Profit Planning-1

Profit Planning-1

You might also like

- Chapter 13 Budgets and Budgetary ControlDocument47 pagesChapter 13 Budgets and Budgetary ControlAndrew StarkNo ratings yet

- Which Expenses Are Fixed and Which Are Variable? Indicate The Monthly Total. Put A Check Mark On The Corresponding TypeDocument4 pagesWhich Expenses Are Fixed and Which Are Variable? Indicate The Monthly Total. Put A Check Mark On The Corresponding TypeKiem SantosNo ratings yet

- Notes On Cash BudgetDocument26 pagesNotes On Cash BudgetJoshua P.No ratings yet

- Maths Project On Home BudgetDocument21 pagesMaths Project On Home BudgetVidhi Chokhani79% (622)

- TA LectureNote-4Document13 pagesTA LectureNote-4nguyenbachptpNo ratings yet

- Review 20Document4 pagesReview 20StubadubNo ratings yet

- Budget: Definition, Classification and Types of BudgetsDocument15 pagesBudget: Definition, Classification and Types of BudgetsAnderson GuzmanNo ratings yet

- 10) BudgetingDocument5 pages10) BudgetingAlbert Krohn SandahlNo ratings yet

- Chapter 6 BudgetsDocument60 pagesChapter 6 BudgetsSandipan DawnNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- Report No. 6 Batoy Khey Heart N. Matano Naffy BDocument35 pagesReport No. 6 Batoy Khey Heart N. Matano Naffy BCamille EscoteNo ratings yet

- Operational BudgetDocument14 pagesOperational BudgetTsega BirhanuNo ratings yet

- Akmen Bab 8Document3 pagesAkmen Bab 8Hafizh GalihNo ratings yet

- CH - 2 Master Budget - Ahmed With Illustration and SolutionDocument15 pagesCH - 2 Master Budget - Ahmed With Illustration and SolutionYohannes MeridNo ratings yet

- HanduotDocument20 pagesHanduotTegene TesfayeNo ratings yet

- Budgeting Planning and ControlDocument31 pagesBudgeting Planning and Controlintan agustina100% (1)

- Chapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningDocument6 pagesChapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningAdoree RamosNo ratings yet

- Chap04 - Profit PlanningDocument36 pagesChap04 - Profit PlanningChi Nguyễn Thị KimNo ratings yet

- Cost II-Ch - 3 Master BudgetDocument14 pagesCost II-Ch - 3 Master BudgetYitera SisayNo ratings yet

- Module in BudgetingDocument5 pagesModule in BudgetingJade TanNo ratings yet

- Profit PlanningDocument5 pagesProfit PlanningChaudhry Umair YounisNo ratings yet

- Chapter 10Document13 pagesChapter 10Shane Melody G. GetonzoNo ratings yet

- Master BudgetDocument5 pagesMaster BudgetSaranyaa KanagarajNo ratings yet

- CH - 3 Master Budget - With Illustration and SolutionDocument16 pagesCH - 3 Master Budget - With Illustration and SolutionMelat TNo ratings yet

- Session 25 - BudgetingDocument27 pagesSession 25 - BudgetingVinukartik PillaiNo ratings yet

- U02 Budget Methodolgies and Budget PreparationDocument26 pagesU02 Budget Methodolgies and Budget PreparationIslam AhmedNo ratings yet

- Chapter 6Document13 pagesChapter 6yana kiutNo ratings yet

- Moduel 4Document11 pagesModuel 4sarojkumardasbsetNo ratings yet

- Summary Master BudgetingDocument5 pagesSummary Master BudgetingliaNo ratings yet

- CH 2 Cost IIDocument10 pagesCH 2 Cost IIfirewNo ratings yet

- CH7 BudgetingDocument51 pagesCH7 BudgetingYMNo ratings yet

- Chapter 5Document7 pagesChapter 5intelragadio100% (1)

- Chapter 08Document18 pagesChapter 08hana_kimi_91No ratings yet

- Budgeting and Budgetary Control 2019Document10 pagesBudgeting and Budgetary Control 2019Kerrice RobinsonNo ratings yet

