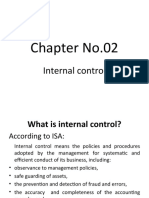

Audit Risk (Audit Alertness)

Audit Risk (Audit Alertness)

You might also like

- CB Module 3 Constructive AccountingDocument133 pagesCB Module 3 Constructive AccountingNiccolo Quintero Garcia100% (6)

- Bank Branch Internal Audit Work ProgramDocument31 pagesBank Branch Internal Audit Work Programozlem100% (1)

- Deposit Function PDFDocument75 pagesDeposit Function PDFrojon pharmacyNo ratings yet

- Module 3Document133 pagesModule 3Arra StypayhorliksonNo ratings yet

- Chapter No.02: Internal ControlDocument28 pagesChapter No.02: Internal ControlMasood khanNo ratings yet

- Balance Means Misstatement of Some Other AccountsDocument3 pagesBalance Means Misstatement of Some Other AccountsKaila Mae Tan DuNo ratings yet

- E2C-FMP-008 Accounting and Finance ProcedureDocument12 pagesE2C-FMP-008 Accounting and Finance ProcedureVPN NetworkNo ratings yet

- PSDB Internal Control StandardsDocument8 pagesPSDB Internal Control StandardsjoachimjackNo ratings yet

- Internal CheckDocument14 pagesInternal CheckAasir NaQviNo ratings yet

- Chapter 2 - SkimmingDocument8 pagesChapter 2 - SkimmingYenttirb NeyugnNo ratings yet

- Frauds in Transactions and Controls To Prevent ItDocument7 pagesFrauds in Transactions and Controls To Prevent ItShiva GamingNo ratings yet

- Branch Operations - Risk AreasDocument21 pagesBranch Operations - Risk AreasAva Vierra Perez-ViejoNo ratings yet

- Aue 2602 - Cycles - Internal Controls - 2014Document54 pagesAue 2602 - Cycles - Internal Controls - 2014Denver CordonNo ratings yet

- Unit 2 - Vouching: Vouching OF Cash ReceiptsDocument11 pagesUnit 2 - Vouching: Vouching OF Cash ReceiptsDeeksha KapoorNo ratings yet

- Ghosh Committee ReDocument3 pagesGhosh Committee ReChetan HiraparaNo ratings yet

- Chapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashDocument35 pagesChapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashEmey CalbayNo ratings yet

- Responseible Checking ProjectDocument5 pagesResponseible Checking Projectapi-276233199No ratings yet

- Cash Handling Policy and ProceduresDocument15 pagesCash Handling Policy and ProceduresLeizza Ni Gui DulaNo ratings yet

- Errors & FraudsDocument27 pagesErrors & FraudsmostakNo ratings yet

- Mod 5 - AuditingDocument51 pagesMod 5 - AuditingInchara S Dept of MBANo ratings yet

- Rights & Obligations of Parties To A ChequeDocument2 pagesRights & Obligations of Parties To A ChequeHammad ZafarNo ratings yet

- Notes: MARCH 18, 2021Document4 pagesNotes: MARCH 18, 2021Joris YapNo ratings yet

- AT Lecture 8 - Tests of Transaction CycleDocument13 pagesAT Lecture 8 - Tests of Transaction CycleダニエルNo ratings yet

- AUDIT OF CashDocument24 pagesAUDIT OF CashMr.AccntngNo ratings yet

- Module 7Document27 pagesModule 7Maricel SanchezNo ratings yet

- Accounting For Government Revenue and Expenditure.Document19 pagesAccounting For Government Revenue and Expenditure.ERICK MLINGWANo ratings yet

- Cash Controland Deposit ProceduresDocument5 pagesCash Controland Deposit ProceduresbangtansonyeondaNo ratings yet

- Unit 2 Audit of Cash and Marketable SecuritiesDocument9 pagesUnit 2 Audit of Cash and Marketable Securitiessolomon adamuNo ratings yet

- Auditing Unit 1Document39 pagesAuditing Unit 1Haseeb AhmedNo ratings yet

- Internal Control ChecklistDocument5 pagesInternal Control ChecklistPHILLIT CLASSNo ratings yet

- Auditing-Unit 3-VouchingDocument12 pagesAuditing-Unit 3-VouchingAnitha RNo ratings yet

- Cash and Securities DepartmentDocument38 pagesCash and Securities DepartmentHAMMADHRNo ratings yet

