Download as pptx, pdf, or txt

You might also like

- p2 - Guerrero Ch15Document27 pagesp2 - Guerrero Ch15JerichoPedragosa83% (12)

- KRA SampleDocument5 pagesKRA Sampleharry22jan100% (2)

- Manual On The Financial Management of BarangaysDocument150 pagesManual On The Financial Management of BarangaysMarcellanne Valles100% (4)

- WCMDocument35 pagesWCMAmit100% (2)

- Variable and Absorption CostingDocument38 pagesVariable and Absorption CostingstarlightNo ratings yet

- Marginal Costing & Absorption CostingDocument56 pagesMarginal Costing & Absorption CostingHoàng Phương ThảoNo ratings yet

- AGA Company Manufactures and Sells A Product ForDocument6 pagesAGA Company Manufactures and Sells A Product ForSeemabians KazmiNo ratings yet

- Harmonizing Your Touchpoints (SD TL) PDFDocument3 pagesHarmonizing Your Touchpoints (SD TL) PDFSy An Nguyen100% (1)

- Overview of Absorption and Variable CostingDocument5 pagesOverview of Absorption and Variable CostingJarrelaine SerranoNo ratings yet

- 1.3 Income Statement and Statement of Comrehensive IncomeDocument20 pages1.3 Income Statement and Statement of Comrehensive IncomeRula Abu NuwarNo ratings yet

- Marginal and Absorption CostingDocument16 pagesMarginal and Absorption CostingRhinosmikeNo ratings yet

- Chapter 7 Joint and By-Product SlidesDocument25 pagesChapter 7 Joint and By-Product SlidesmamitjasNo ratings yet

- A09 Chapter 4 Class Notes 1232Document6 pagesA09 Chapter 4 Class Notes 1232raylannister14No ratings yet

- Absorption Costing GclassDocument4 pagesAbsorption Costing GclassDoromal, Jerome A.No ratings yet

- Fabm2-Module 3 - With ActivitiesDocument6 pagesFabm2-Module 3 - With ActivitiesROWENA MARAMBANo ratings yet

- CHAPTER FOUR Cost and MGMT ACCTDocument12 pagesCHAPTER FOUR Cost and MGMT ACCTFeleke TerefeNo ratings yet

- Module 3 SCMDocument9 pagesModule 3 SCMKhai LaNo ratings yet

- Joint Cost - by ProductDocument15 pagesJoint Cost - by ProductRessa LarasatiNo ratings yet

- Mas-03: Absorption & Variable CostingDocument4 pagesMas-03: Absorption & Variable CostingClint AbenojaNo ratings yet

- 16 Joint Costs and By-ProductsDocument3 pages16 Joint Costs and By-ProductscjccoseNo ratings yet

- STNR DecisionsDocument10 pagesSTNR DecisionsHassan AdamNo ratings yet

- Finals Quiz 2Document6 pagesFinals Quiz 2Sevastian jedd EdicNo ratings yet

- Lesson 3: Statement of Comprehensive IncomeDocument14 pagesLesson 3: Statement of Comprehensive IncomeReymark TalaveraNo ratings yet

- Joint by Products CostingDocument5 pagesJoint by Products CostingJenelyn FloresNo ratings yet

- Module 13 - Breakeven AnalysisDocument9 pagesModule 13 - Breakeven AnalysisGRACE ANN BERGONIONo ratings yet

- Cost-Volume-Profit and Breakeven AnalysisDocument36 pagesCost-Volume-Profit and Breakeven AnalysisJosartNo ratings yet

- Geby Humairah - 200620315 - Akuntansi Biaya 23F - PDFDocument4 pagesGeby Humairah - 200620315 - Akuntansi Biaya 23F - PDFGeby HumairahNo ratings yet

- Break Even - PMDocument7 pagesBreak Even - PMblessedumoh311No ratings yet

- 6 Joint AND By-Product Costing: Lecture Notes - 12/13 Jan 2015Document27 pages6 Joint AND By-Product Costing: Lecture Notes - 12/13 Jan 2015XNo ratings yet

- CMA CU - Chap 6Document24 pagesCMA CU - Chap 6TAMANNANo ratings yet

- 3MA 03 Absortion and Variable CostingDocument3 pages3MA 03 Absortion and Variable CostingAbigail Regondola BonitaNo ratings yet

