Download as pptx, pdf, or txt

You might also like

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- Chapter 15 - Accounting For CorporationsDocument22 pagesChapter 15 - Accounting For CorporationsAlizah BucotNo ratings yet

- Final Exam Key Answer FarDocument3 pagesFinal Exam Key Answer FarComedy Royal Philippines100% (1)

- Holding Period & Expected Return With AnswersDocument2 pagesHolding Period & Expected Return With AnswersSiddhant AggarwalNo ratings yet

- CorporateDocument27 pagesCorporateMega Pop LockerNo ratings yet

- Tax NumericalsDocument11 pagesTax NumericalsRohit PanpatilNo ratings yet

- Long Term Financing MCQ IM PANDEYDocument3 pagesLong Term Financing MCQ IM PANDEYsushmaNo ratings yet

- Stockholders EquityDocument36 pagesStockholders EquityLorenze GuintuNo ratings yet

- Shareholders' Equity: Learning CompetenciesDocument41 pagesShareholders' Equity: Learning CompetenciesRaezel Carla Santos Fontanilla100% (3)

- Acctg For SheDocument14 pagesAcctg For ShePaulo Maramba IdosNo ratings yet

- Corporate Accounting 1: III Semester BBADocument57 pagesCorporate Accounting 1: III Semester BBAAR Ananth Rohith BhatNo ratings yet

- Intermediate Accounting 3Document20 pagesIntermediate Accounting 3Gali jizNo ratings yet

- Chapter 10 Accounting For CorporationDocument6 pagesChapter 10 Accounting For CorporationAngelica Joy ManaoisNo ratings yet

- Companies Act Lecture PresentationDocument34 pagesCompanies Act Lecture PresentationNatrium SodiumNo ratings yet

- SPCM Unit 3 Bba II TMV NotesDocument11 pagesSPCM Unit 3 Bba II TMV NotesRaghuNo ratings yet

- CorporationDocument18 pagesCorporationErika Mae IsipNo ratings yet

- Capital and Its Types: Name: Saroop Cms:42529 Section: B Semester: 6 Assignment:2Document9 pagesCapital and Its Types: Name: Saroop Cms:42529 Section: B Semester: 6 Assignment:2Sanjna ChimnaniNo ratings yet

- Shares & Share CapitalDocument36 pagesShares & Share CapitalkritiNo ratings yet

- Joint Stock CompanyDocument35 pagesJoint Stock Companymo0onshahNo ratings yet

- FINACT2 Handout No. 5 2019Document6 pagesFINACT2 Handout No. 5 2019Janysse CalderonNo ratings yet

- Shareholders EquityDocument25 pagesShareholders EquityJhoanna Mary PescasioNo ratings yet

- Corporate Law - Unit 2Document17 pagesCorporate Law - Unit 2Shem W LyngdohNo ratings yet

- Chapter Five: Corporation Organization and OperationDocument8 pagesChapter Five: Corporation Organization and OperationSamuel DebebeNo ratings yet

- Corpo Lecture With Exercises BDocument10 pagesCorpo Lecture With Exercises BFatima GuevarraNo ratings yet

- Chapter Six Corporation Organization and OperationDocument8 pagesChapter Six Corporation Organization and OperationSamuel DebebeNo ratings yet

- Share and Share CapitalDocument16 pagesShare and Share CapitalChicIshuNo ratings yet

- Share: by Aju K Raju Mba Ii MiimDocument13 pagesShare: by Aju K Raju Mba Ii MiimAju K Raju100% (1)

- Accounts of Limited Company-1Document15 pagesAccounts of Limited Company-1Raghu VeerNo ratings yet

- Chapter 5 CorporationDocument12 pagesChapter 5 CorporationMamaru SewalemNo ratings yet

- Business Law: Certificate LevelDocument11 pagesBusiness Law: Certificate LevelRafidul IslamNo ratings yet

- Issue of SharesDocument53 pagesIssue of SharesKanishk GoyalNo ratings yet

- Share CapitalDocument39 pagesShare CapitalPrincess Aubrey BalbinNo ratings yet

- Share Capital, Share and MembershipDocument17 pagesShare Capital, Share and Membershipakashkr619No ratings yet

- Company Accounts: Mr. Vasim Ahmad (Research Scholar)Document37 pagesCompany Accounts: Mr. Vasim Ahmad (Research Scholar)khushnumaNo ratings yet

- Company Audit: Yash Classes Accounts-5 (Auditing)Document12 pagesCompany Audit: Yash Classes Accounts-5 (Auditing)Shilpan ShahNo ratings yet

