BL Unit 2 Contract of Guarantee

BL Unit 2 Contract of Guarantee

You might also like

- 29 - Draft of Will DeedDocument4 pages29 - Draft of Will Deedbatuksid100% (6)

- The 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsFrom EverandThe 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsRating: 5 out of 5 stars5/5 (1)

- Harding Vs Commercial Union Assurance CoDocument2 pagesHarding Vs Commercial Union Assurance CoShiela Pilar100% (1)

- Consignment AgreementDocument15 pagesConsignment Agreementpeaser0712No ratings yet

- LawDocument11 pagesLawSaad ArshadNo ratings yet

- 13, Contracts of Indemnity and GuaranteeDocument20 pages13, Contracts of Indemnity and GuaranteeGhulam Hassan0% (1)

- Contract of Guarantee Definition of Contract of Guarantee: It Is A Contract To Perform The Promise or Discharge TheDocument9 pagesContract of Guarantee Definition of Contract of Guarantee: It Is A Contract To Perform The Promise or Discharge TheSuchitra SureshNo ratings yet

- Corporate and Other Laws - Notes - CA Inter (New) (1) ICADocument34 pagesCorporate and Other Laws - Notes - CA Inter (New) (1) ICADivyanshu SharmaNo ratings yet

- Kle BL M9Document20 pagesKle BL M9pramit04No ratings yet

- Rights of SuretyDocument18 pagesRights of Suretyankit00009No ratings yet

- Securities Law Contracts of GuaranteeDocument6 pagesSecurities Law Contracts of GuaranteesteNo ratings yet

- What Is A Contract of Guarantee According To Contract Act?: Surety Principal Debtor Creditor ExampleDocument4 pagesWhat Is A Contract of Guarantee According To Contract Act?: Surety Principal Debtor Creditor ExampleIbrahim HassanNo ratings yet

- L 16 Contract of Indemnity and Guarantee 1Document86 pagesL 16 Contract of Indemnity and Guarantee 1Aastha AroraNo ratings yet

- BNK602SEM: Legal Aspects of Banking: TOPIC 5: Indemnity and GuaranteeDocument34 pagesBNK602SEM: Legal Aspects of Banking: TOPIC 5: Indemnity and GuaranteealiaNo ratings yet

- Contract of Indemnity and Law of GuaranteeDocument7 pagesContract of Indemnity and Law of GuaranteeBilawal Mughal100% (1)

- DTL LB 090419Document32 pagesDTL LB 090419Palak ChawlaNo ratings yet

- Indemnity and Guarantee AssignmentDocument5 pagesIndemnity and Guarantee AssignmentShayan KhanNo ratings yet

- Contract of Guarantee 2022Document14 pagesContract of Guarantee 2022Jasson JonesNo ratings yet

- F IndemnityGuaranteeDocument11 pagesF IndemnityGuaranteeNeha BhayaniNo ratings yet

- Contract of Indemnity and GuaranteeDocument10 pagesContract of Indemnity and Guaranteecommercewaale1No ratings yet

- GuaranteeDocument86 pagesGuaranteeManjeev Singh SahniNo ratings yet

- Contract LawDocument57 pagesContract LawJannat ZaidiNo ratings yet

- Business Law FinalDocument80 pagesBusiness Law FinalFakhira ShehzadiNo ratings yet

- Indeminity and GuaranteeDocument18 pagesIndeminity and GuaranteeAanika AeryNo ratings yet

- Contract of Indemnity & GuaranteeDocument3 pagesContract of Indemnity & Guaranteekrishnaghumra67No ratings yet

- Indemnity and Gurantee BL Week 6 06032023 102419amDocument33 pagesIndemnity and Gurantee BL Week 6 06032023 102419amDaym MehmoodNo ratings yet

- Contract II AnswersDocument21 pagesContract II AnswersK LNo ratings yet

- Discharge and Rights of SuretyDocument8 pagesDischarge and Rights of Suretyjerry zaidiNo ratings yet

- Right of SuretyDocument13 pagesRight of SuretyShrikant soni100% (4)

- 6 Indemnity Guarantee Bailment Pledge PDFDocument11 pages6 Indemnity Guarantee Bailment Pledge PDFPavan BasundeNo ratings yet

