Download as pptx, pdf, or txt

You might also like

- Coca Cola Distribution ChannelDocument2 pagesCoca Cola Distribution ChannelLalit Kumar93% (15)

- Economics ProjectDocument35 pagesEconomics ProjectRaviRamchandaniNo ratings yet

- Week 3 Macro2Document57 pagesWeek 3 Macro2Quần hoaNo ratings yet

- Macroeconomics: The Open Economy IDocument57 pagesMacroeconomics: The Open Economy IVaibhav AroraNo ratings yet

- Rhizopus SP HardDocument57 pagesRhizopus SP HardRizta RinindaNo ratings yet

- Chap 05Document55 pagesChap 05Iftikhar AhmedNo ratings yet

- Mankiw Chapter 5 Open Economy InvestmentDocument59 pagesMankiw Chapter 5 Open Economy InvestmentYusi PramandariNo ratings yet

- The Open Economy: AcroeconomicsDocument64 pagesThe Open Economy: AcroeconomicsRamesh vatsNo ratings yet

- The Open Economy: MacroeconomicsDocument59 pagesThe Open Economy: MacroeconomicsAngelique NitzakayaNo ratings yet

- Mankiw8e Chap06Document56 pagesMankiw8e Chap06Teak TatteeNo ratings yet

- The Open Economy: AcroeconomicsDocument60 pagesThe Open Economy: AcroeconomicsSheila AtienzaNo ratings yet

- Open Economy1Document64 pagesOpen Economy1Mariam JahanzebNo ratings yet

- Open EconomyDocument37 pagesOpen EconomyK.m.khizir AhmedNo ratings yet

- MPP 3Document25 pagesMPP 3Nghaktea J. FanaiNo ratings yet

- Imports and Exports As A Percentage of Output: 2000Document8 pagesImports and Exports As A Percentage of Output: 2000Adila ZambakovićNo ratings yet

- Ch. 5 - The Open EconomyDocument35 pagesCh. 5 - The Open EconomyaritjahjaNo ratings yet

- CHAP05Document61 pagesCHAP05Imam AwaluddinNo ratings yet

- The Open Economy: AcroeconomicsDocument60 pagesThe Open Economy: AcroeconomicsVaibhav AroraNo ratings yet

- Intermediate Macroeconomics (Ecn 2215) : The Open Economy by Charles M. Banda Notes Extracted From MankiwDocument29 pagesIntermediate Macroeconomics (Ecn 2215) : The Open Economy by Charles M. Banda Notes Extracted From MankiwYande ZuluNo ratings yet

- Ekonomi Makro I: Ekonomi Terbuka (Open Macroeconomics)Document16 pagesEkonomi Makro I: Ekonomi Terbuka (Open Macroeconomics)Reyna ArellanoNo ratings yet

- The Open Economy: MACROECONOMICS, 8th EditionDocument31 pagesThe Open Economy: MACROECONOMICS, 8th EditionFahriNo ratings yet

- Macroeconomics & The Global EconomyDocument23 pagesMacroeconomics & The Global Economysubash thapaNo ratings yet

- Session 4 Open EconomyDocument55 pagesSession 4 Open Economyshivam kumarNo ratings yet

- The Open Economy (N Gregory Mankiw 8th Edition)Document34 pagesThe Open Economy (N Gregory Mankiw 8th Edition)Desita Natalia Gunawan100% (1)

- The Open Economy: University of WisconsinDocument60 pagesThe Open Economy: University of WisconsinRanjana UpashiNo ratings yet

- Chap 06Document76 pagesChap 06Yiğit KocamanNo ratings yet

- IS - LM ModelDocument47 pagesIS - LM ModelMd AzizNo ratings yet

- The Small Open EconomyDocument21 pagesThe Small Open EconomyVrinda ModaNo ratings yet

- Chapter 3. Classical Theory: The Open Economy in The Long RunDocument45 pagesChapter 3. Classical Theory: The Open Economy in The Long RunMinh HangNo ratings yet

- Intermediate Macroeconomics: L1: National Income in Closed and Open EconomiesDocument39 pagesIntermediate Macroeconomics: L1: National Income in Closed and Open EconomiesJohn MainaNo ratings yet

- Princ ch32 PresentationDocument39 pagesPrinc ch32 PresentationJ.JEFRI CHENNo ratings yet

