Bank Study Case

Bank Study Case

You might also like

- Deluxe SolutionDocument6 pagesDeluxe SolutionR K Patham100% (1)

- Credit Analysis PresentationDocument12 pagesCredit Analysis PresentationSamuel Lewis100% (1)

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument27 pagesSolutions For End-of-Chapter Questions and Problems: Chapter TenSam MNo ratings yet

- Credit Risk ManagementDocument78 pagesCredit Risk ManagementSanjida100% (1)

- Ins-24 Chapter - Wise - Question - Bank2Document181 pagesIns-24 Chapter - Wise - Question - Bank2Shubh100% (2)

- AINS 21 Assignment 9 Insurance PoliciesDocument24 pagesAINS 21 Assignment 9 Insurance PoliciesSiddharth Chakkarwar100% (1)

- Credit Rating in India - JBIMSDocument8 pagesCredit Rating in India - JBIMSSidhi AgarwalNo ratings yet

- Capital Structure and BankruptcyDocument4 pagesCapital Structure and Bankruptcytungeena waseemNo ratings yet

- What Is A Debt RatioDocument11 pagesWhat Is A Debt RatioshreyaNo ratings yet

- Credit Risk PDFDocument28 pagesCredit Risk PDFAnubhav SrivastavaNo ratings yet

- Credit RiskDocument18 pagesCredit Riskyoshiharu.harano1726No ratings yet

- 0036 - Accounting For Business - EditedDocument4 pages0036 - Accounting For Business - EditedAwais AhmedNo ratings yet

- Dhanashree Shirke Credit RatingDocument13 pagesDhanashree Shirke Credit RatingDivya BadbeNo ratings yet

- M-Com Part II Proect: BY Dhanashree Shirke ROLL NO: 4033 Subject: Credit RatingDocument13 pagesM-Com Part II Proect: BY Dhanashree Shirke ROLL NO: 4033 Subject: Credit RatingDivya BadbeNo ratings yet

- Banking Sector AnalysisDocument7 pagesBanking Sector AnalysisKarthikJattiNo ratings yet

- Credit Scoring: Beyond The NumbersDocument34 pagesCredit Scoring: Beyond The NumbersramssravaniNo ratings yet

- FSA Chapter 7Document3 pagesFSA Chapter 7Nadia ZahraNo ratings yet

- Objective of Project ReportDocument16 pagesObjective of Project ReportRobinn TiggaNo ratings yet

- Dai PDFDocument21 pagesDai PDFNinjee BoNo ratings yet

- Credit Analyst Q&ADocument6 pagesCredit Analyst Q&ASudhir PowerNo ratings yet

- Risk Latte - RAROC of A Corporate Loan - "Back of The Envelope" CalculationsDocument3 pagesRisk Latte - RAROC of A Corporate Loan - "Back of The Envelope" CalculationsAshley JomyNo ratings yet

- Financial Statement Analysis-IIDocument45 pagesFinancial Statement Analysis-IINeelisetty Satya SaiNo ratings yet

- Final Project PresentationDocument11 pagesFinal Project PresentationJamalNo ratings yet

- Objective of Project ReportDocument13 pagesObjective of Project ReportPinakisgNo ratings yet

- Analysis of Ratio Bank BcaDocument6 pagesAnalysis of Ratio Bank BcaArya SingaNo ratings yet

- Credit Risk Analysis - Control - GC - 2Document176 pagesCredit Risk Analysis - Control - GC - 2Keith Tanaka MagakaNo ratings yet

- Ratio AnalyDocument19 pagesRatio AnalyNima RockNo ratings yet

- What Affects Your Credit ScoreDocument7 pagesWhat Affects Your Credit ScoreAlpa DwivediNo ratings yet

- What Is RISK Management in Bank?Document10 pagesWhat Is RISK Management in Bank?Antoneth DiazNo ratings yet

- Research Paper On Credit Risk ManagementDocument8 pagesResearch Paper On Credit Risk Managementmpymspvkg100% (1)

- Comparative Analysis of BanksDocument8 pagesComparative Analysis of BanksVanshika KajariaNo ratings yet

- Debt Reckoning: Importance of Looking at DebtDocument3 pagesDebt Reckoning: Importance of Looking at Debthafis82No ratings yet