- Class 9 - Managerial AccountingDocument12 pagesClass 9 - Managerial AccountingcarlaNo ratings yet

- Master Budgeting OutlineDocument14 pagesMaster Budgeting OutlineGina Mantos GocotanoNo ratings yet

- CHAPTER 3 Financial PlanningDocument7 pagesCHAPTER 3 Financial Planningflorabel parana0% (1)

- Master BudgetingDocument6 pagesMaster BudgetingKrNo ratings yet

- Developing Operating & Capital BudgetingDocument48 pagesDeveloping Operating & Capital Budgetingapi-3742302100% (2)

- Bafinmax CM7Document22 pagesBafinmax CM7Marvin AndresNo ratings yet

- Financial Management Chapter 10Document14 pagesFinancial Management Chapter 10Shane Melody G. GetonzoNo ratings yet

- Lecture 11 BIS ManagerialDocument25 pagesLecture 11 BIS Managerialnada ahmedNo ratings yet

- Profit Planning and BudgetingDocument53 pagesProfit Planning and BudgetingBhey PayumoNo ratings yet

- FM Chapter 10-1Document14 pagesFM Chapter 10-1Shane Melody G. GetonzoNo ratings yet

- CH 9 Profit Planning and Activity-Based BudgetingDocument21 pagesCH 9 Profit Planning and Activity-Based BudgetingIsra' I. SweilehNo ratings yet

- Budgeting P1Document48 pagesBudgeting P1YINGGCHI LONGNo ratings yet

- Managerial Accounting IBPDocument58 pagesManagerial Accounting IBPSaadat Ali100% (1)

- Managerial Accounting Asiacareer College/Cparcenter Operational and Financial Budgeting DWM - Reyno, Cpa, DbaDocument3 pagesManagerial Accounting Asiacareer College/Cparcenter Operational and Financial Budgeting DWM - Reyno, Cpa, DbaCertified Public AccountantNo ratings yet

- Financial Planning and Control ProcessDocument3 pagesFinancial Planning and Control ProcessPRINCESS HONEYLET SIGESMUNDONo ratings yet

- Cost CH 2Document16 pagesCost CH 2Shimelis TesemaNo ratings yet

- Master BudgetDocument6 pagesMaster BudgetPacir QubeNo ratings yet

- Brewer6ce WYRNTK Ch07Document5 pagesBrewer6ce WYRNTK Ch07Bilal ShahidNo ratings yet

- Forecasting or BudgetingDocument6 pagesForecasting or BudgetingHannah Faith BagasaniNo ratings yet

- The Importance of Budgets in Financial Planning ClassDocument33 pagesThe Importance of Budgets in Financial Planning ClassMonkey2111No ratings yet

- Summary of Chapter 9 Budget Preparation - Erlinda Katlanis 1081002089Document9 pagesSummary of Chapter 9 Budget Preparation - Erlinda Katlanis 1081002089Linda Katlanis100% (1)

- Budget and BudgetryDocument6 pagesBudget and Budgetryram sagar100% (1)

- Horngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024Document133 pagesHorngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024thomas.casey387100% (21)

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- 4 Profit Planning Budgeting PDFDocument85 pages4 Profit Planning Budgeting PDFNadie LrdNo ratings yet

- Topic 3 Budgetary Process of An OrganisationDocument57 pagesTopic 3 Budgetary Process of An OrganisationMaryam MalieNo ratings yet

- Business Finance For Video Module 2Document16 pagesBusiness Finance For Video Module 2Bai NiloNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Chapter Five - Employee Testing and SelectionDocument23 pagesChapter Five - Employee Testing and Selectionyaxyesahal123No ratings yet

- Chapter 8 Performance Management and Appraisal UpdateDocument17 pagesChapter 8 Performance Management and Appraisal Updateyaxyesahal123No ratings yet

- Chapter Six Interviewing CandidatesDocument16 pagesChapter Six Interviewing Candidatesyaxyesahal123No ratings yet

- DocumentDocument11 pagesDocumentyaxyesahal123No ratings yet

- Ch03 Word 2013Document44 pagesCh03 Word 2013yaxyesahal123No ratings yet

- Area Offices KPIsDocument149 pagesArea Offices KPIsEmmanuel Lucky OhiroNo ratings yet

