Download as pptx, pdf, or txt

You might also like

- PACC Offshore Services IPO ProspectusDocument516 pagesPACC Offshore Services IPO ProspectusJame ColesNo ratings yet

- Real Estate - BP SampleDocument33 pagesReal Estate - BP SamplePro Business Plans100% (2)

- Green Bond Principles June 2022 280622Document10 pagesGreen Bond Principles June 2022 280622Jor LinaNo ratings yet

- Green Bond PrinciplesDocument10 pagesGreen Bond Principlesyoussefsultan511No ratings yet

- Green Bond Principles: June 2021Document10 pagesGreen Bond Principles: June 2021varatharajan KaliyaperumalNo ratings yet

- 2022 Wrap-Up On ESG ReportingDocument5 pages2022 Wrap-Up On ESG ReportingMNo ratings yet

- Esg From Europe ComissionDocument140 pagesEsg From Europe ComissionNicole Arnaud de AguiarNo ratings yet

- MFF 2021-2027 FactsheetDocument3 pagesMFF 2021-2027 FactsheetKristīne Garrido - BogdanovičaNo ratings yet

- In The Loop - Make No Mistake Global ESG Regulations Will Impact US CompaniesDocument5 pagesIn The Loop - Make No Mistake Global ESG Regulations Will Impact US CompaniesAnthony ChanNo ratings yet

- The Ripple Effect of EU Disclosures Regulation in Financial Services SectorDocument7 pagesThe Ripple Effect of EU Disclosures Regulation in Financial Services SectorBOHR International Journal of Business Ethics and Corporate GovernanceNo ratings yet

- Session3 Regulation and Disclosure FT24Document45 pagesSession3 Regulation and Disclosure FT24PGNo ratings yet

- #Buildinglife: Eu Policy Whole Life Carbon RoadmapDocument42 pages#Buildinglife: Eu Policy Whole Life Carbon Roadmapdreamtheater666No ratings yet

- Green Bonds 2Document11 pagesGreen Bonds 2Chahine BergaouiNo ratings yet

- SWD 2022 442 F1 Staff Working Paper en V4 P1 2417689Document41 pagesSWD 2022 442 F1 Staff Working Paper en V4 P1 2417689jhaslamNo ratings yet

- Sgs KN Esg White Paper enDocument16 pagesSgs KN Esg White Paper enfahad aliNo ratings yet

- ST 5465 2023 INIT - enDocument5 pagesST 5465 2023 INIT - enaiNo ratings yet

- Deutsche Bank Green Financing FrameworkDocument9 pagesDeutsche Bank Green Financing FrameworkFelixNo ratings yet

- Green Bond: A Systematic Literature Review For Future Research AgendasDocument29 pagesGreen Bond: A Systematic Literature Review For Future Research AgendasGayathri SNo ratings yet

- WBCSD Circular Economy Action Plan 2020-Summary For BusinessDocument24 pagesWBCSD Circular Economy Action Plan 2020-Summary For BusinessNatalia Valero JimenezNo ratings yet

- Sustainable Finance Faqs: Esg, Climate Regulation and DisclosureDocument22 pagesSustainable Finance Faqs: Esg, Climate Regulation and DisclosureFrancesco CistarillNo ratings yet

- Communicating and Raising Eu Visibility Guidance For External Actions July 2022 - en - 0Document25 pagesCommunicating and Raising Eu Visibility Guidance For External Actions July 2022 - en - 0Marija ZivkovicNo ratings yet

- Communicating and Raising EU Visibility - Guidance For External Actions - July 2022 - 0Document25 pagesCommunicating and Raising EU Visibility - Guidance For External Actions - July 2022 - 0Alecos KelemenisNo ratings yet

- Colombia Uk Pact Call For Expressions of Interest PDFDocument45 pagesColombia Uk Pact Call For Expressions of Interest PDFAlberto CastellanosNo ratings yet

- 17507IIEDDocument115 pages17507IIEDFerdee FerdNo ratings yet

- TPT Implementation Guidance 1Document64 pagesTPT Implementation Guidance 1rustam.shah247No ratings yet

- 5A. Loan Markets Association Green Bonds Principles June 2018 270520Document8 pages5A. Loan Markets Association Green Bonds Principles June 2018 270520sdfgvbnhjvNo ratings yet

- Triodos Bank Eu Taxonomy Reporting Methodology Fy2022Document12 pagesTriodos Bank Eu Taxonomy Reporting Methodology Fy2022RaghunathNo ratings yet

- REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL - Brussels, 22.2.2023 COM (2023) 93 FinalDocument12 pagesREPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL - Brussels, 22.2.2023 COM (2023) 93 Finalfds87No ratings yet

- About Green BondsDocument6 pagesAbout Green BondsAditya GuptaNo ratings yet

- Policy Trends in Environmental Due DiligenceDocument6 pagesPolicy Trends in Environmental Due DiligenceAdel EdjarNo ratings yet

