Download as pptx, pdf, or txt

You might also like

- Planning Campaigns (2111) - 40080344-July 2021-1Document27 pagesPlanning Campaigns (2111) - 40080344-July 2021-1anfal ibrahim83% (12)

- Comprehensive Finance Cheat Sheet Collection 1698244606Document52 pagesComprehensive Finance Cheat Sheet Collection 1698244606muratgreywolf100% (1)

- Retail Value Map - DeloitteDocument22 pagesRetail Value Map - DeloitteWilliam Poon100% (1)

- How To Valuation A CompanyDocument42 pagesHow To Valuation A Companyapi-3720563100% (3)

- Benchmarking Best Practices for Maintenance, Reliability and Asset ManagementFrom EverandBenchmarking Best Practices for Maintenance, Reliability and Asset ManagementNo ratings yet

- BPR For Oil and Gas ConstructionDocument6 pagesBPR For Oil and Gas ConstructionMOORTHY.KENo ratings yet

- Marketing Strategy: (Current & Domestic)Document29 pagesMarketing Strategy: (Current & Domestic)Michelle Eaktavewut100% (6)

- Kellogg's Supply Chain - From Manufacturing To ShelfDocument4 pagesKellogg's Supply Chain - From Manufacturing To Shelfmahavir_lohanaNo ratings yet

- Section - 1 - AnalyzeDocument10 pagesSection - 1 - AnalyzemoorthyNo ratings yet

- BAA R I Presentation FINAL 10.02.11Document27 pagesBAA R I Presentation FINAL 10.02.11Olu AjayiNo ratings yet

- C.O.Capital - Capital Budgeting (OK Na!)Document8 pagesC.O.Capital - Capital Budgeting (OK Na!)Eunice BernalNo ratings yet

- Discounted Cash FlowDocument36 pagesDiscounted Cash Flowapi-3838939100% (13)

- 20007Document5 pages20007Archana J RetinueNo ratings yet

- Lazard IR 2Q23 FINALDocument45 pagesLazard IR 2Q23 FINALVincent BerryNo ratings yet

- Introduction to Financial AnalyticsDocument7 pagesIntroduction to Financial Analyticsasim.khwajaNo ratings yet

- Supply Chains and Working Capital: ManagementDocument60 pagesSupply Chains and Working Capital: ManagementMarko NikolicNo ratings yet

- Accounting Standard Summary Notes Group IDocument15 pagesAccounting Standard Summary Notes Group ISrinivasprasadNo ratings yet

- Interpretation of Financial Statements & Ratio AnalysisDocument35 pagesInterpretation of Financial Statements & Ratio Analysisamitsinghslideshare50% (2)

- BusinessValuationModelingCoursePresentation 200527 140843Document93 pagesBusinessValuationModelingCoursePresentation 200527 140843Maruthi Sabbani100% (3)

- Financial Statement Analysis RatiosDocument4 pagesFinancial Statement Analysis RatiosAmelieNo ratings yet

- Accounting Principles and Business Transactions Cheat Sheet: by ViaDocument1 pageAccounting Principles and Business Transactions Cheat Sheet: by Viaheehan6No ratings yet

- Asset Management Valuations and IlsDocument53 pagesAsset Management Valuations and Ilsarunjangra566No ratings yet

- Capital Expenditure Planning PDFDocument15 pagesCapital Expenditure Planning PDFArchie LazaroNo ratings yet

- Hotels & Resorts: Analytics at TheDocument2 pagesHotels & Resorts: Analytics at TheridwanhakimNo ratings yet

- Kapayas Enterprise: English Private Limited Company Malay Sole-Proprietorship/OthersDocument74 pagesKapayas Enterprise: English Private Limited Company Malay Sole-Proprietorship/OthersRachael0% (1)

- Unit 1: The Future of Procurement and Supply ChainDocument4 pagesUnit 1: The Future of Procurement and Supply Chainmiriam lopezNo ratings yet

- Financial Accounting Analysis Cheat SheetDocument1 pageFinancial Accounting Analysis Cheat SheetMinyu LvNo ratings yet

- Comparable Company Transaction AnalysisDocument31 pagesComparable Company Transaction Analysismisha bansalNo ratings yet

- Part 1 Theories ReviewerDocument18 pagesPart 1 Theories ReviewerNey Dela CruzNo ratings yet

- WH Tis ?: Fundamental Analysis A Fundamental AnalysisDocument7 pagesWH Tis ?: Fundamental Analysis A Fundamental AnalysisAbhinandan ChatterjeeNo ratings yet