- RRL and SignificanceDocument5 pagesRRL and SignificanceYas SyNo ratings yet

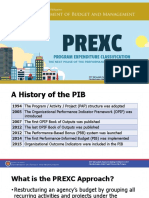

- Program Expenditure Classification PREXCDocument34 pagesProgram Expenditure Classification PREXCMark Lester MundoNo ratings yet

- Marshalling Resources To Support The Strategy Execution EffortDocument6 pagesMarshalling Resources To Support The Strategy Execution EffortCHRISCEL VALIENTENo ratings yet

- Ddo Hand Book PDFDocument159 pagesDdo Hand Book PDFSafdar KhanNo ratings yet

- Proposed Budget September Entire BookDocument643 pagesProposed Budget September Entire BookCircuit MediaNo ratings yet

- Zimbabwe National Water Authority Act, No. 11 of 1998Document20 pagesZimbabwe National Water Authority Act, No. 11 of 1998toga22No ratings yet

- Phys122 Lab 5Document5 pagesPhys122 Lab 5Yeremi Wesly SinagaNo ratings yet

- Non Gov Book QuestionsDocument11 pagesNon Gov Book QuestionsRojille Rye RotorNo ratings yet

- Personal Financial Planning 13th Edition Gitman Test BankDocument32 pagesPersonal Financial Planning 13th Edition Gitman Test BankJeanneRobbinsxwito100% (15)

- AC 203 Final Exam Review WorksheetDocument6 pagesAC 203 Final Exam Review WorksheetLương Thế CườngNo ratings yet

- SAP PS Budget ManagementDocument8 pagesSAP PS Budget ManagementMahendra DahiyaNo ratings yet

- Planning: 1. Short-Term Forecasts. These Are Usually For Periods Up To ThreeDocument31 pagesPlanning: 1. Short-Term Forecasts. These Are Usually For Periods Up To ThreeAnonymous iCvmTVsUtNo ratings yet

- Transmital Letter: Republic of The Philippines Province of Nueva Vizcaya Municipality of AmbaguioDocument12 pagesTransmital Letter: Republic of The Philippines Province of Nueva Vizcaya Municipality of AmbaguioChrisaMae Dagano LitawanNo ratings yet

- Budget and PlanningDocument9 pagesBudget and Planningyes1nthNo ratings yet

- Hca14 - PPT - CH06 Master Budgeting and Responsibility AccountingDocument20 pagesHca14 - PPT - CH06 Master Budgeting and Responsibility AccountingNiizamUddinBhuiyan100% (1)

- Public Financial Management in GhanaDocument6 pagesPublic Financial Management in GhanaKwaku- Tei100% (2)

- Caranglaan SBGRDocument47 pagesCaranglaan SBGRMike GuerzonNo ratings yet

- Group Names: 1. Anisa Ahmed Farah 2. Hanad Bashir Mohamud 3. Ibrahim Hassan Mohamud 4. Kaltuma Abdirashid Ibrahim 5. Mariam Abdiqadir OsmanDocument11 pagesGroup Names: 1. Anisa Ahmed Farah 2. Hanad Bashir Mohamud 3. Ibrahim Hassan Mohamud 4. Kaltuma Abdirashid Ibrahim 5. Mariam Abdiqadir OsmanMohamed HassanNo ratings yet

- Jaipal - Project (1) - 111Document72 pagesJaipal - Project (1) - 111biggbossNo ratings yet

- Major Final OutputsDocument7 pagesMajor Final OutputsEmily BondadNo ratings yet

- KamcoDocument27 pagesKamcoAnn JosephNo ratings yet

- PTCL ReportDocument19 pagesPTCL Reportkashif aliNo ratings yet

- 4upm Zca 649408Document18 pages4upm Zca 649408Adnan LunatNo ratings yet

- Short Term Budgeting HandoutDocument11 pagesShort Term Budgeting HandoutMaurienne MojicaNo ratings yet