- Revocation of GuaranteeDocument13 pagesRevocation of Guaranteeharipriya tharigondaNo ratings yet

- Contracts of Indemnity and GuaranteeDocument30 pagesContracts of Indemnity and GuaranteetarushnicheNo ratings yet

- Unit I Contract of Indemnity and GuaranteeDocument52 pagesUnit I Contract of Indemnity and GuaranteeHemanta PahariNo ratings yet

- Contract of GuaranteeDocument4 pagesContract of GuaranteeSesa GillNo ratings yet

- NotesDocument89 pagesNotesJaya KumarNo ratings yet

- Contingent ContractDocument56 pagesContingent ContractAniket YadavNo ratings yet

- Contract of Guaranteed OffDocument117 pagesContract of Guaranteed OffAnkit SathyaNo ratings yet

- Contract of Indemnity Contract of GuaranteeDocument19 pagesContract of Indemnity Contract of Guaranteekalra_kamal12100% (2)

- Unit 3 Contract of Indemnity and Guarantee: StructureDocument15 pagesUnit 3 Contract of Indemnity and Guarantee: StructuregaardiNo ratings yet

- Contract Act PropositionsDocument15 pagesContract Act PropositionsJudicial AspirantNo ratings yet

- Characteristics: State Etc. v. Bank of India. IDocument9 pagesCharacteristics: State Etc. v. Bank of India. IChaitu ChaituNo ratings yet

- Law of Contract IIDocument58 pagesLaw of Contract IIranjusanjuNo ratings yet

- Indeminity and GuaranteeDocument8 pagesIndeminity and GuaranteeAnbarasan Subu100% (2)

- Contracts of Indemnity and GuaranteeDocument15 pagesContracts of Indemnity and Guaranteemybrowserapp.storeNo ratings yet

- Unit Objectives Learning OutcomesDocument20 pagesUnit Objectives Learning OutcomesAkash BaratheNo ratings yet

- Business Law Unit 2Document62 pagesBusiness Law Unit 2Deepak TongliNo ratings yet

- Special Contract ActDocument45 pagesSpecial Contract ActRohit Kalia67% (6)

- Contract of IndemnityDocument21 pagesContract of IndemnitysaadRaulNo ratings yet

- NotesDocument15 pagesNotesArshil ShahNo ratings yet

- Unit-Ii Indemnity and GuaranteeDocument11 pagesUnit-Ii Indemnity and Guaranteepravin awalkondeNo ratings yet

- Indemnity & GuaranteeDocument21 pagesIndemnity & GuaranteeSushmita DasNo ratings yet

- Final PPT Special ContractsDocument34 pagesFinal PPT Special ContractsMegha Vidhyasagar100% (1)

- Indemnity and GuaranteeDocument11 pagesIndemnity and GuaranteeTrishala SinghNo ratings yet

- Contract Ii Model Answer PaperDocument34 pagesContract Ii Model Answer PaperShubham Pandey100% (1)

- Law Assignment On Special Contract Act & Pubic and Private CompanyDocument41 pagesLaw Assignment On Special Contract Act & Pubic and Private CompanyArushiNo ratings yet

- Indemnity and Guarantee by Asif Khan Qurtuba University Peshawar... BUSINESS LAW.Document6 pagesIndemnity and Guarantee by Asif Khan Qurtuba University Peshawar... BUSINESS LAW.shinwarrikhanNo ratings yet

- Fybms 157 Law Project Jai LilaniDocument6 pagesFybms 157 Law Project Jai LilaniDeesha MirwaniNo ratings yet

- 3 Indemnity and Guarantee 2Document38 pages3 Indemnity and Guarantee 2taimoor akbarNo ratings yet

- Project Work On Revocation of Continuing Guarantee: Aniket RanjanDocument9 pagesProject Work On Revocation of Continuing Guarantee: Aniket RanjanAbhishek RajNo ratings yet

- Contracts of IndemnityDocument17 pagesContracts of IndemnityShekhar ShrivastavaNo ratings yet

- Right of SuretyDocument3 pagesRight of SuretyAdan Hooda100% (2)