- HydrogenDocument39 pagesHydrogenVishesh DwivediNo ratings yet

- 36-Enablon & WK - IB - What To Expect Under The New Corporate Sustainability Reporting Directive - 2022Document6 pages36-Enablon & WK - IB - What To Expect Under The New Corporate Sustainability Reporting Directive - 2022huss fuzzNo ratings yet

- The EU Green Deal - How Will It Impact My Business - CBIDocument35 pagesThe EU Green Deal - How Will It Impact My Business - CBIltmd124bmtNo ratings yet

- Protocol Ares (2016) 5840668-101016Document52 pagesProtocol Ares (2016) 5840668-101016SyaNo ratings yet

- Wa0107.Document28 pagesWa0107.hafidah Nur EpsteinniaNo ratings yet

- Call For Advice To The European Banking Authority On Green Loans and MortgagesDocument7 pagesCall For Advice To The European Banking Authority On Green Loans and Mortgageskarim tarekNo ratings yet

- D3.4 - Technical-Economic Analysis For Determining The Feasibility Threshold For Tradable Biomethane CertificatesDocument24 pagesD3.4 - Technical-Economic Analysis For Determining The Feasibility Threshold For Tradable Biomethane CertificatesCalcRodVerNo ratings yet

- Standarized Natural Capital Management AccountingDocument88 pagesStandarized Natural Capital Management AccountingEdwin Dario Rayo PlazasNo ratings yet

- Pas 2050Document43 pagesPas 2050Pili ESNo ratings yet

- CBI Transport Criteria Document - Apr2021Document24 pagesCBI Transport Criteria Document - Apr2021GamachuNo ratings yet

- Epec Guidance On Energy Efficiency in Public Buildings enDocument64 pagesEpec Guidance On Energy Efficiency in Public Buildings enNicolas HerriauNo ratings yet

- Update of The Zero Draft of The Post-2020 Global Biodiversity FrameworkDocument9 pagesUpdate of The Zero Draft of The Post-2020 Global Biodiversity FrameworkAdi PurnomoNo ratings yet

- Clean Development Mechanism-ScribdDocument26 pagesClean Development Mechanism-ScribdSam KurianNo ratings yet

- Introducing CertifHy - Wouter-Vanhoudt-panel-231115Document13 pagesIntroducing CertifHy - Wouter-Vanhoudt-panel-231115M SidinaNo ratings yet

- GreenFinancingFramework 2021Document29 pagesGreenFinancingFramework 2021Mehul SarkarNo ratings yet

- BGKF TheoryDocument10 pagesBGKF Theoryindra lukmanNo ratings yet

- Cbeju Awp 2024 AmendedDocument134 pagesCbeju Awp 2024 AmendedAnwar TemamNo ratings yet

- Anastasia Guha Director, Northern Europe and MEA Principles For Responsible InvestmentDocument9 pagesAnastasia Guha Director, Northern Europe and MEA Principles For Responsible InvestmentSid KaulNo ratings yet

- BRAUN, FATER, HANDELSONDERNEMING VLAMINGS BV, PG, PG, PGI, PG-B, PGBS, PGUK, PROCTER AND GAMBLE PO MERGED (Merged) ReportDocument13 pagesBRAUN, FATER, HANDELSONDERNEMING VLAMINGS BV, PG, PG, PGI, PG-B, PGBS, PGUK, PROCTER AND GAMBLE PO MERGED (Merged) Reportgallego7719No ratings yet

- Inception Impact Assessment: T L DGDocument5 pagesInception Impact Assessment: T L DGWinnie NatchaNo ratings yet

- Plenaryaddress4-Ms - Sibylleweiler 99351200Document13 pagesPlenaryaddress4-Ms - Sibylleweiler 99351200Hanh HoangNo ratings yet

- LoanlyPlanet - 2019.09Document4 pagesLoanlyPlanet - 2019.09karlng167No ratings yet

- Oj C 2022 206a Full en TXTDocument20 pagesOj C 2022 206a Full en TXTTiberiu PopaNo ratings yet

- PIF Green Bond Impact AssessmentDocument33 pagesPIF Green Bond Impact AssessmentMohamed ZaidiNo ratings yet

- Code of Good Practice For Product GreenhouseDocument24 pagesCode of Good Practice For Product Greenhouseravee_dNo ratings yet

- Report - Green Bonds-AUstralain Amd Asian Market PDFDocument6 pagesReport - Green Bonds-AUstralain Amd Asian Market PDFquratulain NazeerNo ratings yet

- Oil & Gas Uk - 2021Document36 pagesOil & Gas Uk - 2021Thiago Castro RodriguesNo ratings yet