- Budgeting WsDocument5 pagesBudgeting Wsapi-290878974No ratings yet

Download as pptx, pdf, or txt

You might also like

- Chapter 13 Budgets and Budgetary ControlDocument47 pagesChapter 13 Budgets and Budgetary ControlAndrew StarkNo ratings yet

- Which Expenses Are Fixed and Which Are Variable? Indicate The Monthly Total. Put A Check Mark On The Corresponding TypeDocument4 pagesWhich Expenses Are Fixed and Which Are Variable? Indicate The Monthly Total. Put A Check Mark On The Corresponding TypeKiem SantosNo ratings yet

- Notes On Cash BudgetDocument26 pagesNotes On Cash BudgetJoshua P.No ratings yet

- Maths Project On Home BudgetDocument21 pagesMaths Project On Home BudgetVidhi Chokhani79% (622)

- TA LectureNote-4Document13 pagesTA LectureNote-4nguyenbachptpNo ratings yet

- Review 20Document4 pagesReview 20StubadubNo ratings yet

- Budget: Definition, Classification and Types of BudgetsDocument15 pagesBudget: Definition, Classification and Types of BudgetsAnderson GuzmanNo ratings yet

- 10) BudgetingDocument5 pages10) BudgetingAlbert Krohn SandahlNo ratings yet

- Chapter 6 BudgetsDocument60 pagesChapter 6 BudgetsSandipan DawnNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- Report No. 6 Batoy Khey Heart N. Matano Naffy BDocument35 pagesReport No. 6 Batoy Khey Heart N. Matano Naffy BCamille EscoteNo ratings yet

- Operational BudgetDocument14 pagesOperational BudgetTsega BirhanuNo ratings yet

- Akmen Bab 8Document3 pagesAkmen Bab 8Hafizh GalihNo ratings yet

- CH - 2 Master Budget - Ahmed With Illustration and SolutionDocument15 pagesCH - 2 Master Budget - Ahmed With Illustration and SolutionYohannes MeridNo ratings yet

- HanduotDocument20 pagesHanduotTegene TesfayeNo ratings yet

- Budgeting Planning and ControlDocument31 pagesBudgeting Planning and Controlintan agustina100% (1)

- Chapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningDocument6 pagesChapter 5: Financial Forecasting, Corporate Planning, and Budgeting Corporate PlanningAdoree RamosNo ratings yet

- Chap04 - Profit PlanningDocument36 pagesChap04 - Profit PlanningChi Nguyễn Thị KimNo ratings yet

- Cost II-Ch - 3 Master BudgetDocument14 pagesCost II-Ch - 3 Master BudgetYitera SisayNo ratings yet

- Module in BudgetingDocument5 pagesModule in BudgetingJade TanNo ratings yet

- Profit PlanningDocument5 pagesProfit PlanningChaudhry Umair YounisNo ratings yet

- Chapter 10Document13 pagesChapter 10Shane Melody G. GetonzoNo ratings yet

- Master BudgetDocument5 pagesMaster BudgetSaranyaa KanagarajNo ratings yet

- CH - 3 Master Budget - With Illustration and SolutionDocument16 pagesCH - 3 Master Budget - With Illustration and SolutionMelat TNo ratings yet

- Session 25 - BudgetingDocument27 pagesSession 25 - BudgetingVinukartik PillaiNo ratings yet

- U02 Budget Methodolgies and Budget PreparationDocument26 pagesU02 Budget Methodolgies and Budget PreparationIslam AhmedNo ratings yet

- Chapter 6Document13 pagesChapter 6yana kiutNo ratings yet

- Moduel 4Document11 pagesModuel 4sarojkumardasbsetNo ratings yet

- Summary Master BudgetingDocument5 pagesSummary Master BudgetingliaNo ratings yet

- CH 2 Cost IIDocument10 pagesCH 2 Cost IIfirewNo ratings yet

- CH7 BudgetingDocument51 pagesCH7 BudgetingYMNo ratings yet

- Chapter 5Document7 pagesChapter 5intelragadio100% (1)

- Chapter 08Document18 pagesChapter 08hana_kimi_91No ratings yet

- Budgeting and Budgetary Control 2019Document10 pagesBudgeting and Budgetary Control 2019Kerrice RobinsonNo ratings yet