- Contracts of Indemnity and GuaranteeDocument19 pagesContracts of Indemnity and GuaranteeKazia Shamoon AhmedNo ratings yet

- Life, Accident and Health Insurance in the United StatesFrom EverandLife, Accident and Health Insurance in the United StatesRating: 5 out of 5 stars5/5 (1)

- Summary of TRAIN LAWDocument45 pagesSummary of TRAIN LAWKyle JastillanaNo ratings yet

- BWBS3043 Chapter 7 TakafulDocument30 pagesBWBS3043 Chapter 7 TakafulcorinnatsyNo ratings yet

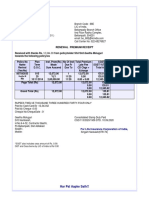

- Renewal Premium Receipt: Har Pal Aapke Sath!!Document1 pageRenewal Premium Receipt: Har Pal Aapke Sath!!krishna krishNo ratings yet

- Avon Protection Systems All Products WarrantyDocument4 pagesAvon Protection Systems All Products WarrantyManuelMartinezNo ratings yet

- GL3655EDocument0 pagesGL3655EandyhrNo ratings yet

- Design ContractDocument7 pagesDesign ContractOllie DesrochersNo ratings yet

- Hud 221D4Document2 pagesHud 221D4eimg20041333No ratings yet

- Own Damage-06-Feb-2021 To 05-Feb-2022: Schedule of Premium (Amount in RS.)Document4 pagesOwn Damage-06-Feb-2021 To 05-Feb-2022: Schedule of Premium (Amount in RS.)avnish sharmaNo ratings yet

- Answer of Exam 1Document18 pagesAnswer of Exam 1አሌክሳንደር ኦሊቨርNo ratings yet

- Solved A Retailer of Electronic Equipment Received Six Vcrs From The PDFDocument1 pageSolved A Retailer of Electronic Equipment Received Six Vcrs From The PDFAnbu jaromiaNo ratings yet

- Republica DominicanaDocument13 pagesRepublica Dominicanacst89No ratings yet

- Taiex Guide For ExpertsDocument4 pagesTaiex Guide For ExpertsllllllluisNo ratings yet

- Ch01.Ppt OverviewDocument55 pagesCh01.Ppt OverviewMohammadYaqoob100% (1)

- Policy 0000000001523360 PDFDocument15 pagesPolicy 0000000001523360 PDFunique infraNo ratings yet

- HDFC ERGO General Insurance Company Limited: Policy No. 2311 1001 8502 4001 000Document3 pagesHDFC ERGO General Insurance Company Limited: Policy No. 2311 1001 8502 4001 000Suresh KumarNo ratings yet

- PR SafeDocument4 pagesPR SafePanchdev KumarNo ratings yet

- Chapter 13 - The Theory of Income TaxationDocument34 pagesChapter 13 - The Theory of Income Taxationwatts1100% (1)

- Plaridel Surety vs. ArtexDocument7 pagesPlaridel Surety vs. ArtexShane Nuss RedNo ratings yet

- What Is Life Insurance ?Document15 pagesWhat Is Life Insurance ?Jagdish SutharNo ratings yet

- AC551 MidtermDocument10 pagesAC551 MidtermAbigail GutierrezNo ratings yet

- IGCSE ECONOMICS: Factor PaymentsDocument2 pagesIGCSE ECONOMICS: Factor Paymentskbafna28100% (1)

- IMI's Code of Professional ConductDocument5 pagesIMI's Code of Professional ConductAbu AlgebraNo ratings yet

- ss4 Instructions PDFDocument7 pagesss4 Instructions PDFIanDubhNo ratings yet

- SOP For Medical InsuranceDocument3 pagesSOP For Medical Insuranceirfankhosa622No ratings yet

- Income Tax Act, 1961: Section 28. Profits and Gains of Business or ProfessionDocument6 pagesIncome Tax Act, 1961: Section 28. Profits and Gains of Business or Professiongslahoti70No ratings yet

- Intercity Operations RFPDocument11 pagesIntercity Operations RFPJoseph LimNo ratings yet

