Download as pptx, pdf, or txt

You might also like

- Unit 8Document17 pagesUnit 8sheetal gudseNo ratings yet

- CO Exam FinalDocument19 pagesCO Exam Finalpratiksha100% (1)

- FSDocument11 pagesFSKarlo D. Recla100% (1)

- Chapter 3 Vertical & Horizontal AnalysisDocument21 pagesChapter 3 Vertical & Horizontal AnalysisWijdan Saleem EdwanNo ratings yet

- Accounting 9th Edition Horngren Solution ManualDocument206 pagesAccounting 9th Edition Horngren Solution ManualAsa100% (1)

- 2009 United FootballDocument22 pages2009 United Footballdeanmx64220% (1)

- Financial Statement Analysis CompleteDocument10 pagesFinancial Statement Analysis CompletePrerana SharmaNo ratings yet

- 02 Financial Statements AnalysisDocument44 pages02 Financial Statements AnalysisalecksgodinezNo ratings yet

- Topic 4 Overview of Analysis TechniquesDocument37 pagesTopic 4 Overview of Analysis TechniquesSir FELSIRXNNo ratings yet

- Aanalysis of FSDocument2 pagesAanalysis of FStharani1771_32442248No ratings yet

- Bafinmax Topic 2Document109 pagesBafinmax Topic 2airwaller rNo ratings yet

- CMA Exam Review - Part 2 - Section A - Financial Statement AnalysisDocument7 pagesCMA Exam Review - Part 2 - Section A - Financial Statement Analysisaiza eroyNo ratings yet

- Financial Statement AnalysisDocument72 pagesFinancial Statement Analysis88ak07No ratings yet

- Analysis F S: Inancial TatementsDocument39 pagesAnalysis F S: Inancial TatementsRaven Dumlao OllerNo ratings yet

- Financial Statement AnalysisDocument30 pagesFinancial Statement AnalysisSAKET MORENo ratings yet

- Financial Management HandoutDocument26 pagesFinancial Management HandoutCarl Yry BitzNo ratings yet

- Financial Management HandoutDocument26 pagesFinancial Management HandoutCarl Yry BitzNo ratings yet

- FM Chapter 2Document16 pagesFM Chapter 2mearghaile4No ratings yet

- Chap 014Document73 pagesChap 014rikitagujralNo ratings yet

- Ch-2 Financial Analysis &planningDocument27 pagesCh-2 Financial Analysis &planningMulatu LombamoNo ratings yet

- Nalysis ND Nterpretation F Inancial Tatements - : Taskin ShakibDocument40 pagesNalysis ND Nterpretation F Inancial Tatements - : Taskin ShakibSadia RahmanNo ratings yet

- Financial Statement and Its AnalysisDocument67 pagesFinancial Statement and Its AnalysisFahim MahmudNo ratings yet

- Analysis and Interpretation of Financial Statements (Accounting)Document10 pagesAnalysis and Interpretation of Financial Statements (Accounting)aenNo ratings yet

- Project On Financial Management (Cost of Captial & Leverage)Document10 pagesProject On Financial Management (Cost of Captial & Leverage)Royal ProjectsNo ratings yet

- Financial Statement AnalysisDocument50 pagesFinancial Statement AnalysisNouf ANo ratings yet

- 4 Financial Statements Analysis IntepretationDocument77 pages4 Financial Statements Analysis IntepretationAkwasi Boateng100% (2)

- Chapter 2 - Financial Analysis (S202.)Document33 pagesChapter 2 - Financial Analysis (S202.)ha.nguyensanasNo ratings yet

- Analysis of Fianacial Statements-9Document25 pagesAnalysis of Fianacial Statements-9rohitsf22 olypm100% (1)

- Week 2 Part 1 BF Financial Statement Analysis and Financial RatiosDocument5 pagesWeek 2 Part 1 BF Financial Statement Analysis and Financial RatiosAraceli PonterosNo ratings yet

- Instructions For Completing CBA Calculations:: Conventions Used in The Cost Benefit Analysis (CBA) ToolkitDocument5 pagesInstructions For Completing CBA Calculations:: Conventions Used in The Cost Benefit Analysis (CBA) ToolkitSwamynathan SubramanianNo ratings yet