- Sap - Financial Statement PlanningDocument28 pagesSap - Financial Statement PlanningRobert van MeijerenNo ratings yet

- 7 Types of Financial ModelsDocument1 page7 Types of Financial Modelsofficial.waqaslatifNo ratings yet

- Oracle Ebusiness Suite - Release 12 Financials Point of View and Upgrade Solutions PackDocument59 pagesOracle Ebusiness Suite - Release 12 Financials Point of View and Upgrade Solutions PackNRK MurthyNo ratings yet

- Joint Venture Management - Sales Positioning - EN20210624Document41 pagesJoint Venture Management - Sales Positioning - EN20210624pramodpatidar2018No ratings yet

- 2022 Transaction ReviewDocument36 pages2022 Transaction ReviewKevin ParkerNo ratings yet

- DCF Valuation Course Notes 365 Financial AnalystDocument12 pagesDCF Valuation Course Notes 365 Financial AnalystArice BertrandNo ratings yet

- Economic Value AddedDocument25 pagesEconomic Value AddedSagar KansalNo ratings yet

- Business Case Study - Entertainment ParkDocument8 pagesBusiness Case Study - Entertainment ParkShivaniNo ratings yet

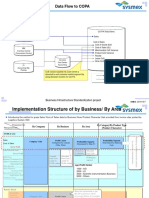

- Data Flow To COPA: Business Infrastructure Standardization ProjectDocument3 pagesData Flow To COPA: Business Infrastructure Standardization ProjectT SAIKIRANNo ratings yet

- Benchmark Introduction in ITDocument13 pagesBenchmark Introduction in ITluc henryNo ratings yet

- Leadership Retreat 10012024Document44 pagesLeadership Retreat 10012024Mshelia M.No ratings yet

- FINAL Semiconductor Co-Investment Program Announcement DeckDocument11 pagesFINAL Semiconductor Co-Investment Program Announcement DeckTyler YanNo ratings yet

- Ipsita CV May2020Document2 pagesIpsita CV May2020Ipsita DuttaNo ratings yet

- BofA-FEBC-M3-Advanced Valuation TechniquesDocument18 pagesBofA-FEBC-M3-Advanced Valuation TechniquesBazaar AajNo ratings yet

- FAR210 MFRS116 PPE - Oct23Document28 pagesFAR210 MFRS116 PPE - Oct23Nur Alya DamiaNo ratings yet

- MS11 - Capital BudgetingDocument8 pagesMS11 - Capital BudgetingElsie GenovaNo ratings yet

- Free Cash Flow Introduction TrainingDocument130 pagesFree Cash Flow Introduction Trainingashrafhussein100% (5)

- Zrive IB 1Q23 Intro To Valuation Methods Up2Document9 pagesZrive IB 1Q23 Intro To Valuation Methods Up2Luis Soldevilla MorenoNo ratings yet

- Standardized Approach For Counterparty Credit RiskDocument2 pagesStandardized Approach For Counterparty Credit RiskjalutukNo ratings yet

- Proposal - Digital Transformation - Banking and Capital MarketsDocument52 pagesProposal - Digital Transformation - Banking and Capital MarketsAnkit CapoorNo ratings yet

- ROI Metrics Are Direct, Easy-To-Interpret Profitability MeasuresDocument20 pagesROI Metrics Are Direct, Easy-To-Interpret Profitability MeasuresValentina GeorgievaNo ratings yet

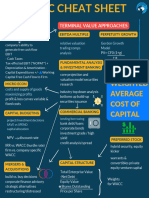

- Cost of Capital 2018Document118 pagesCost of Capital 2018Elik Məmmədov100% (1)

- Introduction To Financial Statement Analysis: by Prof Arun Kumar Agarwal, ACA, ACS IBS, GurgaonDocument13 pagesIntroduction To Financial Statement Analysis: by Prof Arun Kumar Agarwal, ACA, ACS IBS, GurgaonPRACHI DASNo ratings yet

- CS As A Valuer-IndoreDocument42 pagesCS As A Valuer-IndoreGAURAVNo ratings yet

- Session 7-WACCDocument65 pagesSession 7-WACCmichael musillaNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- Agile Procurement: Volume II: Designing and Implementing a Digital TransformationFrom EverandAgile Procurement: Volume II: Designing and Implementing a Digital TransformationNo ratings yet

- A Handbook on Various Aspects of Business and Its Integration with Finance in Modern World: A Bridgeway to Thoughtful CommunicationFrom EverandA Handbook on Various Aspects of Business and Its Integration with Finance in Modern World: A Bridgeway to Thoughtful CommunicationNo ratings yet