- 4 Debt ManagementDocument122 pages4 Debt ManagementAquesha TirmiziNo ratings yet

- Group 3 PresentationDocument38 pagesGroup 3 PresentationCherie Soriano AnanayoNo ratings yet

- Dmart AccountsDocument18 pagesDmart AccountsDrishti KataraNo ratings yet

- BANK3011 Workshop Week 6 SolutionsDocument5 pagesBANK3011 Workshop Week 6 SolutionsZahraaNo ratings yet

- CH 7Document12 pagesCH 722011663No ratings yet

- What Is Credit Appraisal?Document4 pagesWhat Is Credit Appraisal?maniyarasanNo ratings yet

- BWBB2013 - Topic 4 Part 2Document11 pagesBWBB2013 - Topic 4 Part 2myteacheroht.managementNo ratings yet

- Capital Structure: Trade-Off Theory: Session IVDocument24 pagesCapital Structure: Trade-Off Theory: Session IVAshutosh KumarNo ratings yet

- Capitalization Vs DCFDocument8 pagesCapitalization Vs DCFprabindraNo ratings yet

- Optimal Financing Mix Iv: Wrapping Up The Cost of Capital ApproachDocument16 pagesOptimal Financing Mix Iv: Wrapping Up The Cost of Capital ApproachAnshik BansalNo ratings yet

- Benos - SME Risk RatingDocument18 pagesBenos - SME Risk Ratingvishwanath180689No ratings yet

- What Debt-to-Equity Ratio Is Common For A BankDocument6 pagesWhat Debt-to-Equity Ratio Is Common For A Bankselozok1No ratings yet

- Appraised Value Is The Financial Worth Placed On A Real Property Based On A Report by An Appraiser, Who Is ADocument4 pagesAppraised Value Is The Financial Worth Placed On A Real Property Based On A Report by An Appraiser, Who Is AMichelle GozonNo ratings yet

- Fina4400 Final ExamDocument3 pagesFina4400 Final ExamBouchraya MilitoNo ratings yet

- What Is Loan-to-Value (LTV) RatioDocument6 pagesWhat Is Loan-to-Value (LTV) RatioJason CarterNo ratings yet

- Ratio AnalysisDocument13 pagesRatio Analysisgn.metheNo ratings yet

- AssignmentDocument5 pagesAssignmentpankajjaiswal60No ratings yet

- Credit Risk Management Dissertation TopicsDocument8 pagesCredit Risk Management Dissertation TopicsBestOnlinePaperWritersUK100% (1)

- Financial Institutions Management - Chap011Document21 pagesFinancial Institutions Management - Chap011sk625218No ratings yet

- Credit Analyst Questions and Answers 1693198236Document9 pagesCredit Analyst Questions and Answers 1693198236hh2rwfs8f5No ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument27 pagesSolutions For End-of-Chapter Questions and Problems: Chapter TenYasser AlmishalNo ratings yet

- Capital StructureDocument21 pagesCapital StructureMadhu Kumari VaswaniNo ratings yet

- Credit Risk ManagementDocument14 pagesCredit Risk ManagementmirgiyoseshboyevNo ratings yet

- Solvency Analysis: Debt To Equity RatioDocument3 pagesSolvency Analysis: Debt To Equity RatiovidyaNo ratings yet

- Credit Management and Credit Risk ManagementDocument23 pagesCredit Management and Credit Risk Managementsagar7No ratings yet

- Credit AppraisalDocument6 pagesCredit Appraisalnhan thanhNo ratings yet

- Loan Delinquency ReportDocument28 pagesLoan Delinquency ReportWenibet SilvanoNo ratings yet

- Credit Score Secrets: Unlocking the Path to Financial HealthFrom EverandCredit Score Secrets: Unlocking the Path to Financial HealthRating: 1 out of 5 stars1/5 (1)

- An Introduction To Mutual Funds: Umair Javed ImamDocument57 pagesAn Introduction To Mutual Funds: Umair Javed Imamapi-2719799150% (2)

- Deposit Scheme Analysis of Exim BankDocument16 pagesDeposit Scheme Analysis of Exim Bankmamun khanNo ratings yet