- Financial Accounting Fundamentals: John J. Wild 2009 EditionDocument57 pagesFinancial Accounting Fundamentals: John J. Wild 2009 EditionMariamiNo ratings yet

- 2022 Li FraDocument142 pages2022 Li Fraayush4shekharNo ratings yet

- 3 Cash Flows and Financial AnalysisDocument29 pages3 Cash Flows and Financial AnalysisMarlon LadesmaNo ratings yet

- LEVERAGEDocument19 pagesLEVERAGEraka1010100% (10)

- CBSE Class 12 Acc Notes Tools For Financial Statement AnalysisDocument17 pagesCBSE Class 12 Acc Notes Tools For Financial Statement AnalysisManthanNo ratings yet

- MA Project - F-1Document28 pagesMA Project - F-1jay bapodaraNo ratings yet

- Xamination Questions: Mark QuestionDocument12 pagesXamination Questions: Mark QuestionHarsahib SinghNo ratings yet

- Cashflow State Met TemplateDocument4 pagesCashflow State Met TemplateUnichip PakistanNo ratings yet

- AFS12 Pages 20 24,32 38Document12 pagesAFS12 Pages 20 24,32 38Aishwarya MaradapuNo ratings yet

- Introduction To Accounting Preparing For A User's PerspectiveDocument30 pagesIntroduction To Accounting Preparing For A User's Perspectiverochelle regenciaNo ratings yet

- K-L Fashions Financials Statements, 1990-1991Document11 pagesK-L Fashions Financials Statements, 1990-1991HeidiNo ratings yet

- Accounts Unit 01Document5 pagesAccounts Unit 01Sana JKNo ratings yet

- MCQ of LEVERAGE PDFDocument4 pagesMCQ of LEVERAGE PDFMD Shuhel Ahmed80% (5)

- Horizontal and VerticalDocument53 pagesHorizontal and Verticalmushiechan888No ratings yet

- Financial Ratio Analyses and Their Implications To ManagementDocument46 pagesFinancial Ratio Analyses and Their Implications To ManagementPrinsesa EsguerraNo ratings yet

- Fundflow and CashflowDocument10 pagesFundflow and CashflowmaraiaNo ratings yet

- Acc CH1Document5 pagesAcc CH1Trickster TwelveNo ratings yet

- BEGA ELECTROMOTOR SA Financial Condition Analysis PDFDocument16 pagesBEGA ELECTROMOTOR SA Financial Condition Analysis PDFVirgo AeliusNo ratings yet

- Ms9107a - Financial Statements AnalysisDocument7 pagesMs9107a - Financial Statements AnalysisCelestaire LeeNo ratings yet

- Inancing Ecisions Everages: Learning OutcomesDocument35 pagesInancing Ecisions Everages: Learning OutcomesBhai LangurNo ratings yet

- BF305 Week 8Document26 pagesBF305 Week 8tirigotu57No ratings yet

- Lecture Guide No. 2 AE19.ChuaDocument5 pagesLecture Guide No. 2 AE19.ChuaJonellNo ratings yet

- 4 BielikDocument7 pages4 BielikdainesecowboyNo ratings yet

- Credit Evaluation ProcessDocument73 pagesCredit Evaluation ProcessNeeRaz Kunwar100% (2)

- Unit - II - Analysis of Financial StatementsDocument54 pagesUnit - II - Analysis of Financial StatementsPRERNA PANDEY100% (1)

- Unit - II - Analysis of Financial StatementsDocument54 pagesUnit - II - Analysis of Financial StatementsPRERNA PANDEYNo ratings yet

- Financial Statement AnalysisDocument34 pagesFinancial Statement AnalysisanshumanNo ratings yet

- 2019 - Financial Statement Analysis PDFDocument26 pages2019 - Financial Statement Analysis PDFSurya PrakashNo ratings yet

- 2257 SheetDocument2 pages2257 Sheetev.smith850No ratings yet

- Jan11 IntroDocument29 pagesJan11 IntroteyudersNo ratings yet

- Debt Interest Expense Substantive AnalyticalDocument2 pagesDebt Interest Expense Substantive AnalyticalErik RodriguesNo ratings yet

- RatiosDocument26 pagesRatiosKevin Alexander Escobar MontoyaNo ratings yet

- DAFARMCO Loan Application FormDocument6 pagesDAFARMCO Loan Application Formcarlos-tulali-1309No ratings yet

