Download as pptx, pdf, or txt

You might also like

- HW NongradedDocument4 pagesHW NongradedAnDy YiMNo ratings yet

- Interest Rate SwapsDocument6 pagesInterest Rate SwapsKanchan ChawlaNo ratings yet

- FM Assignment-2Document8 pagesFM Assignment-2Rajarshi DaharwalNo ratings yet

- DerivativesDocument65 pagesDerivativesShreyas DongreNo ratings yet

- Forward Rate AgreementsDocument3 pagesForward Rate AgreementssahilgeraNo ratings yet

- Forward Rate Agreement NotesDocument4 pagesForward Rate Agreement NotesSangram PandaNo ratings yet

- Forward Contract Exchange Rate: Fras NotationDocument2 pagesForward Contract Exchange Rate: Fras Notationmuzzamil123No ratings yet

- Forward Rate AgreementsDocument3 pagesForward Rate AgreementsNaga Mani MeruguNo ratings yet

- Interest Rate FuturesDocument103 pagesInterest Rate FuturesSumit SinghNo ratings yet

- Interest Rate DerivativesDocument9 pagesInterest Rate DerivativesPrasad Nayak100% (1)

- 2 Forward Rate AgreementDocument8 pages2 Forward Rate AgreementRicha Gupta100% (1)

- Komal Traesury AssignmentDocument11 pagesKomal Traesury AssignmentmanaskaushikNo ratings yet

- Forward Forward 13TH November 2020Document12 pagesForward Forward 13TH November 2020Jovan SsenkandwaNo ratings yet

- Forward Rate Agreement CalculationDocument4 pagesForward Rate Agreement Calculationjustinmark99No ratings yet

- Forward Rate AgreementsDocument2 pagesForward Rate Agreementsajain22No ratings yet

- Valuation of A Forward Rate Agreement (Pp. 95-96) : Example: You Agree To Borrow $100 From September 1Document5 pagesValuation of A Forward Rate Agreement (Pp. 95-96) : Example: You Agree To Borrow $100 From September 1Reza Al SaadNo ratings yet

- Swapd and FRAsDocument53 pagesSwapd and FRAsSCCEGNo ratings yet

- Forward Rate Agreements: Learning CurveDocument9 pagesForward Rate Agreements: Learning CurveLu DanqingNo ratings yet

- FRADocument4 pagesFRASeema SrivastavaNo ratings yet

- General Knowledge Today - 113Document2 pagesGeneral Knowledge Today - 113niranjan_meharNo ratings yet

- Session 6.3-Forward Rate Agreements LectureDocument6 pagesSession 6.3-Forward Rate Agreements LectureQamber AliNo ratings yet

- Pitele de CapitalDocument14 pagesPitele de CapitalFelix RemeteaNo ratings yet

- Chap 18Document110 pagesChap 18Desai SarvidaNo ratings yet

- CH 18Document131 pagesCH 18Desai SarvidaNo ratings yet

- Forward-Forward Contract and Forward Rate Agreement.Document6 pagesForward-Forward Contract and Forward Rate Agreement.tinotendacarltonNo ratings yet

- Chapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolDocument25 pagesChapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolJuana BoresNo ratings yet

- Forward Rate AgreementsDocument6 pagesForward Rate AgreementsAmul ShresthaNo ratings yet

- Valuation of A Forward Rate Agreement PDFDocument5 pagesValuation of A Forward Rate Agreement PDFdjtaz13No ratings yet

- International Financial Management PgapteDocument30 pagesInternational Financial Management Pgapterameshmba100% (1)

- Managing Fixed-Income Positions With OTC DerivativesDocument86 pagesManaging Fixed-Income Positions With OTC DerivativestniravNo ratings yet

- Financial Engineering and PlanningDocument17 pagesFinancial Engineering and PlanningSavius AllyNo ratings yet

- Forward Rate Agreements: Session 3 - Derivatives & Risk MGTDocument15 pagesForward Rate Agreements: Session 3 - Derivatives & Risk MGTMayankSharmaNo ratings yet

- Interest Rate DerivativesDocument58 pagesInterest Rate DerivativesIndia Forex100% (2)

- M Waqas BBFE-17-48 Assignment #3Document4 pagesM Waqas BBFE-17-48 Assignment #3Muhammad WaQaSNo ratings yet

- Derivatives in ALMDocument53 pagesDerivatives in ALMSam SinhaNo ratings yet

- Fixed Income & Interest Rate DerivativesDocument64 pagesFixed Income & Interest Rate DerivativeskarthikNo ratings yet