- Blutms Saas AgreementDocument7 pagesBlutms Saas AgreementAbayomi OlatidoyeNo ratings yet

Download as pptx, pdf, or txt

You might also like

- 29 - Draft of Will DeedDocument4 pages29 - Draft of Will Deedbatuksid100% (6)

- The 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsFrom EverandThe 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsRating: 5 out of 5 stars5/5 (1)

- Harding Vs Commercial Union Assurance CoDocument2 pagesHarding Vs Commercial Union Assurance CoShiela Pilar100% (1)

- Consignment AgreementDocument15 pagesConsignment Agreementpeaser0712No ratings yet

- LawDocument11 pagesLawSaad ArshadNo ratings yet

- 13, Contracts of Indemnity and GuaranteeDocument20 pages13, Contracts of Indemnity and GuaranteeGhulam Hassan0% (1)

- Contract of Guarantee Definition of Contract of Guarantee: It Is A Contract To Perform The Promise or Discharge TheDocument9 pagesContract of Guarantee Definition of Contract of Guarantee: It Is A Contract To Perform The Promise or Discharge TheSuchitra SureshNo ratings yet

- Corporate and Other Laws - Notes - CA Inter (New) (1) ICADocument34 pagesCorporate and Other Laws - Notes - CA Inter (New) (1) ICADivyanshu SharmaNo ratings yet

- Kle BL M9Document20 pagesKle BL M9pramit04No ratings yet

- Rights of SuretyDocument18 pagesRights of Suretyankit00009No ratings yet

- Securities Law Contracts of GuaranteeDocument6 pagesSecurities Law Contracts of GuaranteesteNo ratings yet

- What Is A Contract of Guarantee According To Contract Act?: Surety Principal Debtor Creditor ExampleDocument4 pagesWhat Is A Contract of Guarantee According To Contract Act?: Surety Principal Debtor Creditor ExampleIbrahim HassanNo ratings yet

- L 16 Contract of Indemnity and Guarantee 1Document86 pagesL 16 Contract of Indemnity and Guarantee 1Aastha AroraNo ratings yet

- BNK602SEM: Legal Aspects of Banking: TOPIC 5: Indemnity and GuaranteeDocument34 pagesBNK602SEM: Legal Aspects of Banking: TOPIC 5: Indemnity and GuaranteealiaNo ratings yet

- Contract of Indemnity and Law of GuaranteeDocument7 pagesContract of Indemnity and Law of GuaranteeBilawal Mughal100% (1)

- DTL LB 090419Document32 pagesDTL LB 090419Palak ChawlaNo ratings yet

- Indemnity and Guarantee AssignmentDocument5 pagesIndemnity and Guarantee AssignmentShayan KhanNo ratings yet

- Contract of Guarantee 2022Document14 pagesContract of Guarantee 2022Jasson JonesNo ratings yet

- F IndemnityGuaranteeDocument11 pagesF IndemnityGuaranteeNeha BhayaniNo ratings yet

- Contract of Indemnity and GuaranteeDocument10 pagesContract of Indemnity and Guaranteecommercewaale1No ratings yet

- GuaranteeDocument86 pagesGuaranteeManjeev Singh SahniNo ratings yet

- Contract LawDocument57 pagesContract LawJannat ZaidiNo ratings yet

- Business Law FinalDocument80 pagesBusiness Law FinalFakhira ShehzadiNo ratings yet

- Indeminity and GuaranteeDocument18 pagesIndeminity and GuaranteeAanika AeryNo ratings yet

- Contract of Indemnity & GuaranteeDocument3 pagesContract of Indemnity & Guaranteekrishnaghumra67No ratings yet

- Indemnity and Gurantee BL Week 6 06032023 102419amDocument33 pagesIndemnity and Gurantee BL Week 6 06032023 102419amDaym MehmoodNo ratings yet

- Contract II AnswersDocument21 pagesContract II AnswersK LNo ratings yet

- Discharge and Rights of SuretyDocument8 pagesDischarge and Rights of Suretyjerry zaidiNo ratings yet

- Right of SuretyDocument13 pagesRight of SuretyShrikant soni100% (4)