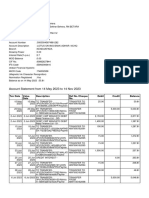

- E StatementDocument2 pagesE StatementS3CH-14 Choy Pak MingNo ratings yet

- Accounting SyllabusDocument16 pagesAccounting SyllabusTarry YzalNo ratings yet

- Working Capital Management Sample ProblemsDocument4 pagesWorking Capital Management Sample ProblemsJames InferidoNo ratings yet

- Rogger Septrya - 2440011362 - TD53-TUTDocument4 pagesRogger Septrya - 2440011362 - TD53-TUTRogger SeptryaNo ratings yet

- Pavan Resume FinalDocument4 pagesPavan Resume FinalDhananjay ShuklaNo ratings yet

- Uhht BG 0 P Il 6 MP 6 GMDocument8 pagesUhht BG 0 P Il 6 MP 6 GMpaappaapNo ratings yet

- Your Easy Health Individual Standard PolicyDocument3 pagesYour Easy Health Individual Standard PolicyMahi MahendranNo ratings yet

- IAS 30 - Disclosures in The Financial Statements of Banks and Similar Financial InstitutionsDocument2 pagesIAS 30 - Disclosures in The Financial Statements of Banks and Similar Financial InstitutionsNadineTicman100% (1)

- Unnumbered - Transaction Flow and Requirement in Opening School Current AccountDocument1 pageUnnumbered - Transaction Flow and Requirement in Opening School Current AccountMC MirandaNo ratings yet

- When Inspiration Does Not Come To Me, I Go Halfway To Meet It. - Sigmund FreudDocument23 pagesWhen Inspiration Does Not Come To Me, I Go Halfway To Meet It. - Sigmund FreudErick OpiyoNo ratings yet

- Financial Management ReviewerDocument57 pagesFinancial Management ReviewerMadelle Q. PradasNo ratings yet

- Research Methodology Microsoft Office Word DocumentDocument35 pagesResearch Methodology Microsoft Office Word DocumentSameer VelaniNo ratings yet

- Time Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th EditionDocument154 pagesTime Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th Editionmohammed alqNo ratings yet

- Cambridge Assessment International Education: Accounting 0452/21 October/November 2017Document9 pagesCambridge Assessment International Education: Accounting 0452/21 October/November 20171234No ratings yet

- Topic 3 - Money - Time Relationships and EquivalenceDocument49 pagesTopic 3 - Money - Time Relationships and EquivalenceMc John PobleteNo ratings yet

- Transactions Download 25-Apr-2024 165608941Document5 pagesTransactions Download 25-Apr-2024 165608941pinkrawpineappleNo ratings yet

- Forensic AuditDocument4 pagesForensic AuditScarlett Singleton RogerNo ratings yet

- Ias 7 Cash Flow Statement ContinuedDocument8 pagesIas 7 Cash Flow Statement ContinuedMichael Bwire100% (1)

- Format of Holding of Specified Securities Network18 Media & Investments LimitedDocument5 pagesFormat of Holding of Specified Securities Network18 Media & Investments LimitedDigvijayNo ratings yet

- Tanggal Uraian Transaksi Nominal Transaksi SaldoDocument3 pagesTanggal Uraian Transaksi Nominal Transaksi SaldoAdryan RasyasznNo ratings yet

- Gr11 Acc P1 (English) November 2019 Marking GuidelinesDocument8 pagesGr11 Acc P1 (English) November 2019 Marking GuidelinesShriddhi MaharajNo ratings yet

- Classic 11 March 2023 To 12 April 2023: Your AccountDocument6 pagesClassic 11 March 2023 To 12 April 2023: Your Accountrig ers100% (1)

- PH 9 HK 2 y 3 GGu 4 ZWLNDocument6 pagesPH 9 HK 2 y 3 GGu 4 ZWLNRanjit BeheraNo ratings yet

- 2022-03-12 MCQs For CSAA Exam PreparationDocument400 pages2022-03-12 MCQs For CSAA Exam PreparationMuhammadNazmushShakibNo ratings yet

- Ifrs 9 QuestionsDocument10 pagesIfrs 9 QuestionsKiri chrisNo ratings yet

- Final Preboard MS ICARE Batch 6Document11 pagesFinal Preboard MS ICARE Batch 6MABI ESPENIDONo ratings yet