- Chapter 10 - Forward and Futures Contracts ExamplesDocument65 pagesChapter 10 - Forward and Futures Contracts ExamplesLeon MushiNo ratings yet

- Forward Rate Agreement (FRA)Document3 pagesForward Rate Agreement (FRA)Shriyanshi JaitlyNo ratings yet

- Uni Flex 120922Document12 pagesUni Flex 120922wilsonNo ratings yet

- Swaps and Interest Rate DerivativesDocument20 pagesSwaps and Interest Rate DerivativesShankar VenkatramanNo ratings yet

- Swap Derivatives: Forward Swaps and SwaptionsDocument74 pagesSwap Derivatives: Forward Swaps and Swaptionsvineet_bmNo ratings yet

- Financial Risk Management - SWAPDocument23 pagesFinancial Risk Management - SWAPChau NguyenNo ratings yet

- F3 Chapter 10Document22 pagesF3 Chapter 10Ali ShahnawazNo ratings yet

- TM Interest Rate SwapDocument16 pagesTM Interest Rate SwapTran ManhNo ratings yet

- II. Interest RatesDocument15 pagesII. Interest RatesDaniel Salas LeonNo ratings yet

- EFB344 Lecture07, FRAs and SwapsDocument35 pagesEFB344 Lecture07, FRAs and SwapsTibet LoveNo ratings yet

- (Lehman Brothers, Tuckman) Interest Rate Parity, Money Market Baisis Swaps, and Cross-Currency Basis SwapsDocument14 pages(Lehman Brothers, Tuckman) Interest Rate Parity, Money Market Baisis Swaps, and Cross-Currency Basis SwapsJonathan Ching100% (1)

- Derivatives - Betting: Chapter Break UpDocument34 pagesDerivatives - Betting: Chapter Break UpJatinkatrodiyaNo ratings yet

- CH 14Document31 pagesCH 14mohamedhusseindableNo ratings yet

- Lecture 6Document32 pagesLecture 6Nilesh PanchalNo ratings yet

- TFS 2015 Lecture 12 Open Revision SessionV2Document29 pagesTFS 2015 Lecture 12 Open Revision SessionV2ThorNo ratings yet

- Bonds ValuationsDocument57 pagesBonds ValuationsarmailgmNo ratings yet

- Name of The Teacher: Gayathri Ravikumar Department: Commerce PG. Subject/Paper Class Year Date Class Time Unit Topic Interest Rate SwapsDocument5 pagesName of The Teacher: Gayathri Ravikumar Department: Commerce PG. Subject/Paper Class Year Date Class Time Unit Topic Interest Rate SwapsGayu RkNo ratings yet

- Currency Derivative1Document47 pagesCurrency Derivative1IubianNo ratings yet

- Interest Rate RiskDocument33 pagesInterest Rate RiskirfanhaidersewagNo ratings yet

- Instructor: Dr. LAU Sie Ting: Course Notes For Seminar 3 Chapter 5: Time Value of Money Part BDocument34 pagesInstructor: Dr. LAU Sie Ting: Course Notes For Seminar 3 Chapter 5: Time Value of Money Part B朱艺璇No ratings yet

- Test Your Knowledge: 2.2.4.2 Pricing of SwaptionsDocument11 pagesTest Your Knowledge: 2.2.4.2 Pricing of SwaptionsRITZ BROWNNo ratings yet

- AFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Document24 pagesAFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Johar MenezesNo ratings yet

- Amendments To The Loan Documents Prsuant To Switching Over To MCLR Linked InterestDocument7 pagesAmendments To The Loan Documents Prsuant To Switching Over To MCLR Linked InterestPRAJA rajyamNo ratings yet

- 5 Simple Interest and DiscountDocument69 pages5 Simple Interest and DiscountJUSTIN HECTOR BRENT SAJULGANo ratings yet

- Ch4: Havaldar and CavaleDocument27 pagesCh4: Havaldar and CavaleShubha Brota Raha75% (4)

- Sales ForcastingDocument28 pagesSales Forcastingkr_dandekarNo ratings yet

- Discriminant Analysis For Risk Classification and PredictionDocument23 pagesDiscriminant Analysis For Risk Classification and PredictionSumit SharmaNo ratings yet

- Analysis of DLF (FINAL)Document31 pagesAnalysis of DLF (FINAL)Sumit SharmaNo ratings yet