- 6 Indemnity Guarantee Bailment Pledge PDFDocument11 pages6 Indemnity Guarantee Bailment Pledge PDFPavan BasundeNo ratings yet

- Revocation of GuaranteeDocument13 pagesRevocation of Guaranteeharipriya tharigondaNo ratings yet

- Contracts of Indemnity and GuaranteeDocument30 pagesContracts of Indemnity and GuaranteetarushnicheNo ratings yet

- Unit I Contract of Indemnity and GuaranteeDocument52 pagesUnit I Contract of Indemnity and GuaranteeHemanta PahariNo ratings yet

- Contract of GuaranteeDocument4 pagesContract of GuaranteeSesa GillNo ratings yet

- NotesDocument89 pagesNotesJaya KumarNo ratings yet

- Contingent ContractDocument56 pagesContingent ContractAniket YadavNo ratings yet

- Contract of Guaranteed OffDocument117 pagesContract of Guaranteed OffAnkit SathyaNo ratings yet

- Contract of Indemnity Contract of GuaranteeDocument19 pagesContract of Indemnity Contract of Guaranteekalra_kamal12100% (2)

- Unit 3 Contract of Indemnity and Guarantee: StructureDocument15 pagesUnit 3 Contract of Indemnity and Guarantee: StructuregaardiNo ratings yet

- Contract Act PropositionsDocument15 pagesContract Act PropositionsJudicial AspirantNo ratings yet

- Characteristics: State Etc. v. Bank of India. IDocument9 pagesCharacteristics: State Etc. v. Bank of India. IChaitu ChaituNo ratings yet

- Law of Contract IIDocument58 pagesLaw of Contract IIranjusanjuNo ratings yet

- Indeminity and GuaranteeDocument8 pagesIndeminity and GuaranteeAnbarasan Subu100% (2)

- Contracts of Indemnity and GuaranteeDocument15 pagesContracts of Indemnity and Guaranteemybrowserapp.storeNo ratings yet

- Unit Objectives Learning OutcomesDocument20 pagesUnit Objectives Learning OutcomesAkash BaratheNo ratings yet

- Business Law Unit 2Document62 pagesBusiness Law Unit 2Deepak TongliNo ratings yet

- Special Contract ActDocument45 pagesSpecial Contract ActRohit Kalia67% (6)

- Contract of IndemnityDocument21 pagesContract of IndemnitysaadRaulNo ratings yet

- NotesDocument15 pagesNotesArshil ShahNo ratings yet

- Unit-Ii Indemnity and GuaranteeDocument11 pagesUnit-Ii Indemnity and Guaranteepravin awalkondeNo ratings yet

- Indemnity & GuaranteeDocument21 pagesIndemnity & GuaranteeSushmita DasNo ratings yet

- Final PPT Special ContractsDocument34 pagesFinal PPT Special ContractsMegha Vidhyasagar100% (1)

- Indemnity and GuaranteeDocument11 pagesIndemnity and GuaranteeTrishala SinghNo ratings yet

- Contract Ii Model Answer PaperDocument34 pagesContract Ii Model Answer PaperShubham Pandey100% (1)

- Law Assignment On Special Contract Act & Pubic and Private CompanyDocument41 pagesLaw Assignment On Special Contract Act & Pubic and Private CompanyArushiNo ratings yet

- Indemnity and Guarantee by Asif Khan Qurtuba University Peshawar... BUSINESS LAW.Document6 pagesIndemnity and Guarantee by Asif Khan Qurtuba University Peshawar... BUSINESS LAW.shinwarrikhanNo ratings yet

- Fybms 157 Law Project Jai LilaniDocument6 pagesFybms 157 Law Project Jai LilaniDeesha MirwaniNo ratings yet

- 3 Indemnity and Guarantee 2Document38 pages3 Indemnity and Guarantee 2taimoor akbarNo ratings yet

- Project Work On Revocation of Continuing Guarantee: Aniket RanjanDocument9 pagesProject Work On Revocation of Continuing Guarantee: Aniket RanjanAbhishek RajNo ratings yet

- Contracts of IndemnityDocument17 pagesContracts of IndemnityShekhar ShrivastavaNo ratings yet

