Download as ppt, pdf, or txt

You might also like

- 4.1 Note On Developing - Start-Up - StrategiesDocument19 pages4.1 Note On Developing - Start-Up - StrategiesSamarth SharmaNo ratings yet

- 05 2023 Sales Out Report MTDDocument2 pages05 2023 Sales Out Report MTDNOCINPLUSNo ratings yet

- Resumen de Exportaciones No Petroleras Por Destino: Miles Usd Fob / Ton (Ene-Sep)Document1 pageResumen de Exportaciones No Petroleras Por Destino: Miles Usd Fob / Ton (Ene-Sep)Lady SuarezNo ratings yet

- Ενότητα 1.2.2 - Παράδειγμα μοντέλων αποτίμησηςDocument43 pagesΕνότητα 1.2.2 - Παράδειγμα μοντέλων αποτίμησηςagis.condtNo ratings yet

- Anexo 1. Resumen Valorización - Estimaciones BiceDocument1 pageAnexo 1. Resumen Valorización - Estimaciones BiceRicardo CarrilloNo ratings yet

- Investments Problem SetDocument5 pagesInvestments Problem Setzer0fxz8209No ratings yet

- Stock Screener203025Document5 pagesStock Screener203025Sde BdrNo ratings yet

- Bahan Prediksi Closing April 2019-1Document12 pagesBahan Prediksi Closing April 2019-1NazarNo ratings yet

- 2021 OPT - Weight For Length or Height of 0-59 Months Old ChildrenDocument50 pages2021 OPT - Weight For Length or Height of 0-59 Months Old Childrenariza baylosisNo ratings yet

- Summary Mill Cost by StationDocument16 pagesSummary Mill Cost by StationAndreas Eduard LerrickNo ratings yet

- VWQECQWEWQDocument39 pagesVWQECQWEWQEdward Roy “Ying” AyingNo ratings yet

- Equity Valuation: REDS-Research Equity Database System Page 1 of 2Document2 pagesEquity Valuation: REDS-Research Equity Database System Page 1 of 2Ariansyah NobelNo ratings yet

- Feeding Highly Prolific Sows in Hot, Humid Climates: Prof. Dr. Bruno A. N. SilvaDocument76 pagesFeeding Highly Prolific Sows in Hot, Humid Climates: Prof. Dr. Bruno A. N. SilvaThầy QuangNo ratings yet

- Equity Valuation: REDS-Research Equity Database System Page 1 of 2Document2 pagesEquity Valuation: REDS-Research Equity Database System Page 1 of 2Ariansyah NobelNo ratings yet

- Particulars FY15 FY16 FY17 FY18 FY19 RevenueDocument14 pagesParticulars FY15 FY16 FY17 FY18 FY19 RevenueShivang KalraNo ratings yet

- Reporte-1t2023 MagotsabDocument2 pagesReporte-1t2023 MagotsabLuis Walter Hernandez VallejosNo ratings yet

- Roche Group Financial DataDocument43 pagesRoche Group Financial DataDryTvMusicNo ratings yet

- Lampiran Ratio Rujukan Bulan Juni 2023Document7 pagesLampiran Ratio Rujukan Bulan Juni 2023Legolas 001No ratings yet

- 2Q23 Consolidated ChartsDocument26 pages2Q23 Consolidated ChartsSANDRO LUIS GUEVARA CONDENo ratings yet

- Form Chia NSKM Theo % Dong Gop Cua KVDocument1 pageForm Chia NSKM Theo % Dong Gop Cua KVphamhoangdung604No ratings yet

- Review Meeting SpecialtisDocument34 pagesReview Meeting Specialtisdestyana.dindaNo ratings yet

- Informe SBS Asset ManagementDocument32 pagesInforme SBS Asset ManagementyaninaNo ratings yet

- Maruti Suzuki ValuationDocument47 pagesMaruti Suzuki ValuationMradul GautamNo ratings yet

- Symbol Name Current Price 1 Month % CHG 3 Month % CHG 6 Month % CHG 1 Year % CHGDocument12 pagesSymbol Name Current Price 1 Month % CHG 3 Month % CHG 6 Month % CHG 1 Year % CHGAmit AwalNo ratings yet