- Chapter 5: Open Economy: PreliminariesDocument10 pagesChapter 5: Open Economy: PreliminariesRahul Singh RajputNo ratings yet

- IS-LM FrameworkDocument54 pagesIS-LM FrameworkLakshmi NairNo ratings yet

- National-Income IIDocument41 pagesNational-Income IIVrinda RajoriaNo ratings yet

- (N. Gregory Mankiw) Macroeconomics (9th Edition) (BookFi) - Pages-176-182-DikompresiDocument7 pages(N. Gregory Mankiw) Macroeconomics (9th Edition) (BookFi) - Pages-176-182-DikompresiNoveliaNo ratings yet

- 178.200 06-8Document32 pages178.200 06-8api-3860979No ratings yet

- Economics: A Macroeconomic Theory of The Open EconomyDocument39 pagesEconomics: A Macroeconomic Theory of The Open Economypham nguyetNo ratings yet

- Mankiw Chapter 12 Mundell Fleming Model Is LM and ErDocument40 pagesMankiw Chapter 12 Mundell Fleming Model Is LM and Erbasirunjie86No ratings yet

- 6 Open EconomyDocument15 pages6 Open EconomyArsalan AliNo ratings yet

- Chap 16Document52 pagesChap 16Hamdi AbdirhmaanNo ratings yet

- Chapter-32-Macro-C32 Open Economy TheoryDocument43 pagesChapter-32-Macro-C32 Open Economy TheoryTruong Nguyen Thao Nhu (K17 DN)No ratings yet

- Chapt 05Document24 pagesChapt 05Ives LeeNo ratings yet

- Chapter 5Document67 pagesChapter 5Meselu BirliewNo ratings yet

- Chapter-32 For StudentsDocument41 pagesChapter-32 For StudentsNguyen Vu Thuc Uyen (K17 QN)No ratings yet

- Ad-AsDocument52 pagesAd-AsVandana RaoNo ratings yet

- Economic Growth IIDocument47 pagesEconomic Growth IIAmbra KoraNo ratings yet

- 18 - Keynesian Models Including The Government and Foreign Sector MCQsDocument12 pages18 - Keynesian Models Including The Government and Foreign Sector MCQsVenniah MusundaNo ratings yet

- CH 4 Open Macroeconomics AAUDocument100 pagesCH 4 Open Macroeconomics AAUFaris KhalidNo ratings yet

- LM R R : The Open EconomyDocument20 pagesLM R R : The Open EconomyZeNo ratings yet

- Growth 1Document57 pagesGrowth 1MahnoorNo ratings yet

- Mankiw-5e-Ch08-07012021-110127pmDocument23 pagesMankiw-5e-Ch08-07012021-110127pmSamNo ratings yet

- The Open Economy: MACROECONOMICS, 7th. Edition N. Gregory Mankiw Mannig J. SimidianDocument35 pagesThe Open Economy: MACROECONOMICS, 7th. Edition N. Gregory Mankiw Mannig J. SimidianMj MakilanNo ratings yet

- Chapter 32 - A Macroeconomic Theory of The Open Economy - StudentsDocument25 pagesChapter 32 - A Macroeconomic Theory of The Open Economy - StudentsPham Thi Phuong Anh (K16 HCM)No ratings yet

- Theory of Economic GrowthDocument97 pagesTheory of Economic GrowthHiệp Nguyễn Thị MinhNo ratings yet

- Slides For Chapter 5: Columbia University February 28, 2019Document47 pagesSlides For Chapter 5: Columbia University February 28, 2019Liu ChengNo ratings yet

- Theory of Economic GrowthDocument103 pagesTheory of Economic Growthkhanhto.workNo ratings yet

- Mundell FlemingDocument45 pagesMundell FlemingAna100% (1)

- Is LMDocument60 pagesIs LMtunaNo ratings yet

- International Macroeconomics: Slides For Chapter 2: Current Account SustainabilityDocument8 pagesInternational Macroeconomics: Slides For Chapter 2: Current Account SustainabilityM Kaderi KibriaNo ratings yet

- Open Economy Mankiw TutorialDocument28 pagesOpen Economy Mankiw TutorialProveedor Iptv EspañaNo ratings yet

- Keynesian is-LM ModelDocument45 pagesKeynesian is-LM ModelNorsurianaNo ratings yet

- Private Debt: Yield, Safety and the Emergence of Alternative LendingFrom EverandPrivate Debt: Yield, Safety and the Emergence of Alternative LendingNo ratings yet