- Internal RoutineDocument10 pagesInternal RoutineAris Mae LepartoNo ratings yet

- Cash Handling Policy For Express Kitchen LTDDocument3 pagesCash Handling Policy For Express Kitchen LTDjohnkimani243No ratings yet

- Duties and ResponsibilitiesDocument2 pagesDuties and ResponsibilitiesVictorina Mcy BagnadenNo ratings yet

- Cash Handling and Accounts Receivable Policy PresentationDocument22 pagesCash Handling and Accounts Receivable Policy PresentationJSNo ratings yet

- Cashing Tills PDFDocument17 pagesCashing Tills PDFAna-Maria BadeaNo ratings yet

- MODULE 8 - Test of ControlsDocument16 pagesMODULE 8 - Test of ControlsRufina B VerdeNo ratings yet

- Cash Receipts CycleDocument4 pagesCash Receipts CycleYenNo ratings yet

- Loss Prevention PolicyDocument6 pagesLoss Prevention PolicyPQLicensingNo ratings yet

- Different Areas of Frauds in BanksDocument4 pagesDifferent Areas of Frauds in BanksKush SinghNo ratings yet

- Internal Audit and Budget Department - Cash ReceiptsDocument13 pagesInternal Audit and Budget Department - Cash ReceiptsMarineth Monsanto100% (1)

- Roles and Responsibilities & Taking Over: Module-1Document15 pagesRoles and Responsibilities & Taking Over: Module-1kailas bankNo ratings yet

- AssuranceDocument3 pagesAssurancehazel.yiran.liuNo ratings yet

- Internal Control ProceduresDocument13 pagesInternal Control ProceduresAndre CarrerasNo ratings yet

- 02 - Audi.... Chap. 02 - OKDocument48 pages02 - Audi.... Chap. 02 - OKFazila AzharNo ratings yet

- Awtlang Walang LineDocument4 pagesAwtlang Walang Linejoseph lasayNo ratings yet

- Group 2 Revenue CycleDocument24 pagesGroup 2 Revenue CyclegelaNo ratings yet

- Chapter 4 - Cash and Internal ControlsDocument10 pagesChapter 4 - Cash and Internal Controlsvictoria.05.santosNo ratings yet

- Material CVDocument2 pagesMaterial CVmuhammadnoman086No ratings yet

- Chapter 5 DUTYDocument19 pagesChapter 5 DUTYtemedebereNo ratings yet

- Accounting, Unit 1 - Topic 1Document68 pagesAccounting, Unit 1 - Topic 1Teal JacobsNo ratings yet

- Financial AccountingDocument17 pagesFinancial AccountingYukino YukinoshitaNo ratings yet

- Final Quiz ReviewDocument17 pagesFinal Quiz ReviewHibbah OwaisNo ratings yet

- 6 Cash TransactionsDocument29 pages6 Cash TransactionsZindgiKiKhatirNo ratings yet

- Sample Sacco Internal Controls PolicyDocument11 pagesSample Sacco Internal Controls PolicyAmulioto Elijah MuchelleNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Cca RulesDocument55 pagesCca RulesdimbhaNo ratings yet

- Public WorksDocument56 pagesPublic WorksdimbhaNo ratings yet

- PCA - Lokayukta ActDocument12 pagesPCA - Lokayukta ActdimbhaNo ratings yet

- G.P BudgetDocument20 pagesG.P BudgetdimbhaNo ratings yet

- Form of Application For Final Payment of Balances in The General Provident Fund Account To The Account General Karnataka, BangaloreDocument2 pagesForm of Application For Final Payment of Balances in The General Provident Fund Account To The Account General Karnataka, BangaloredimbhaNo ratings yet

- Below Poverty LineDocument12 pagesBelow Poverty LinedimbhaNo ratings yet

- Srikalahasti Rahu Ketu Pooja - Tickets - Online Booking - Timings - DaysDocument5 pagesSrikalahasti Rahu Ketu Pooja - Tickets - Online Booking - Timings - DaysdimbhaNo ratings yet

- HRMS Dos DontsDocument7 pagesHRMS Dos DontsdimbhaNo ratings yet

- Gunda KriyeDocument14 pagesGunda KriyedimbhaNo ratings yet

- Sri Vadirajaguru StotramDocument6 pagesSri Vadirajaguru StotramdimbhaNo ratings yet

- Samantha Smith Jeff Smith: Coho Vineyard and Winery 5678 Vineyard Drive Whidbey Island, Wa 48823Document1 pageSamantha Smith Jeff Smith: Coho Vineyard and Winery 5678 Vineyard Drive Whidbey Island, Wa 48823dimbhaNo ratings yet

