Download as pptx, pdf, or txt

You might also like

- Money & Banking DallasDocument16 pagesMoney & Banking DallasBZ Riger100% (1)

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceFrom EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinanceRating: 4 out of 5 stars4/5 (9)

- Usps Money OrderDocument4 pagesUsps Money Ordermulibunso67% (3)

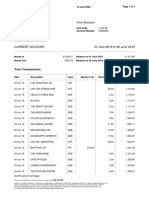

- Account Number Statement Period: ActivityDocument2 pagesAccount Number Statement Period: ActivityTim McGraw100% (2)

- Mrunal Sir's Economy 2020 Batch - Handout PDFDocument32 pagesMrunal Sir's Economy 2020 Batch - Handout PDFssattyyaammNo ratings yet

- Money MechanicsDocument79 pagesMoney MechanicsjoReGal100% (2)

- Fee Challan Subject Change PDFDocument1 pageFee Challan Subject Change PDFAnonymous Qfi6uDE100% (1)

- Attachments 71b8d55c 2019 June Statement PDFDocument5 pagesAttachments 71b8d55c 2019 June Statement PDFMarianaNo ratings yet

- Finacle Book For Bank Auditors PDFDocument54 pagesFinacle Book For Bank Auditors PDFGaurav jain100% (1)

- Money - Born of Credit?: SpeechDocument16 pagesMoney - Born of Credit?: Speechfadsfaw100% (1)

- Chap.14.Money - Bank. 1Document27 pagesChap.14.Money - Bank. 1Nguyễn Trần Duy AnhNo ratings yet

- 7 MoneyDocument33 pages7 Moneykunjal pasariNo ratings yet

- Money & Banks... The Hidden Truth Behind The Global Debt Scam by Richard GreavesDocument12 pagesMoney & Banks... The Hidden Truth Behind The Global Debt Scam by Richard GreavespoiuymNo ratings yet

- Ec103 Week 07 and 08 s14Document31 pagesEc103 Week 07 and 08 s14юрий локтионовNo ratings yet

- Fixing Our Broken Economy v2Document6 pagesFixing Our Broken Economy v2Dan George IIINo ratings yet

- Money InflationDocument11 pagesMoney InflationvaxyaNo ratings yet

- How Banking Developed - Fin 102 July 2018Document14 pagesHow Banking Developed - Fin 102 July 2018beaNo ratings yet

- Week 9-10 - Chapter 20 - Money, Prices and Financial IntermediariesDocument28 pagesWeek 9-10 - Chapter 20 - Money, Prices and Financial IntermediariesOona NiallNo ratings yet

- Economics AssignmentsDocument12 pagesEconomics AssignmentsDj DannexNo ratings yet

- 8 Money & Banking Part I: Money & Banks: Macro./ Topic 8 / P.1Document9 pages8 Money & Banking Part I: Money & Banks: Macro./ Topic 8 / P.1Syed TariqshahNo ratings yet

- Macroeconomics Module 5Document6 pagesMacroeconomics Module 5Jonnel GadinganNo ratings yet

- Who Creates Money?: L'éco en BrefDocument3 pagesWho Creates Money?: L'éco en BrefcesarangomezNo ratings yet

- Chap 5 Money Supply and Bank NegaraDocument59 pagesChap 5 Money Supply and Bank NegaraDashania GregoryNo ratings yet

- Frictional & Instrumen Kebij MoneterDocument41 pagesFrictional & Instrumen Kebij MoneterBagus GilangNo ratings yet

- The Banking SystemDocument29 pagesThe Banking SystemNghĩa HuỳnhNo ratings yet

- Makro - Monetary PolicyDocument17 pagesMakro - Monetary PolicyCindy Gusti RohanNo ratings yet

- The Banking System, What Banks Do.Document25 pagesThe Banking System, What Banks Do.Andreas Widhi100% (1)

- International Money and Banking: 2. Banks and Financial IntermediationDocument15 pagesInternational Money and Banking: 2. Banks and Financial IntermediationMohammed Said MaamraNo ratings yet