- Laporan Monitoring Fresh Food Nov 2021Document46 pagesLaporan Monitoring Fresh Food Nov 2021Muh. Ilham NurNo ratings yet

- Moc 2.2018 PP Ops - TNDocument93 pagesMoc 2.2018 PP Ops - TNHaja Mohamed SheriffNo ratings yet

- Daily Market Sheet 1-5-10Document2 pagesDaily Market Sheet 1-5-10chainbridgeinvestingNo ratings yet

- Bronch AdDocument23 pagesBronch AdAbdelrahman NazmiNo ratings yet

- DOMO-Mill Cost Des'21Document20 pagesDOMO-Mill Cost Des'21Andreas Eduard LerrickNo ratings yet

- Data MixmrktDocument9 pagesData MixmrktRavi David UllahNo ratings yet

- Analisa Agen No RepeatDocument1 pageAnalisa Agen No Repeatirfan edisonNo ratings yet

- Business Valuation - ROTIDocument21 pagesBusiness Valuation - ROTITEDY TEDYNo ratings yet

- Fraport Greece - YTD 03 Traffic 2019 Vs 2018Document2 pagesFraport Greece - YTD 03 Traffic 2019 Vs 2018TatianaNo ratings yet

- Krakatau Steel A CaseDocument9 pagesKrakatau Steel A CaseFarhan SoepraptoNo ratings yet

- Fraport Greece YTD 04 Traffic 2019vs2018Document2 pagesFraport Greece YTD 04 Traffic 2019vs2018TatianaNo ratings yet

- Monitoring Cont Struk 1 - 24 May 2023Document41 pagesMonitoring Cont Struk 1 - 24 May 2023Nico BadrisonNo ratings yet

- Monitoring Pps Store 1-14 Agt 23-1Document182 pagesMonitoring Pps Store 1-14 Agt 23-1El FatihNo ratings yet

- RD Release 2Q21 20210810 ENDocument19 pagesRD Release 2Q21 20210810 ENRodrigo FerreiraNo ratings yet

- Preparatory Examination Provincial Results Analysis 2023Document5 pagesPreparatory Examination Provincial Results Analysis 2023Agnes MmathaboNo ratings yet

- Monthly Report - Growth Fund - P - Apr'21Document5 pagesMonthly Report - Growth Fund - P - Apr'21dapen kujangNo ratings yet

- Equity Valuacion (Grupo SBS)Document3 pagesEquity Valuacion (Grupo SBS)Juan José BlesaNo ratings yet

- Daily Market Update 4Document1 pageDaily Market Update 4Towfick KamalNo ratings yet

- Review On Financial Statements: Management Discussion & Analysis Quarter Ended 30 September, 2017Document10 pagesReview On Financial Statements: Management Discussion & Analysis Quarter Ended 30 September, 2017nanda rafsanjaniNo ratings yet

- Buss Plan KPRDocument521 pagesBuss Plan KPRApriadi YusufNo ratings yet

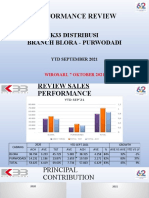

- Performance Review: K33 Distribusi Branch Blora - PurwodadiDocument14 pagesPerformance Review: K33 Distribusi Branch Blora - PurwodadiCipto Saritomo S.PNo ratings yet

- Proposed Target 2016 Revised 2Document12 pagesProposed Target 2016 Revised 2ecalotaNo ratings yet

- 07 - Julio - PatentamientoDocument5 pages07 - Julio - PatentamientoLeonardo PeirettiNo ratings yet

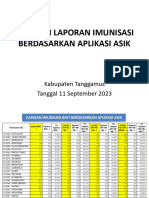

- EVALUASI LAPORAN IMUNISASI ASIK 11 September 2023Document9 pagesEVALUASI LAPORAN IMUNISASI ASIK 11 September 2023Ircham IrchamNo ratings yet

- Equity Valuation: REDS-Research Equity Database System Page 1 of 2Document2 pagesEquity Valuation: REDS-Research Equity Database System Page 1 of 2Ariansyah NobelNo ratings yet

- Rekapitulasi Capaian Bian 24 Agustus 2022Document1 pageRekapitulasi Capaian Bian 24 Agustus 2022Nidya SuarniNo ratings yet