- Absorption and Variable Costing, and Inventory Management: Discussion QuestionsDocument28 pagesAbsorption and Variable Costing, and Inventory Management: Discussion QuestionsParth GandhiNo ratings yet

- Relevant Costing or Incremental AnalysisDocument48 pagesRelevant Costing or Incremental Analysis06162kNo ratings yet

- Absorption and Variable CostingDocument5 pagesAbsorption and Variable CostingKIM RAGANo ratings yet

- Short-Term Business DecisionsDocument15 pagesShort-Term Business DecisionsZiad NehadNo ratings yet

- Mas Preweek Hndouts Batch 92Document26 pagesMas Preweek Hndouts Batch 92Mark Anthony CasupangNo ratings yet

- Explain The Difference Between Variable and Absorption CostingDocument8 pagesExplain The Difference Between Variable and Absorption CostingJc QuismundoNo ratings yet

- Team Work Makes The Dream Work Acctg15 Var. Absorption CostingDocument4 pagesTeam Work Makes The Dream Work Acctg15 Var. Absorption Costinggeorgia cerezoNo ratings yet

- Fabm2 Mod3Document10 pagesFabm2 Mod3Margaret Pagdilao MaliksiNo ratings yet

- Cost - Direct Costing, CVP AnalysisDocument7 pagesCost - Direct Costing, CVP AnalysisAriMurdiyantoNo ratings yet

- Examination Answer Booklet: To Be Filled by Student Before Completing The Examination STUDENT ID NUMBER 120-634 .Document26 pagesExamination Answer Booklet: To Be Filled by Student Before Completing The Examination STUDENT ID NUMBER 120-634 .Shaxle Shiiraar shaxleNo ratings yet

- Chapter 8 SolutionsDocument37 pagesChapter 8 SolutionsMasha LankNo ratings yet

- Ebook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFDocument51 pagesEbook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFxaviaalexandrawp86i100% (14)

- Contribution Approach 2Document16 pagesContribution Approach 2kualler80% (5)

- Ca 1 Costing TechniquesDocument6 pagesCa 1 Costing TechniquesORIYOMI KASALINo ratings yet

- Variable Costing vs. Absorption CostingDocument7 pagesVariable Costing vs. Absorption CostingGêmTürÏngånÖNo ratings yet

- Unit 7: Joint and By-Product Costing SystemDocument8 pagesUnit 7: Joint and By-Product Costing SystemCielo PulmaNo ratings yet

- Lecture Notes: Afar G/N/E de Leon 2813-Joint and by Product Costing MAY 2020Document4 pagesLecture Notes: Afar G/N/E de Leon 2813-Joint and by Product Costing MAY 2020May Grethel Joy PeranteNo ratings yet

- Reviewer in BFDocument2 pagesReviewer in BFFelicity EspinosaNo ratings yet

- Management Accounting NotesDocument212 pagesManagement Accounting NotesFrank Chinguwo100% (1)

- Variable Costing: A Decision-Making Perspective: True-False StatementsDocument8 pagesVariable Costing: A Decision-Making Perspective: True-False StatementsJanina Marie GarciaNo ratings yet

- Wahyudi 29123005 Case6 Syndicate1 YP69BDocument5 pagesWahyudi 29123005 Case6 Syndicate1 YP69Bwahyudimba69No ratings yet

- Absorption & Variable CostingDocument21 pagesAbsorption & Variable CostingHamnahariyatiNo ratings yet

- Contribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is ADocument7 pagesContribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is AEVELYN ROSE MOGAONo ratings yet

- Pricing Products and Services: Per Unit TotalDocument3 pagesPricing Products and Services: Per Unit TotalSherwin Francis MendozaNo ratings yet

- p2 Guerrero Ch15Document27 pagesp2 Guerrero Ch15Michael Brian TorresNo ratings yet

- Joint, Standard, ABCDocument10 pagesJoint, Standard, ABCXairah Kriselle de Ocampo50% (2)

- Statement of Comprehensive Income: Intended Learning OutcomesDocument18 pagesStatement of Comprehensive Income: Intended Learning OutcomesJmaseNo ratings yet