Download as pptx, pdf, or txt

You might also like

- Deluxe SolutionDocument6 pagesDeluxe SolutionR K Patham100% (1)

- Credit Analysis PresentationDocument12 pagesCredit Analysis PresentationSamuel Lewis100% (1)

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument27 pagesSolutions For End-of-Chapter Questions and Problems: Chapter TenSam MNo ratings yet

- Credit Risk ManagementDocument78 pagesCredit Risk ManagementSanjida100% (1)

- Ins-24 Chapter - Wise - Question - Bank2Document181 pagesIns-24 Chapter - Wise - Question - Bank2Shubh100% (2)

- AINS 21 Assignment 9 Insurance PoliciesDocument24 pagesAINS 21 Assignment 9 Insurance PoliciesSiddharth Chakkarwar100% (1)

- Credit Rating in India - JBIMSDocument8 pagesCredit Rating in India - JBIMSSidhi AgarwalNo ratings yet

- Capital Structure and BankruptcyDocument4 pagesCapital Structure and Bankruptcytungeena waseemNo ratings yet

- What Is A Debt RatioDocument11 pagesWhat Is A Debt RatioshreyaNo ratings yet

- Credit Risk PDFDocument28 pagesCredit Risk PDFAnubhav SrivastavaNo ratings yet

- Credit RiskDocument18 pagesCredit Riskyoshiharu.harano1726No ratings yet

- 0036 - Accounting For Business - EditedDocument4 pages0036 - Accounting For Business - EditedAwais AhmedNo ratings yet

- Dhanashree Shirke Credit RatingDocument13 pagesDhanashree Shirke Credit RatingDivya BadbeNo ratings yet

- M-Com Part II Proect: BY Dhanashree Shirke ROLL NO: 4033 Subject: Credit RatingDocument13 pagesM-Com Part II Proect: BY Dhanashree Shirke ROLL NO: 4033 Subject: Credit RatingDivya BadbeNo ratings yet

- Banking Sector AnalysisDocument7 pagesBanking Sector AnalysisKarthikJattiNo ratings yet

- Credit Scoring: Beyond The NumbersDocument34 pagesCredit Scoring: Beyond The NumbersramssravaniNo ratings yet

- FSA Chapter 7Document3 pagesFSA Chapter 7Nadia ZahraNo ratings yet

- Objective of Project ReportDocument16 pagesObjective of Project ReportRobinn TiggaNo ratings yet

- Dai PDFDocument21 pagesDai PDFNinjee BoNo ratings yet

- Credit Analyst Q&ADocument6 pagesCredit Analyst Q&ASudhir PowerNo ratings yet

- Risk Latte - RAROC of A Corporate Loan - "Back of The Envelope" CalculationsDocument3 pagesRisk Latte - RAROC of A Corporate Loan - "Back of The Envelope" CalculationsAshley JomyNo ratings yet

- Financial Statement Analysis-IIDocument45 pagesFinancial Statement Analysis-IINeelisetty Satya SaiNo ratings yet

- Final Project PresentationDocument11 pagesFinal Project PresentationJamalNo ratings yet

- Objective of Project ReportDocument13 pagesObjective of Project ReportPinakisgNo ratings yet

- Analysis of Ratio Bank BcaDocument6 pagesAnalysis of Ratio Bank BcaArya SingaNo ratings yet

- Credit Risk Analysis - Control - GC - 2Document176 pagesCredit Risk Analysis - Control - GC - 2Keith Tanaka MagakaNo ratings yet

- Ratio AnalyDocument19 pagesRatio AnalyNima RockNo ratings yet

- What Affects Your Credit ScoreDocument7 pagesWhat Affects Your Credit ScoreAlpa DwivediNo ratings yet

- What Is RISK Management in Bank?Document10 pagesWhat Is RISK Management in Bank?Antoneth DiazNo ratings yet

- Research Paper On Credit Risk ManagementDocument8 pagesResearch Paper On Credit Risk Managementmpymspvkg100% (1)

- Comparative Analysis of BanksDocument8 pagesComparative Analysis of BanksVanshika KajariaNo ratings yet

