Download as pptx, pdf, or txt

You might also like

- International Accounting Standards: IAS 29 "Financial Reporting in Hyperinflationary Economies"Document29 pagesInternational Accounting Standards: IAS 29 "Financial Reporting in Hyperinflationary Economies"Phebieon MukwenhaNo ratings yet

- R25 Financial Reporting Quality IFT NotesDocument20 pagesR25 Financial Reporting Quality IFT Notesmd mehmoodNo ratings yet

- Week 1 - Introduction To AccountingDocument34 pagesWeek 1 - Introduction To AccountingAidon StanleyNo ratings yet

- Week 1 - Introduction To AccountingDocument34 pagesWeek 1 - Introduction To AccountingAidon StanleyNo ratings yet

- LM10 Financial Reporting Quality IFT NotesDocument16 pagesLM10 Financial Reporting Quality IFT NotesjagjitbhaimbbsNo ratings yet

- Ifsa Chapter17Document67 pagesIfsa Chapter17luu hung100% (1)

- Cma Far 2024Document26 pagesCma Far 2024Montaser MohammedNo ratings yet

- Lecture 5Document34 pagesLecture 5Maham AhsanNo ratings yet

- Financial Accounting For ManagersDocument127 pagesFinancial Accounting For ManagerssowmtinaNo ratings yet

- Foundations of Entrepreneurship: Basic Accounting and Financial StatementsDocument89 pagesFoundations of Entrepreneurship: Basic Accounting and Financial StatementsTejaswi BandlamudiNo ratings yet

- Financial AccountancyDocument57 pagesFinancial AccountancyKhalilur Rehaman Savanur100% (1)

- Ac 1Document39 pagesAc 1taajNo ratings yet

- 7 Fin ReportingDocument33 pages7 Fin ReportingMuhammad JibranNo ratings yet

- Presentation of FS & Its' AuditingDocument27 pagesPresentation of FS & Its' AuditingTeamAudit Runner GroupNo ratings yet

- Conceptual Framework & Accounting StandardsDocument33 pagesConceptual Framework & Accounting StandardsJocy DelgadoNo ratings yet

- Bcom QbankDocument13 pagesBcom QbankIshaNo ratings yet

- Understanding Financial Statements C5Document19 pagesUnderstanding Financial Statements C5jerainmallari12No ratings yet

- Verde y Blanco Simple Moderno Capacitación Sobre Cómo Crear Una Presentación Oral de Canva Presentación Con Video (Autoguardado)Document41 pagesVerde y Blanco Simple Moderno Capacitación Sobre Cómo Crear Una Presentación Oral de Canva Presentación Con Video (Autoguardado)karen velozNo ratings yet

- IFRSDocument17 pagesIFRSAnushka chibdeNo ratings yet

- Slide f3 1 StudentDocument444 pagesSlide f3 1 Studentlinh nguyễn100% (1)

- Finance For Non-Finance PeopleDocument18 pagesFinance For Non-Finance PeopleSyed Muhammad AsimNo ratings yet

- CH 03Document31 pagesCH 03Tyler NielsenNo ratings yet

- Vinayak 22251 Accounts 1Document5 pagesVinayak 22251 Accounts 1vinayakNo ratings yet

- CHAPTER 1 and 2 Overview and Concepts in AccountingDocument15 pagesCHAPTER 1 and 2 Overview and Concepts in AccountingVin FajardoNo ratings yet

- BF-2 Assignment 1Document8 pagesBF-2 Assignment 1sabya.rathoreNo ratings yet

- Financial Accounting: Jaideep Jadhav Page 1 of 14Document14 pagesFinancial Accounting: Jaideep Jadhav Page 1 of 14krishangurawariyaNo ratings yet

- FRC CRR Annual Review Highlights October 2021Document6 pagesFRC CRR Annual Review Highlights October 2021Ziyodullo IsroilovNo ratings yet

- Revised AccountingDocument46 pagesRevised AccountingAli NasarNo ratings yet

- The Other Face of Managerial AccountingDocument20 pagesThe Other Face of Managerial AccountingModar AlzaiemNo ratings yet

- Chapter 2Document66 pagesChapter 2cejofe2892No ratings yet

- Creative AccountingDocument13 pagesCreative AccountingMira CE100% (1)

- Chapter 3 Managerial-Finance Solutions PDFDocument24 pagesChapter 3 Managerial-Finance Solutions PDFMohammad Mamun UddinNo ratings yet

- Chapter 2 Financial Statement and Cash Flow AnalysisDocument26 pagesChapter 2 Financial Statement and Cash Flow AnalysisFarooqChaudharyNo ratings yet

