthly: Bank of TanzaniaDocument33 pagesReview Economic Monthly: Bank of TanzaniaAnonymous FnM14a0No ratings yet

- (ECON2113) (2017) (F) Final 63uz5yz22zf 65641 PDFDocument2 pages(ECON2113) (2017) (F) Final 63uz5yz22zf 65641 PDFNamanNo ratings yet

- ENT 430 International Business IIDocument329 pagesENT 430 International Business IIEmeka Ken NwosuNo ratings yet

- IPCR2022 JulyDocument2 pagesIPCR2022 JulyJuly Rose LamagNo ratings yet

- 04 Task Performance 1Document6 pages04 Task Performance 1Hanna LyNo ratings yet

- VAT Refund Directive 24-2008 (English)Document5 pagesVAT Refund Directive 24-2008 (English)YoNo ratings yet

- Liquidity RatioDocument4 pagesLiquidity RatioskylarNo ratings yet

- Chapter I The Land and The PeopleDocument111 pagesChapter I The Land and The Peopleshabbir hussainNo ratings yet

- Guidelines For Standard Products For Fire and Allied Perils - Bharat Griha Raksha, Bharat Sookshma Udyam Suraksha and Bharat Laghu Udyam SurakshaDocument17 pagesGuidelines For Standard Products For Fire and Allied Perils - Bharat Griha Raksha, Bharat Sookshma Udyam Suraksha and Bharat Laghu Udyam SurakshaAtul KumarNo ratings yet

- BERYLLS Study Top 100 Supplier-2019 ENDocument16 pagesBERYLLS Study Top 100 Supplier-2019 ENJorge Navarro BeckerNo ratings yet

- Policy For Mortgaged of Licenced Land in Lieu of BGDocument2 pagesPolicy For Mortgaged of Licenced Land in Lieu of BGSarthak ShuklaNo ratings yet

- Cara Menghitung Biaya K3Document53 pagesCara Menghitung Biaya K3H. Muhammad Temter GandaNo ratings yet

- Fsav 6e Test Bank Mod14 TF MC 101520Document10 pagesFsav 6e Test Bank Mod14 TF MC 101520pauline leNo ratings yet

- Phone BillDocument1 pagePhone BillAbhishekSaurabhNo ratings yet

- Business Finance: Quarter I (Week 5)Document12 pagesBusiness Finance: Quarter I (Week 5)clarisse ginez83% (6)

- Introduction To Production and Operation Management: Chapter OutlineDocument12 pagesIntroduction To Production and Operation Management: Chapter Outlineyza gunidaNo ratings yet

- Your College NameDocument22 pagesYour College NamegihanNo ratings yet

- MoneyLab ReaderDocument311 pagesMoneyLab ReaderLouise Pasteur de FariaNo ratings yet

- Application For Cancellation or Variation of Nomination in An Account Under National Savings SchemeDocument1 pageApplication For Cancellation or Variation of Nomination in An Account Under National Savings SchemeParul GuleriaNo ratings yet

- Lets-Go-Webinar-Entrepreneurship-In-The-Digital-Age-E-Commerce-Fundamentals-Reaction PaperDocument2 pagesLets-Go-Webinar-Entrepreneurship-In-The-Digital-Age-E-Commerce-Fundamentals-Reaction PaperDanica Balindoa VillafuerteNo ratings yet

- SMES Insolvency - A.G. Martinez 2022Document65 pagesSMES Insolvency - A.G. Martinez 2022Vilija MogenyteNo ratings yet

- Thesis On Unemployment in Nigeria PDFDocument7 pagesThesis On Unemployment in Nigeria PDFHelpWithYourPaperAurora100% (2)

- Flygt 4320 MixersDocument4 pagesFlygt 4320 MixersEder Callejas PerezNo ratings yet

- MBA FPX5008 - Assessment2 1Document11 pagesMBA FPX5008 - Assessment2 1AA TsolScholarNo ratings yet

- Recommended VendorsDocument1 pageRecommended Vendorsapi-26011493No ratings yet

- Corporate Finance Group AssignmentDocument3 pagesCorporate Finance Group AssignmentGitanshNo ratings yet