- ++ Goat - Farming - Record - KeepingDocument32 pages++ Goat - Farming - Record - KeepingAbigail Kaunda SoviNo ratings yet

- Vitrox q22015Document12 pagesVitrox q22015Dennis AngNo ratings yet

- 12 AUTO Budgeting and ProgrammingDocument14 pages12 AUTO Budgeting and ProgrammingJim YauNo ratings yet

- PICPA Income Tax Pas Tax2Document175 pagesPICPA Income Tax Pas Tax2jennyMBNo ratings yet

- ACCG41 Accounting Concepts. Accruals Prepayments Practice QuestionsDocument3 pagesACCG41 Accounting Concepts. Accruals Prepayments Practice QuestionsNauman HashmiNo ratings yet

- Cellular Lightweight Concrete BlocksDocument71 pagesCellular Lightweight Concrete BlocksRavi Kumar Mogilsetti100% (1)

- Government GrantDocument3 pagesGovernment GrantGerlie OpinionNo ratings yet

- C.M.A One Word ReferenceDocument6 pagesC.M.A One Word ReferenceABDUL JALEELNo ratings yet

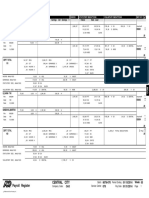

- Payroll Register PD01-31-14 PDFDocument30 pagesPayroll Register PD01-31-14 PDFJoseph ManriquezNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesDyenNo ratings yet

- Act110 Activity 9Document7 pagesAct110 Activity 9Kilwa DyNo ratings yet

- Paper-12: Management Accounting Suggested Answers Section - ADocument5 pagesPaper-12: Management Accounting Suggested Answers Section - AQuestion BankNo ratings yet

- Lesson No. 3: Cities of Mandaluyong and PasigDocument37 pagesLesson No. 3: Cities of Mandaluyong and PasigRenelle Habac100% (1)

- Pooja Singh AssignmentDocument5 pagesPooja Singh Assignmentraj vardhan agarwalNo ratings yet

- Equipment Cash Interest Rent Equity Asset Asset Liability Expense Expense Asset Asset Share Capital Bank Loan Prepaid Rent Remaining SupplyDocument8 pagesEquipment Cash Interest Rent Equity Asset Asset Liability Expense Expense Asset Asset Share Capital Bank Loan Prepaid Rent Remaining SupplyManikangkana BaishyaNo ratings yet

- Observation of Financial Management in Senior High Schools in The Ashanti RegionDocument35 pagesObservation of Financial Management in Senior High Schools in The Ashanti RegionBernard ObengNo ratings yet

- Additional - Chapter 13Document12 pagesAdditional - Chapter 13Gega XachidENo ratings yet

- A Textbook of Refrigeration and Air Conditioning by R S Khurmi and J K GuptaDocument2 pagesA Textbook of Refrigeration and Air Conditioning by R S Khurmi and J K GuptaA's Power100% (2)

- CH 14Document35 pagesCH 14Leila50% (2)

- Lecture15 - Error CorrectionDocument2 pagesLecture15 - Error Correctionjsus22No ratings yet

- Tax CPAR Final Pre Board2Document5 pagesTax CPAR Final Pre Board2No Longer Existing67% (3)

- RCF Ratio AnlysisDocument46 pagesRCF Ratio AnlysisAnil KoliNo ratings yet

- Parcial Balotario 2Document91 pagesParcial Balotario 2Carla ArecheNo ratings yet

- N-Q.1, N Q.3, A-Ced.1, A-Rei.4, F-If.2, F-BF.2, F Le.2, G-SRT.8Document20 pagesN-Q.1, N Q.3, A-Ced.1, A-Rei.4, F-If.2, F-BF.2, F Le.2, G-SRT.8mrsmassieNo ratings yet

- NSC Accounting Grade 12 May June 2023 P1 and MemoDocument32 pagesNSC Accounting Grade 12 May June 2023 P1 and Memozondoowethu5No ratings yet

- Finance Guidelines Manual For Local Departments of Social Services - VA DSS - Oct 2009Document426 pagesFinance Guidelines Manual For Local Departments of Social Services - VA DSS - Oct 2009Rick ThomaNo ratings yet