- Right of SuretyDocument3 pagesRight of SuretyAdan Hooda100% (2)

- Contracts of Indemnity and GuaranteeDocument19 pagesContracts of Indemnity and GuaranteeKazia Shamoon AhmedNo ratings yet

- Life, Accident and Health Insurance in the United StatesFrom EverandLife, Accident and Health Insurance in the United StatesRating: 5 out of 5 stars5/5 (1)

- Summary of TRAIN LAWDocument45 pagesSummary of TRAIN LAWKyle JastillanaNo ratings yet

- BWBS3043 Chapter 7 TakafulDocument30 pagesBWBS3043 Chapter 7 TakafulcorinnatsyNo ratings yet

- Renewal Premium Receipt: Har Pal Aapke Sath!!Document1 pageRenewal Premium Receipt: Har Pal Aapke Sath!!krishna krishNo ratings yet

- Avon Protection Systems All Products WarrantyDocument4 pagesAvon Protection Systems All Products WarrantyManuelMartinezNo ratings yet

- GL3655EDocument0 pagesGL3655EandyhrNo ratings yet

- Design ContractDocument7 pagesDesign ContractOllie DesrochersNo ratings yet

- Hud 221D4Document2 pagesHud 221D4eimg20041333No ratings yet

- Own Damage-06-Feb-2021 To 05-Feb-2022: Schedule of Premium (Amount in RS.)Document4 pagesOwn Damage-06-Feb-2021 To 05-Feb-2022: Schedule of Premium (Amount in RS.)avnish sharmaNo ratings yet

- Answer of Exam 1Document18 pagesAnswer of Exam 1አሌክሳንደር ኦሊቨርNo ratings yet

- Solved A Retailer of Electronic Equipment Received Six Vcrs From The PDFDocument1 pageSolved A Retailer of Electronic Equipment Received Six Vcrs From The PDFAnbu jaromiaNo ratings yet

- Republica DominicanaDocument13 pagesRepublica Dominicanacst89No ratings yet

- Taiex Guide For ExpertsDocument4 pagesTaiex Guide For ExpertsllllllluisNo ratings yet

- Ch01.Ppt OverviewDocument55 pagesCh01.Ppt OverviewMohammadYaqoob100% (1)

- Policy 0000000001523360 PDFDocument15 pagesPolicy 0000000001523360 PDFunique infraNo ratings yet

- HDFC ERGO General Insurance Company Limited: Policy No. 2311 1001 8502 4001 000Document3 pagesHDFC ERGO General Insurance Company Limited: Policy No. 2311 1001 8502 4001 000Suresh KumarNo ratings yet

- PR SafeDocument4 pagesPR SafePanchdev KumarNo ratings yet

- Chapter 13 - The Theory of Income TaxationDocument34 pagesChapter 13 - The Theory of Income Taxationwatts1100% (1)

- Plaridel Surety vs. ArtexDocument7 pagesPlaridel Surety vs. ArtexShane Nuss RedNo ratings yet

- What Is Life Insurance ?Document15 pagesWhat Is Life Insurance ?Jagdish SutharNo ratings yet

- AC551 MidtermDocument10 pagesAC551 MidtermAbigail GutierrezNo ratings yet

- IGCSE ECONOMICS: Factor PaymentsDocument2 pagesIGCSE ECONOMICS: Factor Paymentskbafna28100% (1)

- IMI's Code of Professional ConductDocument5 pagesIMI's Code of Professional ConductAbu AlgebraNo ratings yet

- ss4 Instructions PDFDocument7 pagesss4 Instructions PDFIanDubhNo ratings yet

- SOP For Medical InsuranceDocument3 pagesSOP For Medical Insuranceirfankhosa622No ratings yet

- Income Tax Act, 1961: Section 28. Profits and Gains of Business or ProfessionDocument6 pagesIncome Tax Act, 1961: Section 28. Profits and Gains of Business or Professiongslahoti70No ratings yet

- Intercity Operations RFPDocument11 pagesIntercity Operations RFPJoseph LimNo ratings yet

- Blutms Saas AgreementDocument7 pagesBlutms Saas AgreementAbayomi OlatidoyeNo ratings yet