- Airbus ValoDocument19 pagesAirbus ValobendidisalaheddineNo ratings yet

- Nfa Southern Tagalog Region Marketing Operations: April 14, 2020Document13 pagesNfa Southern Tagalog Region Marketing Operations: April 14, 2020Christine MagnayeNo ratings yet

- 10 - 04. PSM 24-31 Okt 2023 - StoreDocument366 pages10 - 04. PSM 24-31 Okt 2023 - StoreRamdi NastiarNo ratings yet

- Daily FNO Overview: Retail ResearchDocument5 pagesDaily FNO Overview: Retail ResearchjaimaaganNo ratings yet

- GridExport December 8 2022 19 20 38Document4 pagesGridExport December 8 2022 19 20 38FBusinessNo ratings yet

- Hitungan ACC 2021 PBUN SalinanDocument6 pagesHitungan ACC 2021 PBUN SalinanFarid Ruskanda BasyarahilNo ratings yet

- Trend Maret 2024Document1 pageTrend Maret 2024Nur FauzanNo ratings yet

- 09 - Septiembre - PatentamientoDocument5 pages09 - Septiembre - PatentamientoLeonardo PeirettiNo ratings yet

- Portfolio SnapshotDocument63 pagesPortfolio Snapshotgurudev21No ratings yet

- Stock Screener203544Document5 pagesStock Screener203544Sde BdrNo ratings yet

- Economic and Financial Analyses of Small and Medium Food Crops Agro-Processing Firms in GhanaFrom EverandEconomic and Financial Analyses of Small and Medium Food Crops Agro-Processing Firms in GhanaNo ratings yet

- Training & Facilitation Workshop - TTT For GSKDocument10 pagesTraining & Facilitation Workshop - TTT For GSKMustafa El mohandesNo ratings yet

- Tax-interviewDocument1 pageTax-interviewMustafa El mohandesNo ratings yet

- Rebutal Letter Mustafa 02.08Document1 pageRebutal Letter Mustafa 02.08Mustafa El mohandesNo ratings yet

- Sy & Leb EtickeDocument2 pagesSy & Leb EtickeMustafa El mohandesNo ratings yet

- Jordan - Org - Chart 17 1 2012Document1 pageJordan - Org - Chart 17 1 2012Mustafa El mohandesNo ratings yet

- 7 Habits For Highly Effective ManagersDocument8 pages7 Habits For Highly Effective ManagersMustafa El mohandesNo ratings yet

- City HospitalDocument3 pagesCity HospitalMustafa El mohandesNo ratings yet

- PDF For Kol InfluenceDocument117 pagesPDF For Kol InfluenceMustafa El mohandesNo ratings yet

- Sales Force Incentives Chem Ever 3Document9 pagesSales Force Incentives Chem Ever 3Mustafa El mohandesNo ratings yet

- Measuring & Evaluating LearningDocument15 pagesMeasuring & Evaluating LearningMustafa El mohandesNo ratings yet

- Abu Dhabi OrganogramDocument1 pageAbu Dhabi OrganogramMustafa El mohandesNo ratings yet

- Wallbreakers 2019Document113 pagesWallbreakers 2019Mustafa El mohandesNo ratings yet

- Acy 231Document4 pagesAcy 231Mustafa El mohandesNo ratings yet

- Emotions & MoodsDocument7 pagesEmotions & MoodsMustafa El mohandesNo ratings yet

- Basma Attallah CV3 PDFDocument1 pageBasma Attallah CV3 PDFMustafa El mohandesNo ratings yet

- MAZE PresentationDocument7 pagesMAZE PresentationMustafa El mohandesNo ratings yet

- Customer-Service-Fundamentals-1214944405396582-8 (2 Files Merged)Document40 pagesCustomer-Service-Fundamentals-1214944405396582-8 (2 Files Merged)Mustafa El mohandesNo ratings yet

- WallbreakersDocument19 pagesWallbreakersMustafa El mohandesNo ratings yet

- Itemized Bill 12-2023Document12 pagesItemized Bill 12-2023Mustafa El mohandesNo ratings yet

- Sneak Peak Into UbcDocument29 pagesSneak Peak Into UbcfacelesswithemiliaNo ratings yet