- Financial Statements and Analysis: ̈ Instructor's ResourcesDocument24 pagesFinancial Statements and Analysis: ̈ Instructor's ResourcesMohammad Mamun UddinNo ratings yet

- Chapter 2Document67 pagesChapter 2Adam MilakaraNo ratings yet

- FMA NotesDocument19 pagesFMA NotesLAXIANo ratings yet

- BAM 1 - Fundamentals of AccountingDocument33 pagesBAM 1 - Fundamentals of AccountingimheziiyyNo ratings yet

- Accounting: Prof: Jim Wallace TA: GolfDocument41 pagesAccounting: Prof: Jim Wallace TA: GolfNida BilalNo ratings yet

- Creative AccountingDocument11 pagesCreative AccountingSaskia Hanunnisak100% (1)

- Batson InternationalDocument24 pagesBatson InternationalAnand DedhiaNo ratings yet

- Chap 8 AccountingDocument28 pagesChap 8 AccountingnobelehlumisaNo ratings yet

- Q1Document8 pagesQ1SharanyaNo ratings yet

- Accounting Period Shareholders DividendsDocument3 pagesAccounting Period Shareholders DividendsAmaranathreddy YgNo ratings yet

- What Are Accounting StandardsDocument4 pagesWhat Are Accounting StandardsHimanshu SinghNo ratings yet

- Earnings & Financial Reporting Quality: Bistrova JuliaDocument32 pagesEarnings & Financial Reporting Quality: Bistrova JuliaRosalie Arguelles BachillerNo ratings yet

- Financial Essentials For DirectorsDocument70 pagesFinancial Essentials For DirectorsjohnnhaviraNo ratings yet

- 3.6.1 General Filing Requirements: Preparing and Filing Accounts. There Are Deadlines byDocument7 pages3.6.1 General Filing Requirements: Preparing and Filing Accounts. There Are Deadlines byJossie PhineNo ratings yet

- FR & FasDocument195 pagesFR & FasPrerana SharmaNo ratings yet

- Generally Accepted Accounting Principles (GAAP) Is A Term Used To Refer To The StandardDocument6 pagesGenerally Accepted Accounting Principles (GAAP) Is A Term Used To Refer To The StandardRahul JainNo ratings yet

- Introduction To Financial Statements: Wirecard ScandalDocument22 pagesIntroduction To Financial Statements: Wirecard ScandalNilesh Kumar GuptaNo ratings yet

- Notes - Introduction To Financial Statements, Ratio Analysis, Business OrganisationDocument8 pagesNotes - Introduction To Financial Statements, Ratio Analysis, Business OrganisationSilke HerbertNo ratings yet

- Finance Compendium PartII DMS IIT DelhiDocument55 pagesFinance Compendium PartII DMS IIT DelhiKhyati ChauhanNo ratings yet

- Review of Accounting ConceptsDocument9 pagesReview of Accounting ConceptsAngielyn PamandananNo ratings yet

- Lec 1Document29 pagesLec 1alinoornabeel110No ratings yet

- Introduction To Financial Statements and Other Financial ReportingDocument24 pagesIntroduction To Financial Statements and Other Financial ReportingAlina ZubairNo ratings yet

- Efa 09Document10 pagesEfa 09thuong13123No ratings yet

- Advanced Financial AccountingDocument17 pagesAdvanced Financial AccountingFisher100% (2)

- BUAD 804 Individual Assignement - Mayowa Omonile - P23DLBA80051Document7 pagesBUAD 804 Individual Assignement - Mayowa Omonile - P23DLBA80051Mayowa OmonileNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- a546437f-4a8a-4892-aa1a-fffbb3f57ba1Document19 pagesa546437f-4a8a-4892-aa1a-fffbb3f57ba1mayadevichandran94No ratings yet

- Chapter 5 1 1Document22 pagesChapter 5 1 1mayadevichandran94No ratings yet

- Chapter 1Document16 pagesChapter 1mayadevichandran94No ratings yet

- Chapter 9Document21 pagesChapter 9mayadevichandran94No ratings yet

- Chapter 12Document22 pagesChapter 12mayadevichandran94No ratings yet

- Chapter 11Document18 pagesChapter 11mayadevichandran94No ratings yet

- Chapter 10Document22 pagesChapter 10mayadevichandran94No ratings yet

- Chapter 8Document16 pagesChapter 8mayadevichandran94No ratings yet

- Business CombiDocument14 pagesBusiness CombiJohn Cesar PaunatNo ratings yet

- Islamic Banking in Bangladesh Progress and PotentialsDocument23 pagesIslamic Banking in Bangladesh Progress and Potentialssumaiya sumaNo ratings yet