- MeaningDocument19 pagesMeaningSrusti ParekhNo ratings yet

- ACTBFAR Lecture - Accounting For Corporation - V25Document147 pagesACTBFAR Lecture - Accounting For Corporation - V25Kristian Angelo MamarilNo ratings yet

- Corporate AccountingDocument749 pagesCorporate AccountingDr. Mohammad Noor Alam75% (8)

- Assignment 01Document13 pagesAssignment 01javieriakhan674No ratings yet

- Introduction To Issue Forfeiture and Reissue of SharesDocument37 pagesIntroduction To Issue Forfeiture and Reissue of SharesRkenterpriseNo ratings yet

- Issue of SharesDocument9 pagesIssue of SharesLearn MitraNo ratings yet

- Lecture 5 - Shareholder's Equity AccountingDocument33 pagesLecture 5 - Shareholder's Equity Accountingpeter kong100% (1)

- Share Capital & DebentureDocument17 pagesShare Capital & DebentureRajani SanjuNo ratings yet

- Owner's Equity Section of Every Corporation Is The Shareholders' EquityDocument12 pagesOwner's Equity Section of Every Corporation Is The Shareholders' EquityMon RamNo ratings yet

- Audit of Share CapitalDocument35 pagesAudit of Share CapitalHetal Bhanushali50% (6)

- Shareholders Equity Part 1Document57 pagesShareholders Equity Part 1AlliahDataNo ratings yet

- Share Capital: Urmila ItamDocument33 pagesShare Capital: Urmila ItamUrmila JagadeeswariNo ratings yet

- Shareholder S' EquityDocument55 pagesShareholder S' EquityRojParconNo ratings yet

- Handout On Chapter 12 Corporations PDFDocument9 pagesHandout On Chapter 12 Corporations PDFJeric TorionNo ratings yet

- ACCOUNTING FOR CORPORATIONS-Share CapitalDocument57 pagesACCOUNTING FOR CORPORATIONS-Share CapitalMarriel Fate Cullano75% (8)

- Share CapDocument29 pagesShare CapRabbikaNo ratings yet

- Tybcom - Share NotesDocument749 pagesTybcom - Share NotesManojj21No ratings yet

- UNIT 4: Company Accounts-Share CapitalDocument13 pagesUNIT 4: Company Accounts-Share CapitalpraveentyagiNo ratings yet

- Topic 11 EquityDocument21 pagesTopic 11 EquityAbd AL Rahman Shah Bin Azlan ShahNo ratings yet

- Edited Corporate LawsDocument12 pagesEdited Corporate LawsRashmin SolankiNo ratings yet

- Chapter 6 CorporationDocument7 pagesChapter 6 CorporationAmaa AmaaNo ratings yet

- Amity University Rajasthan: Brief Description On SharesDocument7 pagesAmity University Rajasthan: Brief Description On SharesSahida ParveenNo ratings yet

- LAB - Group 5 - Shares and DirectorDocument33 pagesLAB - Group 5 - Shares and DirectorMoulina BandyopadhyayNo ratings yet

- Shares CapitalDocument30 pagesShares CapitalDeeyla Kamarulzaman100% (1)

- Shareholders EquityDocument62 pagesShareholders EquityMark LouieNo ratings yet

- Lecture 5 - The Capital of A CompanyDocument43 pagesLecture 5 - The Capital of A CompanyZale EzekielNo ratings yet

- AuditingDocument21 pagesAuditingShilpan ShahNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- DepletionDocument2 pagesDepletioncaraaatbongNo ratings yet

- Activity in Accounting For CorporationDocument2 pagesActivity in Accounting For CorporationcaraaatbongNo ratings yet

- 2nd Interim in Purposive CommunicationDocument4 pages2nd Interim in Purposive CommunicationcaraaatbongNo ratings yet

- Purposivecommunication - Communication Processes, Principles, and Ethics (Autosaved)Document24 pagesPurposivecommunication - Communication Processes, Principles, and Ethics (Autosaved)caraaatbongNo ratings yet

- Chapter3purposivecom 201108134308Document29 pagesChapter3purposivecom 201108134308caraaatbongNo ratings yet

- Assignment in Partnership OperationsDocument4 pagesAssignment in Partnership OperationscaraaatbongNo ratings yet

- Working Papers For CorporationDocument8 pagesWorking Papers For CorporationcaraaatbongNo ratings yet

- POCHEBSA231CDocument1 pagePOCHEBSA231CcaraaatbongNo ratings yet

- Chapter 4 - Incorporation of PartnershpDocument8 pagesChapter 4 - Incorporation of PartnershpcaraaatbongNo ratings yet