- Vis Cond of RoadsDocument6 pagesVis Cond of RoadsdimbhaNo ratings yet

- Machinary Returns For The Month of October-2010: Reg .NoDocument34 pagesMachinary Returns For The Month of October-2010: Reg .NodimbhaNo ratings yet

- Yuva Samsath 2011-12Document110 pagesYuva Samsath 2011-12dimbhaNo ratings yet

- ಸರ್ಕಾರಿ ಅಧಿಕಾರಿ ನೌಕರರುಗಳ ವಿರುದ್ಧ ಶಿಸ್ತುಕ್ರಮ ಇಲಾಖಾ ವಿಚಾರಣೆಯ ಅವಶ್ಯಕ ಪರಿಪೂರ್ಣ ಪ್ರಸ್ತಾವನೆಗಳನ್ನು ವಿಳಂಬವಿಲ್ಲದೇ ಸಲ್ಲಿಸುವ ಬಗ್ಗೆ ಮರು ಸೂಚನೆಗಳು PDFDocument3 pagesಸರ್ಕಾರಿ ಅಧಿಕಾರಿ ನೌಕರರುಗಳ ವಿರುದ್ಧ ಶಿಸ್ತುಕ್ರಮ ಇಲಾಖಾ ವಿಚಾರಣೆಯ ಅವಶ್ಯಕ ಪರಿಪೂರ್ಣ ಪ್ರಸ್ತಾವನೆಗಳನ್ನು ವಿಳಂಬವಿಲ್ಲದೇ ಸಲ್ಲಿಸುವ ಬಗ್ಗೆ ಮರು ಸೂಚನೆಗಳು PDFdimbhaNo ratings yet

- Páaiàäð Áðºàpà C©Üaiàäavàgà Àgà Pàbéãj,: ( Éæãpéæã Àaiéæãv, Azàgàä Àävàäû M À Áqàä D® Ájué E Ásé)Document1 pagePáaiàäð Áðºàpà C©Üaiàäavàgà Àgà Pàbéãj,: ( Éæãpéæã Àaiéæãv, Azàgàä Àävàäû M À Áqàä D® Ájué E Ásé)dimbhaNo ratings yet

- Part EOG (Page 1069 1212)Document144 pagesPart EOG (Page 1069 1212)dimbhaNo ratings yet

Download as pptx, pdf, or txt

You might also like

- CB Module 3 Constructive AccountingDocument133 pagesCB Module 3 Constructive AccountingNiccolo Quintero Garcia100% (6)

- Bank Branch Internal Audit Work ProgramDocument31 pagesBank Branch Internal Audit Work Programozlem100% (1)

- Deposit Function PDFDocument75 pagesDeposit Function PDFrojon pharmacyNo ratings yet

- Module 3Document133 pagesModule 3Arra StypayhorliksonNo ratings yet

- Chapter No.02: Internal ControlDocument28 pagesChapter No.02: Internal ControlMasood khanNo ratings yet

- Balance Means Misstatement of Some Other AccountsDocument3 pagesBalance Means Misstatement of Some Other AccountsKaila Mae Tan DuNo ratings yet

- E2C-FMP-008 Accounting and Finance ProcedureDocument12 pagesE2C-FMP-008 Accounting and Finance ProcedureVPN NetworkNo ratings yet

- PSDB Internal Control StandardsDocument8 pagesPSDB Internal Control StandardsjoachimjackNo ratings yet

- Internal CheckDocument14 pagesInternal CheckAasir NaQviNo ratings yet

- Chapter 2 - SkimmingDocument8 pagesChapter 2 - SkimmingYenttirb NeyugnNo ratings yet

- Frauds in Transactions and Controls To Prevent ItDocument7 pagesFrauds in Transactions and Controls To Prevent ItShiva GamingNo ratings yet

- Branch Operations - Risk AreasDocument21 pagesBranch Operations - Risk AreasAva Vierra Perez-ViejoNo ratings yet

- Aue 2602 - Cycles - Internal Controls - 2014Document54 pagesAue 2602 - Cycles - Internal Controls - 2014Denver CordonNo ratings yet

- Unit 2 - Vouching: Vouching OF Cash ReceiptsDocument11 pagesUnit 2 - Vouching: Vouching OF Cash ReceiptsDeeksha KapoorNo ratings yet

- Ghosh Committee ReDocument3 pagesGhosh Committee ReChetan HiraparaNo ratings yet

- Chapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashDocument35 pagesChapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashEmey CalbayNo ratings yet