- WTO Provisions and Implications For IndiaDocument19 pagesWTO Provisions and Implications For IndiaSumit SharmaNo ratings yet

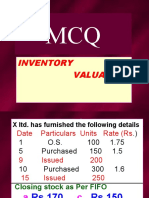

- MCQ Inventory Valuation LBSIMDocument49 pagesMCQ Inventory Valuation LBSIMSumit SharmaNo ratings yet

- BankerDocument2 pagesBankerNguyễn Thanh HươngNo ratings yet

- MBA Mortgage Market StabilizationDocument5 pagesMBA Mortgage Market StabilizationJohn MechemNo ratings yet

- Introductions: 1.1 Purpose of The Project DefinitionDocument10 pagesIntroductions: 1.1 Purpose of The Project Definitionnaruto boeingNo ratings yet

- Valuation and Rates of ReturnDocument16 pagesValuation and Rates of ReturnKhairul NisaNo ratings yet

- John Maynard KeynesDocument7 pagesJohn Maynard KeynesCanadianValueNo ratings yet

- C 12 LCNRV - Problem SolvingDocument1 pageC 12 LCNRV - Problem Solvingkyle mandaresioNo ratings yet

- Unicorn Interactive PDF2.0 3Document40 pagesUnicorn Interactive PDF2.0 3roviko1611No ratings yet

- Capital BudgetingDocument47 pagesCapital BudgetingShaheer AliNo ratings yet

- GodrejDocument4 pagesGodrejdeepaksikriNo ratings yet

- Foreign Direct Investment Research PaperDocument8 pagesForeign Direct Investment Research Paperxvszcorif100% (1)

- Cost Cutting Ideas PDFDocument4 pagesCost Cutting Ideas PDFmuthuswamy77100% (1)

- PreliOfferDocument96 pagesPreliOfferMuhammad IbadNo ratings yet

- Impressions From Ideaweek St. Moritz 2020Document13 pagesImpressions From Ideaweek St. Moritz 2020RNo ratings yet

- Coinforex Company ProfileDocument15 pagesCoinforex Company Profilelewisjr344No ratings yet

- 21 Secrets I Wish I Knew at The Start of My Investing CareerDocument5 pages21 Secrets I Wish I Knew at The Start of My Investing Careerjohnsmith1806No ratings yet

- A Cash Management in A Supper Market StoreDocument64 pagesA Cash Management in A Supper Market Storechukwu solomon67% (3)

- A Study of Customer Satisfaction Towards Mutual Funds Executive SummaryDocument71 pagesA Study of Customer Satisfaction Towards Mutual Funds Executive SummaryHarprit KaurNo ratings yet

- 1001Document2 pages1001Lovely Dela Cruz GanoanNo ratings yet

- F2 - Financial ManagementDocument20 pagesF2 - Financial ManagementRobert MunyaradziNo ratings yet

- This Study Resource WasDocument8 pagesThis Study Resource WasRoghayeh MOUSAVISAGHARCHINo ratings yet

- Rules On Bursa Malaysia Securities BerhadDocument193 pagesRules On Bursa Malaysia Securities BerhadSeo Soon YiNo ratings yet

- Chapter-I: Derivatives (Futures & Options)Document18 pagesChapter-I: Derivatives (Futures & Options)burranareshNo ratings yet

- 2019-01-24 Rekha Mourya - Coypm9419m - 2018Document25 pages2019-01-24 Rekha Mourya - Coypm9419m - 2018ApoorvNo ratings yet

- Vce Summmer Internship Program ( - Stock Market)Document21 pagesVce Summmer Internship Program ( - Stock Market)Annu KashyapNo ratings yet

- Dividend Policy, Growth, and The Valuation of Shares-1961Document24 pagesDividend Policy, Growth, and The Valuation of Shares-1961Ming CheNo ratings yet

- 8553-Advanced Fnancial AccountingDocument19 pages8553-Advanced Fnancial AccountingSaad BashirNo ratings yet

- Nur Afni Yunita, Muftia Chairunnisa: Nurafni - Yunita@unimal - Ac.idDocument10 pagesNur Afni Yunita, Muftia Chairunnisa: Nurafni - Yunita@unimal - Ac.idJannah LathubaNo ratings yet

- How Can You Invest in Your Health and EducationDocument2 pagesHow Can You Invest in Your Health and EducationNermeen C. AlapaNo ratings yet

- IEDA 3230: Engineering EconomyDocument10 pagesIEDA 3230: Engineering EconomyjnfzNo ratings yet