- Finals Reviewer DevpsychDocument15 pagesFinals Reviewer DevpsychcaraaatbongNo ratings yet

- Enhancing Procurement Strategies For Resolving Agency Issues in ClientDocument6 pagesEnhancing Procurement Strategies For Resolving Agency Issues in ClientcaraaatbongNo ratings yet

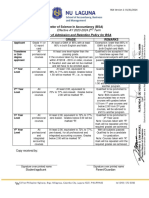

- NU Laguna BSA Admission and Retention Policy Revised 02152024Document1 pageNU Laguna BSA Admission and Retention Policy Revised 02152024caraaatbongNo ratings yet

- NSTP 1 ReviewerDocument6 pagesNSTP 1 ReviewercaraaatbongNo ratings yet

- Reviewer in Business FinanceDocument2 pagesReviewer in Business FinancecaraaatbongNo ratings yet

- The Contemporary World ReviewerDocument4 pagesThe Contemporary World ReviewercaraaatbongNo ratings yet

- Jemina InsightsDocument1 pageJemina InsightscaraaatbongNo ratings yet

- Corporation Quiz 2 Up To JournalizingDocument5 pagesCorporation Quiz 2 Up To Journalizingycalinaj.cbaNo ratings yet

- CSSA Best Practice Guide SharesDocument27 pagesCSSA Best Practice Guide ShareswNo ratings yet

- The Founders Guide To VC FinanceDocument145 pagesThe Founders Guide To VC FinanceDouggie YuNo ratings yet

- Chapter Wise Board Question Mutual Fund: Sapan ParikhDocument6 pagesChapter Wise Board Question Mutual Fund: Sapan ParikhAnkitNo ratings yet

- EventDocument14 pagesEventVenkatesh VNo ratings yet

- Chapter 2 Financail Analysis&planningDocument13 pagesChapter 2 Financail Analysis&planninganteneh hailieNo ratings yet

- 3 - Forms of Business OrganisationDocument2 pages3 - Forms of Business OrganisationNatasha RushNo ratings yet

- Acc AssignmentDocument5 pagesAcc AssignmentBlen tesfayeNo ratings yet

- Basic Earnings Per ShareDocument2 pagesBasic Earnings Per SharePaula De RuedaNo ratings yet

- Exercise Problem 3 - Shareholder's EquityDocument5 pagesExercise Problem 3 - Shareholder's EquityLLYOD FRANCIS LAYLAYNo ratings yet

- Ratio Analysis and ExamplesDocument18 pagesRatio Analysis and ExamplesUnique OfficialsNo ratings yet

- Dividend Policy of Hero Honda Over The Last 5 YearsDocument8 pagesDividend Policy of Hero Honda Over The Last 5 YearsAlex JoeNo ratings yet

- Capital - Table Excel TemplateDocument5 pagesCapital - Table Excel TemplateGolamMostafaNo ratings yet

- Manyak Company ProjectDocument12 pagesManyak Company Projectprashansha kumudNo ratings yet

- 2021 Corpo E2Document98 pages2021 Corpo E2kimber lloyd biloNo ratings yet

- 75 Questions Test - SolutionDocument65 pages75 Questions Test - SolutionCute BabiesNo ratings yet

- Emu LinesDocument22 pagesEmu LinesRahul MehraNo ratings yet

- Shareholders' Equity (Student's Reference)Document26 pagesShareholders' Equity (Student's Reference)Jhanna RoseNo ratings yet

- She HandoutsDocument7 pagesShe HandoutsBrent DumangengNo ratings yet

- Investing With Nse 500 Top GainersDocument6 pagesInvesting With Nse 500 Top GainersAnuranjan VermaNo ratings yet

- Petitioner Respondents: Anna Teng, Securities and Exchange Commission (Sec) and Ting Ping LayDocument10 pagesPetitioner Respondents: Anna Teng, Securities and Exchange Commission (Sec) and Ting Ping LayJakielyn Anne CruzNo ratings yet

- Stice 18e Ch13 SOL FinalDocument56 pagesStice 18e Ch13 SOL FinalKhôi NguyênNo ratings yet

- FORM PAS 4 - Draft Format - CommonDocument12 pagesFORM PAS 4 - Draft Format - Commonlegal shuruNo ratings yet

- Current Ratio: Interpretation and Evaluation of The Ratio Analysis of People's Insurance Company (PICL)Document50 pagesCurrent Ratio: Interpretation and Evaluation of The Ratio Analysis of People's Insurance Company (PICL)HR CHRNo ratings yet

- Problem No. 1Document5 pagesProblem No. 1Jinrikisha TimoteoNo ratings yet