- Debt Reckoning: Importance of Looking at DebtDocument3 pagesDebt Reckoning: Importance of Looking at Debthafis82No ratings yet

- 4 Debt ManagementDocument122 pages4 Debt ManagementAquesha TirmiziNo ratings yet

- Group 3 PresentationDocument38 pagesGroup 3 PresentationCherie Soriano AnanayoNo ratings yet

- Dmart AccountsDocument18 pagesDmart AccountsDrishti KataraNo ratings yet

- BANK3011 Workshop Week 6 SolutionsDocument5 pagesBANK3011 Workshop Week 6 SolutionsZahraaNo ratings yet

- CH 7Document12 pagesCH 722011663No ratings yet

- What Is Credit Appraisal?Document4 pagesWhat Is Credit Appraisal?maniyarasanNo ratings yet

- BWBB2013 - Topic 4 Part 2Document11 pagesBWBB2013 - Topic 4 Part 2myteacheroht.managementNo ratings yet

- Capital Structure: Trade-Off Theory: Session IVDocument24 pagesCapital Structure: Trade-Off Theory: Session IVAshutosh KumarNo ratings yet

- Capitalization Vs DCFDocument8 pagesCapitalization Vs DCFprabindraNo ratings yet

- Optimal Financing Mix Iv: Wrapping Up The Cost of Capital ApproachDocument16 pagesOptimal Financing Mix Iv: Wrapping Up The Cost of Capital ApproachAnshik BansalNo ratings yet

- Benos - SME Risk RatingDocument18 pagesBenos - SME Risk Ratingvishwanath180689No ratings yet

- What Debt-to-Equity Ratio Is Common For A BankDocument6 pagesWhat Debt-to-Equity Ratio Is Common For A Bankselozok1No ratings yet

- Appraised Value Is The Financial Worth Placed On A Real Property Based On A Report by An Appraiser, Who Is ADocument4 pagesAppraised Value Is The Financial Worth Placed On A Real Property Based On A Report by An Appraiser, Who Is AMichelle GozonNo ratings yet

- Fina4400 Final ExamDocument3 pagesFina4400 Final ExamBouchraya MilitoNo ratings yet

- What Is Loan-to-Value (LTV) RatioDocument6 pagesWhat Is Loan-to-Value (LTV) RatioJason CarterNo ratings yet

- Ratio AnalysisDocument13 pagesRatio Analysisgn.metheNo ratings yet

- AssignmentDocument5 pagesAssignmentpankajjaiswal60No ratings yet

- Credit Risk Management Dissertation TopicsDocument8 pagesCredit Risk Management Dissertation TopicsBestOnlinePaperWritersUK100% (1)

- Financial Institutions Management - Chap011Document21 pagesFinancial Institutions Management - Chap011sk625218No ratings yet

- Credit Analyst Questions and Answers 1693198236Document9 pagesCredit Analyst Questions and Answers 1693198236hh2rwfs8f5No ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument27 pagesSolutions For End-of-Chapter Questions and Problems: Chapter TenYasser AlmishalNo ratings yet

- Capital StructureDocument21 pagesCapital StructureMadhu Kumari VaswaniNo ratings yet

- Credit Risk ManagementDocument14 pagesCredit Risk ManagementmirgiyoseshboyevNo ratings yet

- Solvency Analysis: Debt To Equity RatioDocument3 pagesSolvency Analysis: Debt To Equity RatiovidyaNo ratings yet

- Credit Management and Credit Risk ManagementDocument23 pagesCredit Management and Credit Risk Managementsagar7No ratings yet

- Credit AppraisalDocument6 pagesCredit Appraisalnhan thanhNo ratings yet

- Loan Delinquency ReportDocument28 pagesLoan Delinquency ReportWenibet SilvanoNo ratings yet

- Credit Score Secrets: Unlocking the Path to Financial HealthFrom EverandCredit Score Secrets: Unlocking the Path to Financial HealthRating: 1 out of 5 stars1/5 (1)

- An Introduction To Mutual Funds: Umair Javed ImamDocument57 pagesAn Introduction To Mutual Funds: Umair Javed Imamapi-2719799150% (2)

- Deposit Scheme Analysis of Exim BankDocument16 pagesDeposit Scheme Analysis of Exim Bankmamun khanNo ratings yet