- Macro Money, Monetary Policy & Tools UpdatedDocument38 pagesMacro Money, Monetary Policy & Tools UpdatedZerin RushmiNo ratings yet

- (Lecture 8.1) Chapter 11 Money and Financial System (L8)Document28 pages(Lecture 8.1) Chapter 11 Money and Financial System (L8)Chen Yee KhooNo ratings yet

- How To Travel HimachalDocument15 pagesHow To Travel HimachalShubham ChoudharyNo ratings yet

- Mankiw - Money and Finansial SystemDocument37 pagesMankiw - Money and Finansial SystemBRYAN SIANDRYNo ratings yet

- Macro - EconomicsDocument28 pagesMacro - EconomicsFarabi GulandazNo ratings yet

- The Money GameDocument13 pagesThe Money GameMuneeb AliNo ratings yet

- 1911193643Document199 pages1911193643Alex KoNo ratings yet

- Banks and Bank Risks The Role of BanksDocument12 pagesBanks and Bank Risks The Role of BanksRosunnieNo ratings yet

- Lec2.6.1 SlidesDocument32 pagesLec2.6.1 SlidesmanandeepamazonNo ratings yet

- Ch2 (Supply of Money)Document22 pagesCh2 (Supply of Money)Rezuanul RafiNo ratings yet

- Lecture 8Document47 pagesLecture 8Billiee ButccherNo ratings yet

- Money and Banking-InflationDocument7 pagesMoney and Banking-InflationRahziel Lopena San JoseNo ratings yet

- Apuntes Unit 3Document12 pagesApuntes Unit 3Sara TapiaNo ratings yet

- The Money MarketDocument20 pagesThe Money MarketNick GrzebienikNo ratings yet

- Origin of The Word: Banca, From Old High German Banc, Bank "Bench, Counter". Benches Were Used As Desks orDocument6 pagesOrigin of The Word: Banca, From Old High German Banc, Bank "Bench, Counter". Benches Were Used As Desks orSarvesh JaiswalNo ratings yet

- The Monetary System: Solutions To Textbook ProblemsDocument9 pagesThe Monetary System: Solutions To Textbook ProblemsMainland FounderNo ratings yet

- Money and Financial SystemDocument37 pagesMoney and Financial SystemTheresiaNo ratings yet

- MacroEconomics2e Chapter14Document29 pagesMacroEconomics2e Chapter14Minh NguyệtNo ratings yet

- Chapter 7Document17 pagesChapter 7Yasin IsikNo ratings yet

- Broad Money and Narrow MoneyDocument39 pagesBroad Money and Narrow MoneyAmit Daga0% (1)

- The Bank of EnglandDocument10 pagesThe Bank of EnglandМаша ЛиNo ratings yet

- M7 MoneyDocument35 pagesM7 MoneyJohnny SinsNo ratings yet

- 3 - Money Supply and Money CreationDocument14 pages3 - Money Supply and Money Creationmajmmallikarachchi.mallikarachchiNo ratings yet

- Ch. 12 MoneyDocument30 pagesCh. 12 Moneylauravertelcanada2023No ratings yet

- Mecanica Moderna Del Dinero PDFDocument50 pagesMecanica Moderna Del Dinero PDFHarold AponteNo ratings yet

- Insider Information: What Wall Street Doesn't Want Your Street to KnowFrom EverandInsider Information: What Wall Street Doesn't Want Your Street to KnowNo ratings yet

- Debt 101: From Interest Rates and Credit Scores to Student Loans and Debt Payoff Strategies, an Essential Primer on Managing DebtFrom EverandDebt 101: From Interest Rates and Credit Scores to Student Loans and Debt Payoff Strategies, an Essential Primer on Managing DebtRating: 4 out of 5 stars4/5 (3)

- Top 9 Crypto Picks: How you can win in the Cryptocurrency revolution!From EverandTop 9 Crypto Picks: How you can win in the Cryptocurrency revolution!No ratings yet