- Commerce Form4 NotesDocument85 pagesCommerce Form4 Noteskeolopile josephNo ratings yet

- HSBC Ivb VC Term Sheet Guide 2024Document67 pagesHSBC Ivb VC Term Sheet Guide 2024Xie NiyunNo ratings yet

- BSC (Hons) Business Management (: BMP6003 International HRMDocument25 pagesBSC (Hons) Business Management (: BMP6003 International HRMNazmus Sakib RahatNo ratings yet

- CadburyDocument36 pagesCadburymaakanksha12No ratings yet

- Manufacture'S Authorization Form: StampDocument1 pageManufacture'S Authorization Form: StampAhmed GhassanyNo ratings yet

- Andrew Yule & Co. LTD: Board of DirectorsDocument8 pagesAndrew Yule & Co. LTD: Board of Directorsdarth vaderNo ratings yet

- Fundamentals Feasibility StudyDocument78 pagesFundamentals Feasibility StudyMohamed Mubarak100% (4)

- Clothing Store Sales Associate ResumeDocument5 pagesClothing Store Sales Associate Resumefsv5r7a1100% (1)

- HRMT 623 Hamid Kazemi AssignmentDocument14 pagesHRMT 623 Hamid Kazemi AssignmentAvneet Kaur SranNo ratings yet

- Internet MicroenvironmentDocument9 pagesInternet MicroenvironmentAnshuman NarangNo ratings yet

- Mba Employment Report 2014 FinalDocument13 pagesMba Employment Report 2014 Finaladitya taradeNo ratings yet

- Learning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Document13 pagesLearning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Yuri GalloNo ratings yet

- WomansHubMar62020 PDFDocument32 pagesWomansHubMar62020 PDFZainaAdamuNo ratings yet

- Foundation Plan Roof Beam Plan: C D E B A 14.00m C D E B ADocument1 pageFoundation Plan Roof Beam Plan: C D E B A 14.00m C D E B AJohn Carl SalasNo ratings yet

- Varun Manian, MD Radiance Realty, Ranks Among The Top Entrepreneurs in The CountryDocument8 pagesVarun Manian, MD Radiance Realty, Ranks Among The Top Entrepreneurs in The CountryAkansha SinghNo ratings yet

- BL FormatoDocument2 pagesBL FormatoBetsabeth LopezNo ratings yet

- Digital-Skills-Digital-Marketing Certificate of Achievement Oj838x9 PDFDocument2 pagesDigital-Skills-Digital-Marketing Certificate of Achievement Oj838x9 PDFMd.Taharul IslamNo ratings yet

- Onboarding Portal Seller Guide: (Desktop)Document29 pagesOnboarding Portal Seller Guide: (Desktop)Rizka WahyuNo ratings yet

- Module 4. Activity Based Costing (Questions)Document9 pagesModule 4. Activity Based Costing (Questions)Praneeth KNo ratings yet

- Financial Management in The Sport Industry 2nd Brown Solution ManualDocument36 pagesFinancial Management in The Sport Industry 2nd Brown Solution Manualverrugassterrink.08ywf6100% (49)

- Liqudated DDocument24 pagesLiqudated DEbrahim AbdellaNo ratings yet

- Lesson 5: Corporate Social Responsibility Ethics and Social Responsibility Enlightened Self InterestDocument35 pagesLesson 5: Corporate Social Responsibility Ethics and Social Responsibility Enlightened Self InterestLily DaniaNo ratings yet

- Soal Pas Myob Kelas Xii GanjilDocument4 pagesSoal Pas Myob Kelas Xii GanjilLank BpNo ratings yet

- Nike VS AdidasDocument67 pagesNike VS AdidasNitesh Agrawal100% (2)

- Deed-of-Absolute-Sale-TALAKAG - TEODORO AYNONDocument3 pagesDeed-of-Absolute-Sale-TALAKAG - TEODORO AYNONRC Farms TalakagNo ratings yet

- Tutorial CSDocument5 pagesTutorial CSallyaNo ratings yet

- HUB Corruption Ix - Biological, Chemical and Seismic WeaponsDocument56 pagesHUB Corruption Ix - Biological, Chemical and Seismic WeaponsDr Romesh Arya ChakravartiNo ratings yet