- Responseible Checking ProjectDocument5 pagesResponseible Checking Projectapi-276233199No ratings yet

- Cash Handling Policy and ProceduresDocument15 pagesCash Handling Policy and ProceduresLeizza Ni Gui DulaNo ratings yet

- Errors & FraudsDocument27 pagesErrors & FraudsmostakNo ratings yet

- Mod 5 - AuditingDocument51 pagesMod 5 - AuditingInchara S Dept of MBANo ratings yet

- Rights & Obligations of Parties To A ChequeDocument2 pagesRights & Obligations of Parties To A ChequeHammad ZafarNo ratings yet

- Notes: MARCH 18, 2021Document4 pagesNotes: MARCH 18, 2021Joris YapNo ratings yet

- AT Lecture 8 - Tests of Transaction CycleDocument13 pagesAT Lecture 8 - Tests of Transaction CycleダニエルNo ratings yet

- AUDIT OF CashDocument24 pagesAUDIT OF CashMr.AccntngNo ratings yet

- Module 7Document27 pagesModule 7Maricel SanchezNo ratings yet

- Accounting For Government Revenue and Expenditure.Document19 pagesAccounting For Government Revenue and Expenditure.ERICK MLINGWANo ratings yet

- Cash Controland Deposit ProceduresDocument5 pagesCash Controland Deposit ProceduresbangtansonyeondaNo ratings yet

- Unit 2 Audit of Cash and Marketable SecuritiesDocument9 pagesUnit 2 Audit of Cash and Marketable Securitiessolomon adamuNo ratings yet

- Auditing Unit 1Document39 pagesAuditing Unit 1Haseeb AhmedNo ratings yet

- Internal Control ChecklistDocument5 pagesInternal Control ChecklistPHILLIT CLASSNo ratings yet

- Auditing-Unit 3-VouchingDocument12 pagesAuditing-Unit 3-VouchingAnitha RNo ratings yet

- Cash and Securities DepartmentDocument38 pagesCash and Securities DepartmentHAMMADHRNo ratings yet

- Internal RoutineDocument10 pagesInternal RoutineAris Mae LepartoNo ratings yet

- Cash Handling Policy For Express Kitchen LTDDocument3 pagesCash Handling Policy For Express Kitchen LTDjohnkimani243No ratings yet

- Duties and ResponsibilitiesDocument2 pagesDuties and ResponsibilitiesVictorina Mcy BagnadenNo ratings yet

- Cash Handling and Accounts Receivable Policy PresentationDocument22 pagesCash Handling and Accounts Receivable Policy PresentationJSNo ratings yet

- Cashing Tills PDFDocument17 pagesCashing Tills PDFAna-Maria BadeaNo ratings yet

- MODULE 8 - Test of ControlsDocument16 pagesMODULE 8 - Test of ControlsRufina B VerdeNo ratings yet

- Cash Receipts CycleDocument4 pagesCash Receipts CycleYenNo ratings yet

- Loss Prevention PolicyDocument6 pagesLoss Prevention PolicyPQLicensingNo ratings yet

- Different Areas of Frauds in BanksDocument4 pagesDifferent Areas of Frauds in BanksKush SinghNo ratings yet

- Internal Audit and Budget Department - Cash ReceiptsDocument13 pagesInternal Audit and Budget Department - Cash ReceiptsMarineth Monsanto100% (1)

- Roles and Responsibilities & Taking Over: Module-1Document15 pagesRoles and Responsibilities & Taking Over: Module-1kailas bankNo ratings yet

- AssuranceDocument3 pagesAssurancehazel.yiran.liuNo ratings yet

- Internal Control ProceduresDocument13 pagesInternal Control ProceduresAndre CarrerasNo ratings yet

- 02 - Audi.... Chap. 02 - OKDocument48 pages02 - Audi.... Chap. 02 - OKFazila AzharNo ratings yet

- Awtlang Walang LineDocument4 pagesAwtlang Walang Linejoseph lasayNo ratings yet

- Group 2 Revenue CycleDocument24 pagesGroup 2 Revenue CyclegelaNo ratings yet

- Chapter 4 - Cash and Internal ControlsDocument10 pagesChapter 4 - Cash and Internal Controlsvictoria.05.santosNo ratings yet

- Material CVDocument2 pagesMaterial CVmuhammadnoman086No ratings yet

- Chapter 5 DUTYDocument19 pagesChapter 5 DUTYtemedebereNo ratings yet

- Accounting, Unit 1 - Topic 1Document68 pagesAccounting, Unit 1 - Topic 1Teal JacobsNo ratings yet