- ARGOS Cape - Credit - AgreementDocument12 pagesARGOS Cape - Credit - Agreementlomaxpl1No ratings yet

- Credit Card Webquest: WWW - Aie.o RGDocument3 pagesCredit Card Webquest: WWW - Aie.o RGapi-299234513No ratings yet

- Financial Analysis of HDFC BankDocument48 pagesFinancial Analysis of HDFC BankAbhay JainNo ratings yet

- E Money PDFDocument41 pagesE Money PDFCPMMNo ratings yet

- Post Graduate Diploma Course On Banking & FinanceDocument3 pagesPost Graduate Diploma Course On Banking & FinanceKuthubudeen T MNo ratings yet

- Swift CodeDocument2 pagesSwift CodeEmmarold OdwongosNo ratings yet

- Pengantar Akuntan II: Present Value of Principal To Be Received at MaturityDocument4 pagesPengantar Akuntan II: Present Value of Principal To Be Received at MaturityalifNo ratings yet

- Philippine Deposit Insurance Corporation (Pdic) :: Pdic Act (Ra 3591, As Amended)Document2 pagesPhilippine Deposit Insurance Corporation (Pdic) :: Pdic Act (Ra 3591, As Amended)Arvin John MasuelaNo ratings yet

- SBLC Offer For A Leased BG-SBLC, Procedure and MemorandumDocument2 pagesSBLC Offer For A Leased BG-SBLC, Procedure and MemorandumSharonNo ratings yet

- ArnelDocument3 pagesArnelMedz NicolasNo ratings yet

- Ramky Infrastructure Limited - HyderabadDocument13 pagesRamky Infrastructure Limited - HyderabadgopikrishnaggkNo ratings yet

- Specimen Copy For M.Tech Admission Interview Call LetterDocument3 pagesSpecimen Copy For M.Tech Admission Interview Call LetterApeksha KoreNo ratings yet

- AXIS Bank RTGS & NEFT FormDocument11 pagesAXIS Bank RTGS & NEFT FormNeha JunejaNo ratings yet

- 5 6087118687465112700Document4 pages5 6087118687465112700Vishnu KumarNo ratings yet

- 22049896 - Presentation Submission for session 11 - Nguyễn Hữu Minh TuấnDocument11 pages22049896 - Presentation Submission for session 11 - Nguyễn Hữu Minh TuấnTuấn NguyễnNo ratings yet

- Wise Transaction Invoice Transfer 569634840 754051821 enDocument2 pagesWise Transaction Invoice Transfer 569634840 754051821 enAETHERNo ratings yet

- Financial Assets, Money, Financial Transactions, and Financial InstitutionsDocument24 pagesFinancial Assets, Money, Financial Transactions, and Financial InstitutionsJeremy MacalaladNo ratings yet

- Ibs TMN Sri Serdang, S'Gor 1 30/06/22Document30 pagesIbs TMN Sri Serdang, S'Gor 1 30/06/22Mohd Rozli Mohd KassimNo ratings yet

- Questionnaire For GICDocument5 pagesQuestionnaire For GICSowmi DaaluNo ratings yet

- Banking and Negotiable Instruments Course Outline - Garima GoswamiDocument17 pagesBanking and Negotiable Instruments Course Outline - Garima GoswamiShabriNo ratings yet

- PRESENTATION in Rural BankingDocument18 pagesPRESENTATION in Rural BankingglorydharmarajNo ratings yet

- Holy Cross College: B. Cause and EffectDocument12 pagesHoly Cross College: B. Cause and EffectSam VeraNo ratings yet

- 2019 Mid-Year promotion-NineYes Furniture PDFDocument3 pages2019 Mid-Year promotion-NineYes Furniture PDFIbrahim JaleelNo ratings yet

- UTS182868063 Auth LetterDocument3 pagesUTS182868063 Auth LetterChamathi PiyasadiniNo ratings yet

- Personal Loan PDFDocument3 pagesPersonal Loan PDFbusiness loanNo ratings yet