- Class 9 - Managerial AccountingDocument12 pagesClass 9 - Managerial AccountingcarlaNo ratings yet

- Master Budgeting OutlineDocument14 pagesMaster Budgeting OutlineGina Mantos GocotanoNo ratings yet

- CHAPTER 3 Financial PlanningDocument7 pagesCHAPTER 3 Financial Planningflorabel parana0% (1)

- Master BudgetingDocument6 pagesMaster BudgetingKrNo ratings yet

- Developing Operating & Capital BudgetingDocument48 pagesDeveloping Operating & Capital Budgetingapi-3742302100% (2)

- Bafinmax CM7Document22 pagesBafinmax CM7Marvin AndresNo ratings yet

- Financial Management Chapter 10Document14 pagesFinancial Management Chapter 10Shane Melody G. GetonzoNo ratings yet

- Lecture 11 BIS ManagerialDocument25 pagesLecture 11 BIS Managerialnada ahmedNo ratings yet

- Profit Planning and BudgetingDocument53 pagesProfit Planning and BudgetingBhey PayumoNo ratings yet

- FM Chapter 10-1Document14 pagesFM Chapter 10-1Shane Melody G. GetonzoNo ratings yet

- CH 9 Profit Planning and Activity-Based BudgetingDocument21 pagesCH 9 Profit Planning and Activity-Based BudgetingIsra' I. SweilehNo ratings yet

- Budgeting P1Document48 pagesBudgeting P1YINGGCHI LONGNo ratings yet

- Managerial Accounting IBPDocument58 pagesManagerial Accounting IBPSaadat Ali100% (1)

- Managerial Accounting Asiacareer College/Cparcenter Operational and Financial Budgeting DWM - Reyno, Cpa, DbaDocument3 pagesManagerial Accounting Asiacareer College/Cparcenter Operational and Financial Budgeting DWM - Reyno, Cpa, DbaCertified Public AccountantNo ratings yet

- Financial Planning and Control ProcessDocument3 pagesFinancial Planning and Control ProcessPRINCESS HONEYLET SIGESMUNDONo ratings yet

- Cost CH 2Document16 pagesCost CH 2Shimelis TesemaNo ratings yet

- Master BudgetDocument6 pagesMaster BudgetPacir QubeNo ratings yet

- Brewer6ce WYRNTK Ch07Document5 pagesBrewer6ce WYRNTK Ch07Bilal ShahidNo ratings yet

- Forecasting or BudgetingDocument6 pagesForecasting or BudgetingHannah Faith BagasaniNo ratings yet

- The Importance of Budgets in Financial Planning ClassDocument33 pagesThe Importance of Budgets in Financial Planning ClassMonkey2111No ratings yet

- Summary of Chapter 9 Budget Preparation - Erlinda Katlanis 1081002089Document9 pagesSummary of Chapter 9 Budget Preparation - Erlinda Katlanis 1081002089Linda Katlanis100% (1)

- Budget and BudgetryDocument6 pagesBudget and Budgetryram sagar100% (1)

- Horngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024Document133 pagesHorngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024thomas.casey387100% (21)

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- 4 Profit Planning Budgeting PDFDocument85 pages4 Profit Planning Budgeting PDFNadie LrdNo ratings yet

- Topic 3 Budgetary Process of An OrganisationDocument57 pagesTopic 3 Budgetary Process of An OrganisationMaryam MalieNo ratings yet

- Business Finance For Video Module 2Document16 pagesBusiness Finance For Video Module 2Bai NiloNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Chapter Five - Employee Testing and SelectionDocument23 pagesChapter Five - Employee Testing and Selectionyaxyesahal123No ratings yet

- Chapter 8 Performance Management and Appraisal UpdateDocument17 pagesChapter 8 Performance Management and Appraisal Updateyaxyesahal123No ratings yet

- Chapter Six Interviewing CandidatesDocument16 pagesChapter Six Interviewing Candidatesyaxyesahal123No ratings yet