- Syllabus - IBMDocument2 pagesSyllabus - IBMDEAN RESEARCH AND DEVELOPMENTNo ratings yet

- Exercises-Có Đáp ÁnDocument10 pagesExercises-Có Đáp ÁnDuyên Duyên100% (1)

- CH 7 Cost of CapitalDocument59 pagesCH 7 Cost of CapitalAsmi SinglaNo ratings yet

- Working Capital ManagementDocument29 pagesWorking Capital ManagementRohit MattuNo ratings yet

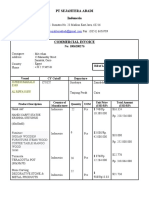

- Invoice BriandaSNDocument2 pagesInvoice BriandaSNJuang LaksanaNo ratings yet

- December 2020 Review: Euler Hermes Country Risk RatingsDocument5 pagesDecember 2020 Review: Euler Hermes Country Risk RatingsLFNo ratings yet

- How Can We ExportDocument94 pagesHow Can We ExportUdit PradeepNo ratings yet

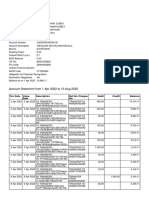

- Account Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubham TyagiNo ratings yet

- Top 10 Financial Services Companies in IndiaDocument2 pagesTop 10 Financial Services Companies in IndiaSapna NairNo ratings yet

- List of Non Deposit Accepting Non-Banking Financial Companies (NBFCS) As On February 28, 2017 Sr. No. Company Name Ahmedabad Regional OfficeDocument446 pagesList of Non Deposit Accepting Non-Banking Financial Companies (NBFCS) As On February 28, 2017 Sr. No. Company Name Ahmedabad Regional OfficeamandeepNo ratings yet

- SAP MM Accounting Entry..Ranjit YadavDocument18 pagesSAP MM Accounting Entry..Ranjit YadavItishreeNo ratings yet

- Tche 303 - Money and Banking Tutorial Assignment 6Document3 pagesTche 303 - Money and Banking Tutorial Assignment 6Tường ThuậtNo ratings yet

- ESL Banking Reading Comprehension PassageDocument2 pagesESL Banking Reading Comprehension PassageAbdirashid OsmanNo ratings yet

- Principles of Banking and FinanceDocument4 pagesPrinciples of Banking and FinanceEmmanuel NyachiriNo ratings yet

- International Trade Law AssignmentsDocument6 pagesInternational Trade Law AssignmentsNilotpal RaiNo ratings yet

- UGEC 2226 Discovering Africa: Environment, Society and ProspectsDocument40 pagesUGEC 2226 Discovering Africa: Environment, Society and ProspectsMan Lai LeeNo ratings yet

- Lime BrochureDocument20 pagesLime BrochureDignity SortexNo ratings yet

- Safe Shop Plan - 2022 JuneDocument40 pagesSafe Shop Plan - 2022 Juneshinu pokemon masterNo ratings yet

- 22 To 27 - Appendix-XXII To XXVII (Page 326-334)Document9 pages22 To 27 - Appendix-XXII To XXVII (Page 326-334)08 Ajay Halder 11- CNo ratings yet

- WAHDA KonşimentoDocument1 pageWAHDA Konşimentoفتحي القزيريNo ratings yet

- History Proposed Mock Examination, 2019Document11 pagesHistory Proposed Mock Examination, 2019edwinmasaiNo ratings yet

- In Class Quiz 3 - Attempt ReviewDocument7 pagesIn Class Quiz 3 - Attempt ReviewLan PhươngNo ratings yet

- Answer Eco211 Dec 2018.PDFDocument9 pagesAnswer Eco211 Dec 2018.PDFRusyda AzizNo ratings yet

- Ads 2122 555603 PDFDocument3 pagesAds 2122 555603 PDFHarsh PatelNo ratings yet

- Money and Banking PPT QuestionsDocument41 pagesMoney and Banking PPT Questionszainab130831No ratings yet

- 4.export Channels of DistributionDocument24 pages4.export Channels of DistributionRayhan Atunu50% (2)

- 9781398308282CambEconsWorkBook AnswersFinalDocument71 pages9781398308282CambEconsWorkBook AnswersFinalAlvaro SalazarNo ratings yet

- Unit 5 CashDocument9 pagesUnit 5 CashNigussie BerhanuNo ratings yet