- E StatementDocument2 pagesE StatementS3CH-14 Choy Pak MingNo ratings yet

- Accounting SyllabusDocument16 pagesAccounting SyllabusTarry YzalNo ratings yet

- Working Capital Management Sample ProblemsDocument4 pagesWorking Capital Management Sample ProblemsJames InferidoNo ratings yet

- Rogger Septrya - 2440011362 - TD53-TUTDocument4 pagesRogger Septrya - 2440011362 - TD53-TUTRogger SeptryaNo ratings yet

- Pavan Resume FinalDocument4 pagesPavan Resume FinalDhananjay ShuklaNo ratings yet

- Uhht BG 0 P Il 6 MP 6 GMDocument8 pagesUhht BG 0 P Il 6 MP 6 GMpaappaapNo ratings yet

- Your Easy Health Individual Standard PolicyDocument3 pagesYour Easy Health Individual Standard PolicyMahi MahendranNo ratings yet

- IAS 30 - Disclosures in The Financial Statements of Banks and Similar Financial InstitutionsDocument2 pagesIAS 30 - Disclosures in The Financial Statements of Banks and Similar Financial InstitutionsNadineTicman100% (1)

- Unnumbered - Transaction Flow and Requirement in Opening School Current AccountDocument1 pageUnnumbered - Transaction Flow and Requirement in Opening School Current AccountMC MirandaNo ratings yet

- When Inspiration Does Not Come To Me, I Go Halfway To Meet It. - Sigmund FreudDocument23 pagesWhen Inspiration Does Not Come To Me, I Go Halfway To Meet It. - Sigmund FreudErick OpiyoNo ratings yet

- Financial Management ReviewerDocument57 pagesFinancial Management ReviewerMadelle Q. PradasNo ratings yet

- Research Methodology Microsoft Office Word DocumentDocument35 pagesResearch Methodology Microsoft Office Word DocumentSameer VelaniNo ratings yet

- Time Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th EditionDocument154 pagesTime Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th Editionmohammed alqNo ratings yet

- Cambridge Assessment International Education: Accounting 0452/21 October/November 2017Document9 pagesCambridge Assessment International Education: Accounting 0452/21 October/November 20171234No ratings yet

- Topic 3 - Money - Time Relationships and EquivalenceDocument49 pagesTopic 3 - Money - Time Relationships and EquivalenceMc John PobleteNo ratings yet

- Transactions Download 25-Apr-2024 165608941Document5 pagesTransactions Download 25-Apr-2024 165608941pinkrawpineappleNo ratings yet

- Forensic AuditDocument4 pagesForensic AuditScarlett Singleton RogerNo ratings yet

- Ias 7 Cash Flow Statement ContinuedDocument8 pagesIas 7 Cash Flow Statement ContinuedMichael Bwire100% (1)

- Format of Holding of Specified Securities Network18 Media & Investments LimitedDocument5 pagesFormat of Holding of Specified Securities Network18 Media & Investments LimitedDigvijayNo ratings yet

- Tanggal Uraian Transaksi Nominal Transaksi SaldoDocument3 pagesTanggal Uraian Transaksi Nominal Transaksi SaldoAdryan RasyasznNo ratings yet

- Gr11 Acc P1 (English) November 2019 Marking GuidelinesDocument8 pagesGr11 Acc P1 (English) November 2019 Marking GuidelinesShriddhi MaharajNo ratings yet

- Classic 11 March 2023 To 12 April 2023: Your AccountDocument6 pagesClassic 11 March 2023 To 12 April 2023: Your Accountrig ers100% (1)

- PH 9 HK 2 y 3 GGu 4 ZWLNDocument6 pagesPH 9 HK 2 y 3 GGu 4 ZWLNRanjit BeheraNo ratings yet

- 2022-03-12 MCQs For CSAA Exam PreparationDocument400 pages2022-03-12 MCQs For CSAA Exam PreparationMuhammadNazmushShakibNo ratings yet

- Ifrs 9 QuestionsDocument10 pagesIfrs 9 QuestionsKiri chrisNo ratings yet

- Final Preboard MS ICARE Batch 6Document11 pagesFinal Preboard MS ICARE Batch 6MABI ESPENIDONo ratings yet