- Financial Steering: Valuation, KPI Management and the Interaction with IFRSFrom EverandFinancial Steering: Valuation, KPI Management and the Interaction with IFRSNo ratings yet

- Valuable OSS - Delivering a Return on Your Investment in Operational Support Systems (OSS)From EverandValuable OSS - Delivering a Return on Your Investment in Operational Support Systems (OSS)No ratings yet

- ECO Comic StripsDocument4 pagesECO Comic StripsNurul Izzaty bt Md Zaini100% (1)

- Gain - Pro Report - Private Equity vs. Independently HeldDocument36 pagesGain - Pro Report - Private Equity vs. Independently HeldLegonNo ratings yet

- 13 Dela Cruz - Chapters 5 and 6 Summaries PDFDocument12 pages13 Dela Cruz - Chapters 5 and 6 Summaries PDFMau Dela CruzNo ratings yet

- ALIGNINGDocument16 pagesALIGNINGgianlucaNo ratings yet

- How To Build A Powerful Human Resources Strategy: Master Course - Episode 04Document9 pagesHow To Build A Powerful Human Resources Strategy: Master Course - Episode 04Muhammad Jafar100% (1)

- Concepts of Marketing1Document31 pagesConcepts of Marketing1nesey76043No ratings yet

- Production Possibility: Curve (PPC)Document33 pagesProduction Possibility: Curve (PPC)quratulainNo ratings yet

- Distribution Model For FMCGDocument20 pagesDistribution Model For FMCGRahul Gupta100% (1)

- Supply Chain Operations Reference ModelDocument7 pagesSupply Chain Operations Reference ModelRegina Arballo Moreira CesarNo ratings yet

- Chapter 1: Company Profile 1.1. Introduction CompanyDocument7 pagesChapter 1: Company Profile 1.1. Introduction Companypink pinkNo ratings yet

- Management Accounting and Analysis: Name: Rana Vivek SinghDocument8 pagesManagement Accounting and Analysis: Name: Rana Vivek SinghRana Vivek SinghNo ratings yet

- Bank Management CIA 3 (A)Document25 pagesBank Management CIA 3 (A)Shrikaran BeecharajuNo ratings yet

- Product Management: Dhaval BhatkarDocument14 pagesProduct Management: Dhaval BhatkarAmrutha P RNo ratings yet

- ACCA AA TuitionEx2021-22 CBE As JG21Jan crw1502 gf0203 crw0403 SPi12MarDocument22 pagesACCA AA TuitionEx2021-22 CBE As JG21Jan crw1502 gf0203 crw0403 SPi12MarAbid AliNo ratings yet

- LLP BSPLDocument17 pagesLLP BSPLKiran KumarNo ratings yet

- Chapter 3 An Introduction To Consolidated Financial Statements - STDDocument54 pagesChapter 3 An Introduction To Consolidated Financial Statements - STDdhfbbbbbbbbbbbbbbbbbh100% (1)

- About XL DynamicsDocument7 pagesAbout XL DynamicsBHUPIENo ratings yet

- SharpShooterScalpingStrategy FuturesDocument24 pagesSharpShooterScalpingStrategy FuturesOmar CendronNo ratings yet

- Lecture 2 BCG MatrixDocument26 pagesLecture 2 BCG MatrixAnant MishraNo ratings yet

- Topic 7: Elements of MarketingDocument17 pagesTopic 7: Elements of MarketingSamuel KabandaNo ratings yet

- W1 Defining Financial TermsDocument6 pagesW1 Defining Financial TermsSuzie TaingNo ratings yet

- MGT959 Stock Market Operations 14723::lalit Kumar Bhardwaj 3.0 0.0 0.0 3.0 Courses With Conceptual FocusDocument7 pagesMGT959 Stock Market Operations 14723::lalit Kumar Bhardwaj 3.0 0.0 0.0 3.0 Courses With Conceptual FocusAnkit Singh ChauhanNo ratings yet

- FSA - Ch02 - Introduction To Financial Statements and Other Financial Reporting TopicsDocument32 pagesFSA - Ch02 - Introduction To Financial Statements and Other Financial Reporting TopicsSamar MessaoudNo ratings yet

- Learning Skills Assg 2Document11 pagesLearning Skills Assg 2BETTY WEE CHONG TIAN STUDENTNo ratings yet

- Chopra3 PPT ch01Document25 pagesChopra3 PPT ch01osama haseebNo ratings yet

- Beaver 1968 PDFDocument27 pagesBeaver 1968 PDFYosi Yulivia100% (1)