- Financial AccountingDocument17 pagesFinancial AccountingYukino YukinoshitaNo ratings yet

- Final Quiz ReviewDocument17 pagesFinal Quiz ReviewHibbah OwaisNo ratings yet

- 6 Cash TransactionsDocument29 pages6 Cash TransactionsZindgiKiKhatirNo ratings yet

- Sample Sacco Internal Controls PolicyDocument11 pagesSample Sacco Internal Controls PolicyAmulioto Elijah MuchelleNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Cca RulesDocument55 pagesCca RulesdimbhaNo ratings yet

- Public WorksDocument56 pagesPublic WorksdimbhaNo ratings yet

- PCA - Lokayukta ActDocument12 pagesPCA - Lokayukta ActdimbhaNo ratings yet

- G.P BudgetDocument20 pagesG.P BudgetdimbhaNo ratings yet

- Form of Application For Final Payment of Balances in The General Provident Fund Account To The Account General Karnataka, BangaloreDocument2 pagesForm of Application For Final Payment of Balances in The General Provident Fund Account To The Account General Karnataka, BangaloredimbhaNo ratings yet

- Below Poverty LineDocument12 pagesBelow Poverty LinedimbhaNo ratings yet

- Srikalahasti Rahu Ketu Pooja - Tickets - Online Booking - Timings - DaysDocument5 pagesSrikalahasti Rahu Ketu Pooja - Tickets - Online Booking - Timings - DaysdimbhaNo ratings yet

- HRMS Dos DontsDocument7 pagesHRMS Dos DontsdimbhaNo ratings yet

- Gunda KriyeDocument14 pagesGunda KriyedimbhaNo ratings yet

- Sri Vadirajaguru StotramDocument6 pagesSri Vadirajaguru StotramdimbhaNo ratings yet

- Samantha Smith Jeff Smith: Coho Vineyard and Winery 5678 Vineyard Drive Whidbey Island, Wa 48823Document1 pageSamantha Smith Jeff Smith: Coho Vineyard and Winery 5678 Vineyard Drive Whidbey Island, Wa 48823dimbhaNo ratings yet

- Vis Cond of RoadsDocument6 pagesVis Cond of RoadsdimbhaNo ratings yet

- Machinary Returns For The Month of October-2010: Reg .NoDocument34 pagesMachinary Returns For The Month of October-2010: Reg .NodimbhaNo ratings yet

- Yuva Samsath 2011-12Document110 pagesYuva Samsath 2011-12dimbhaNo ratings yet

- ಸರ್ಕಾರಿ ಅಧಿಕಾರಿ ನೌಕರರುಗಳ ವಿರುದ್ಧ ಶಿಸ್ತುಕ್ರಮ ಇಲಾಖಾ ವಿಚಾರಣೆಯ ಅವಶ್ಯಕ ಪರಿಪೂರ್ಣ ಪ್ರಸ್ತಾವನೆಗಳನ್ನು ವಿಳಂಬವಿಲ್ಲದೇ ಸಲ್ಲಿಸುವ ಬಗ್ಗೆ ಮರು ಸೂಚನೆಗಳು PDFDocument3 pagesಸರ್ಕಾರಿ ಅಧಿಕಾರಿ ನೌಕರರುಗಳ ವಿರುದ್ಧ ಶಿಸ್ತುಕ್ರಮ ಇಲಾಖಾ ವಿಚಾರಣೆಯ ಅವಶ್ಯಕ ಪರಿಪೂರ್ಣ ಪ್ರಸ್ತಾವನೆಗಳನ್ನು ವಿಳಂಬವಿಲ್ಲದೇ ಸಲ್ಲಿಸುವ ಬಗ್ಗೆ ಮರು ಸೂಚನೆಗಳು PDFdimbhaNo ratings yet

- Páaiàäð Áðºàpà C©Üaiàäavàgà Àgà Pàbéãj,: ( Éæãpéæã Àaiéæãv, Azàgàä Àävàäû M À Áqàä D® Ájué E Ásé)Document1 pagePáaiàäð Áðºàpà C©Üaiàäavàgà Àgà Pàbéãj,: ( Éæãpéæã Àaiéæãv, Azàgàä Àävàäû M À Áqàä D® Ájué E Ásé)dimbhaNo ratings yet

- Part EOG (Page 1069 1212)Document144 pagesPart EOG (Page 1069 1212)dimbhaNo ratings yet