- CH 3Document17 pagesCH 3trishanjaliNo ratings yet

- Week 2 - Sept 12-16, 2022 - AcctgDocument9 pagesWeek 2 - Sept 12-16, 2022 - Acctgmaria teresa aparreNo ratings yet

- Joint Product L7 UpdatedDocument14 pagesJoint Product L7 Updatedviony catelinaNo ratings yet

- Quiz 2Document4 pagesQuiz 2Kathleen CusipagNo ratings yet

- Report 2 - Management Accounting (Reworked)Document11 pagesReport 2 - Management Accounting (Reworked)Янислав БорисовNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Production Planning & Control: Syllabus ContentsDocument10 pagesProduction Planning & Control: Syllabus ContentsShivani SharmaNo ratings yet

- International Journal of Research Publications Volume-69, Issue-1, January 2021Document29 pagesInternational Journal of Research Publications Volume-69, Issue-1, January 2021Thomas EsguerraNo ratings yet

- Franchise Package 2020Document18 pagesFranchise Package 2020Edwin CharlesNo ratings yet

- Accounting Assignment 6Document2 pagesAccounting Assignment 6Nahid HawkNo ratings yet

- Premium CH 16 Monopolistic CompetitionDocument24 pagesPremium CH 16 Monopolistic Competitionpranitis gnNo ratings yet

- Transformation With A Capital TDocument130 pagesTransformation With A Capital TAnsgar SkauNo ratings yet

- USA Today - Pursuing The Network Strategy (HBS 402-010) Ch07Document9 pagesUSA Today - Pursuing The Network Strategy (HBS 402-010) Ch07Chan TkfcNo ratings yet

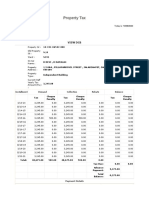

- House Tax ReceiptDocument2 pagesHouse Tax ReceiptAkshaya Raman RamNo ratings yet

- Test Bank PDFDocument9 pagesTest Bank PDFVickesh MalkaniNo ratings yet

- Miracle Fruit Q1Document2 pagesMiracle Fruit Q1hyunsuk fhebieNo ratings yet

- 18 Risk ManagementDocument28 pages18 Risk ManagementReyansh SharmaNo ratings yet

- Debt FinancingDocument2 pagesDebt FinancingjointariqaslamNo ratings yet

- Adam Smith - The Wealth of Nations Book I, Chapter 1. "Of The Division of Labour"Document7 pagesAdam Smith - The Wealth of Nations Book I, Chapter 1. "Of The Division of Labour"JessicaNo ratings yet

- Cost DriversDocument4 pagesCost DriversOlubukola Akintunde100% (1)

- 2018 PNB Paribas - Exane - Retail - Final PDFDocument23 pages2018 PNB Paribas - Exane - Retail - Final PDFRafael VielmaNo ratings yet

- Amsdeer Corporation: Abhishek KumarDocument14 pagesAmsdeer Corporation: Abhishek KumarAbhishek_Kumar_2594100% (1)

- Nokia - Company ProfileDocument53 pagesNokia - Company ProfileNitinAgnihotriNo ratings yet

- Lovelock PPT Chapter 05Document27 pagesLovelock PPT Chapter 05Darshan ParameshNo ratings yet

- Asm2 - 2:11:2020Document45 pagesAsm2 - 2:11:2020Le Tran Uyen Thao (FGW HCM)No ratings yet

- Kpi Planner PDFDocument3 pagesKpi Planner PDFtarrteaNo ratings yet

- The Enterprise Development Programme Annual Review 2012Document29 pagesThe Enterprise Development Programme Annual Review 2012OxfamNo ratings yet

- Section 8 of Unclaimed Moneys Act 1965Document3 pagesSection 8 of Unclaimed Moneys Act 1965Syazwani RazakNo ratings yet

- Strategic ManagementDocument8 pagesStrategic ManagementPulkit GargNo ratings yet

- Lecture 13 Financial Planning 709 12Document34 pagesLecture 13 Financial Planning 709 12bakerNo ratings yet

- Agricultural Marketing Environment in AssamDocument7 pagesAgricultural Marketing Environment in AssamobijitNo ratings yet