- One Stop Payment Gateway Solution: Form-BuilderDocument35 pagesOne Stop Payment Gateway Solution: Form-BuilderSuryaChummaNo ratings yet

- Chance of A Lifetime (A Case Study) : Assignment No. 2 (FPM)Document4 pagesChance of A Lifetime (A Case Study) : Assignment No. 2 (FPM)Hamza KhalidNo ratings yet

- Aarti Industries - Company Update - 170921Document19 pagesAarti Industries - Company Update - 170921darshanmaldeNo ratings yet

- RockAuto Order Confirmation For Order 259622845Document1 pageRockAuto Order Confirmation For Order 259622845Manfred SchlagerNo ratings yet

- BUS 685-3 IB Lecture 2Document60 pagesBUS 685-3 IB Lecture 2Sadman SihabNo ratings yet

- Quanto Skew: Peter J Ackel First Version: 25th July 2009 This Version: 4th June 2016Document9 pagesQuanto Skew: Peter J Ackel First Version: 25th July 2009 This Version: 4th June 2016Hans WeissmanNo ratings yet

- Subramani PayslipDocument2 pagesSubramani PayslipMr. HarshaNo ratings yet

- Professional Resume: Accomplished Supply Chain Management/ Logistics/ SAP MM, WM, EWM Executive SummaryDocument5 pagesProfessional Resume: Accomplished Supply Chain Management/ Logistics/ SAP MM, WM, EWM Executive Summaryprakash rayNo ratings yet

- Hattia Update 10 Mei 2024Document27 pagesHattia Update 10 Mei 2024Nur AnisaNo ratings yet

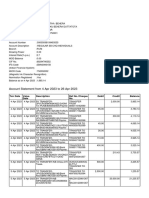

- Statement of Account: Transaction Date Description Debit Credit Available BalanceDocument13 pagesStatement of Account: Transaction Date Description Debit Credit Available BalanceIkramNo ratings yet

- Omnichannel Customer Experience: A Literature Review: Lisnawati Ratih Hurriyati Disman Vanessa GaffarDocument5 pagesOmnichannel Customer Experience: A Literature Review: Lisnawati Ratih Hurriyati Disman Vanessa GaffarAnh Vu LeNo ratings yet

- Account Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceBIKRAM KUMAR BEHERANo ratings yet

- A Queen Dies Slowly - The Rise and Decline of Iloilo CityDocument17 pagesA Queen Dies Slowly - The Rise and Decline of Iloilo CityJohn Feil JimenezNo ratings yet

- Bajaj Allianz Fund FactsheetDocument2 pagesBajaj Allianz Fund FactsheetgirlsbioNo ratings yet

- BIB English 2012Document114 pagesBIB English 2012Natnael100% (1)

- Bloomberg Businessweek 10-02-24Document68 pagesBloomberg Businessweek 10-02-24Viktor MadaraszNo ratings yet

- Central Bank Balance Sheet AnalysisDocument26 pagesCentral Bank Balance Sheet AnalysissuksesNo ratings yet

- 05january2024 India DailyDocument155 pages05january2024 India Dailypradeep kumarNo ratings yet

- History of The European UnionDocument21 pagesHistory of The European UnionSheejaVargheseNo ratings yet

- Cash BudgetDocument15 pagesCash Budgetpriyanshu kumari0% (1)

- Banking and Insurance Law ProjectDocument14 pagesBanking and Insurance Law ProjectVanshita GuptaNo ratings yet

- Sept 21 ExercisesDocument12 pagesSept 21 ExercisesPeachyNo ratings yet

- Afar1 Grp4 Acctng4materials Jit BackflushDocument39 pagesAfar1 Grp4 Acctng4materials Jit BackflushAngela Miles DizonNo ratings yet

- 1st-Quarter-Exam Applied EconomicsDocument4 pages1st-Quarter-Exam Applied EconomicsAndrew LimosNo ratings yet

- Presentacion de NexansDocument87 pagesPresentacion de Nexanssantiago foriguaNo ratings yet

- QuizDocument2 pagesQuizrysii gamesNo ratings yet

- Business StudyDocument4 pagesBusiness Studymurganv2006No ratings yet

- MGMT2023-Lecture 1-Intro To Financial ManagementDocument23 pagesMGMT2023-Lecture 1-Intro To Financial ManagementIsmadth2918388No ratings yet