- CSFRD ProposalDocument66 pagesCSFRD ProposalAnna HonorataNo ratings yet

- Bridge 2020 08 WestenbroekDocument24 pagesBridge 2020 08 WestenbroekSvetlin RanguelovNo ratings yet

- Proposal For Directive SustainabilityDocument63 pagesProposal For Directive SustainabilityALBA DIAZ SUAREZNo ratings yet

- Decarbonising End-use Sectors: Green Hydrogen CertificationFrom EverandDecarbonising End-use Sectors: Green Hydrogen CertificationNo ratings yet

- Article 6 of the Paris Agreement: Drawing Lessons from the Joint Crediting Mechanism (Version II)From EverandArticle 6 of the Paris Agreement: Drawing Lessons from the Joint Crediting Mechanism (Version II)No ratings yet

- JanetDocument3 pagesJanetHassanNo ratings yet

- Role of Accounting StandardsDocument10 pagesRole of Accounting StandardsMohd FaizanNo ratings yet

- Gaap - Stephen J BigelowDocument4 pagesGaap - Stephen J BigelowInnocent MundaNo ratings yet

- Operating LeaseDocument7 pagesOperating Leasesantosashleymay7No ratings yet

- BillDocument1 pageBillDebasis RoutNo ratings yet

- Compound Interest Worksheet 2Document1 pageCompound Interest Worksheet 2Akhil RajNo ratings yet

- Law of Business Organization - DissolutionDocument46 pagesLaw of Business Organization - DissolutionJasminAubreyNo ratings yet

- Risk and COCDocument28 pagesRisk and COCaneeshaNo ratings yet

- Commercial Bank OperationsDocument15 pagesCommercial Bank Operationsbonifacio gianga jrNo ratings yet

- Obligations and Contracts TestDocument28 pagesObligations and Contracts TestHazel Marie De GuzmanNo ratings yet

- Assignment 1 Essay (Saving Vs Investing)Document13 pagesAssignment 1 Essay (Saving Vs Investing)Nadirah ShahiraNo ratings yet

- Midterm II-1Document46 pagesMidterm II-1Josh MagatNo ratings yet

- Ijfs 07 00018 With CoverDocument14 pagesIjfs 07 00018 With CoverSultonmurod ZokhidovNo ratings yet

- Invoice 3678238462Document1 pageInvoice 3678238462Ritesh KumarNo ratings yet

- Notes: Source: Neil Dworkin, PH.D., Assistant Professor of Management, Western ConnectieutDocument3 pagesNotes: Source: Neil Dworkin, PH.D., Assistant Professor of Management, Western ConnectieutYohanaa Syafaat SiahaanNo ratings yet

- Whitepaper: Version 9.0 - 9 May 2018Document54 pagesWhitepaper: Version 9.0 - 9 May 2018Mongol ZaluuNo ratings yet

- Chun Ling Trial Exam 2022 - P2 (Answers)Document9 pagesChun Ling Trial Exam 2022 - P2 (Answers)Wei WenNo ratings yet

- BWPT - Annual Report - 2013 PDFDocument252 pagesBWPT - Annual Report - 2013 PDFNur NatasyaNo ratings yet

- Euro Zone Crisis QDocument70 pagesEuro Zone Crisis Qtarungupta2001No ratings yet

- Tugas Kelompok 5Document4 pagesTugas Kelompok 5Bought By UsNo ratings yet

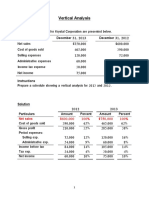

- Vertical Analysis SolutionsDocument5 pagesVertical Analysis SolutionsSamer IsmaelNo ratings yet

- Finance Assignment InstructionDocument7 pagesFinance Assignment InstructionJe-Ta CllNo ratings yet

- Certified Retail Banker: Ruqayya Alwan - Alya AlzaabiDocument15 pagesCertified Retail Banker: Ruqayya Alwan - Alya AlzaabiRoqaia AlwanNo ratings yet

- PWC Oil Gas Taxation 2012 10 enDocument32 pagesPWC Oil Gas Taxation 2012 10 enSudNo ratings yet

- The Government Corporate Counsel For Petitioner. Lorenzo A. Sales For Private RespondentsDocument3 pagesThe Government Corporate Counsel For Petitioner. Lorenzo A. Sales For Private RespondentsChristopher AdvinculaNo ratings yet

- India's BOP and Foreign ExchangeDocument7 pagesIndia's BOP and Foreign ExchangeSuria UnnikrishnanNo ratings yet

- Chapter Three Remittance: - 3.1 Outline of Remittance - 3.2 Procedure For Remittance - 3.3 Application of RemittanceDocument19 pagesChapter Three Remittance: - 3.1 Outline of Remittance - 3.2 Procedure For Remittance - 3.3 Application of Remittancevero100% (1)

- Reporting in Tax 1Document7 pagesReporting in Tax 1Lielet MatutinoNo ratings yet