- DocumentDocument11 pagesDocumentyaxyesahal123No ratings yet

- Ch03 Word 2013Document44 pagesCh03 Word 2013yaxyesahal123No ratings yet

- Area Offices KPIsDocument149 pagesArea Offices KPIsEmmanuel Lucky OhiroNo ratings yet

- RRL and SignificanceDocument5 pagesRRL and SignificanceYas SyNo ratings yet

- Program Expenditure Classification PREXCDocument34 pagesProgram Expenditure Classification PREXCMark Lester MundoNo ratings yet

- Marshalling Resources To Support The Strategy Execution EffortDocument6 pagesMarshalling Resources To Support The Strategy Execution EffortCHRISCEL VALIENTENo ratings yet

- Ddo Hand Book PDFDocument159 pagesDdo Hand Book PDFSafdar KhanNo ratings yet

- Proposed Budget September Entire BookDocument643 pagesProposed Budget September Entire BookCircuit MediaNo ratings yet

- Zimbabwe National Water Authority Act, No. 11 of 1998Document20 pagesZimbabwe National Water Authority Act, No. 11 of 1998toga22No ratings yet

- Phys122 Lab 5Document5 pagesPhys122 Lab 5Yeremi Wesly SinagaNo ratings yet

- Non Gov Book QuestionsDocument11 pagesNon Gov Book QuestionsRojille Rye RotorNo ratings yet

- Personal Financial Planning 13th Edition Gitman Test BankDocument32 pagesPersonal Financial Planning 13th Edition Gitman Test BankJeanneRobbinsxwito100% (15)

- AC 203 Final Exam Review WorksheetDocument6 pagesAC 203 Final Exam Review WorksheetLương Thế CườngNo ratings yet

- SAP PS Budget ManagementDocument8 pagesSAP PS Budget ManagementMahendra DahiyaNo ratings yet

- Planning: 1. Short-Term Forecasts. These Are Usually For Periods Up To ThreeDocument31 pagesPlanning: 1. Short-Term Forecasts. These Are Usually For Periods Up To ThreeAnonymous iCvmTVsUtNo ratings yet

- Transmital Letter: Republic of The Philippines Province of Nueva Vizcaya Municipality of AmbaguioDocument12 pagesTransmital Letter: Republic of The Philippines Province of Nueva Vizcaya Municipality of AmbaguioChrisaMae Dagano LitawanNo ratings yet

- Budget and PlanningDocument9 pagesBudget and Planningyes1nthNo ratings yet

- Hca14 - PPT - CH06 Master Budgeting and Responsibility AccountingDocument20 pagesHca14 - PPT - CH06 Master Budgeting and Responsibility AccountingNiizamUddinBhuiyan100% (1)

- Public Financial Management in GhanaDocument6 pagesPublic Financial Management in GhanaKwaku- Tei100% (2)

- Caranglaan SBGRDocument47 pagesCaranglaan SBGRMike GuerzonNo ratings yet

- Group Names: 1. Anisa Ahmed Farah 2. Hanad Bashir Mohamud 3. Ibrahim Hassan Mohamud 4. Kaltuma Abdirashid Ibrahim 5. Mariam Abdiqadir OsmanDocument11 pagesGroup Names: 1. Anisa Ahmed Farah 2. Hanad Bashir Mohamud 3. Ibrahim Hassan Mohamud 4. Kaltuma Abdirashid Ibrahim 5. Mariam Abdiqadir OsmanMohamed HassanNo ratings yet

- Jaipal - Project (1) - 111Document72 pagesJaipal - Project (1) - 111biggbossNo ratings yet

- Major Final OutputsDocument7 pagesMajor Final OutputsEmily BondadNo ratings yet

- KamcoDocument27 pagesKamcoAnn JosephNo ratings yet

- PTCL ReportDocument19 pagesPTCL Reportkashif aliNo ratings yet

- 4upm Zca 649408Document18 pages4upm Zca 649408Adnan LunatNo ratings yet

- Short Term Budgeting HandoutDocument11 pagesShort Term Budgeting HandoutMaurienne MojicaNo ratings yet

- Budgeting WsDocument5 pagesBudgeting Wsapi-290878974No ratings yet