Download as ppt, pdf, or txt

You might also like

- Unit III Receivables Management - Concept of Credit PolicyDocument16 pagesUnit III Receivables Management - Concept of Credit PolicyYash Raj Tripathi0% (1)

- Unit 3 - Receivable ManagementDocument18 pagesUnit 3 - Receivable Managementharish50% (2)

- Chapter 28 Credit ManagementDocument26 pagesChapter 28 Credit Management185496185496100% (1)

- FM Management NotesDocument96 pagesFM Management NotesGovindh200178% (9)

- Credit PolicyDocument84 pagesCredit PolicyDan John Karikottu100% (6)

- "Any Fool Can Lend Money, But It Takes Lot of Skills To Get It Back" Presented By-Anisha.NDocument20 pages"Any Fool Can Lend Money, But It Takes Lot of Skills To Get It Back" Presented By-Anisha.NShalini NagavarapuNo ratings yet

- Presented By: Neha Chopra Mba Sem IiiDocument14 pagesPresented By: Neha Chopra Mba Sem IiiyashsviNo ratings yet

- Assignment of Receivables ManagementDocument6 pagesAssignment of Receivables ManagementHarsh ChauhanNo ratings yet

- Account Receivables Management & Credit Policy: Presented byDocument37 pagesAccount Receivables Management & Credit Policy: Presented byKhalid Khan100% (1)

- Accounts Receivables ManagementDocument11 pagesAccounts Receivables ManagementAli xNo ratings yet

- Accounts ReceivableDocument52 pagesAccounts Receivablemarget100% (3)

- Account Receivable ManagementDocument49 pagesAccount Receivable ManagementAli Mubin FitranandaNo ratings yet

- Karina ReportDocument15 pagesKarina ReportKarina BalatbatNo ratings yet

- A Study On Receivables ManagementDocument3 pagesA Study On Receivables ManagementShameem AnwarNo ratings yet

- Unit 4 RM1Document18 pagesUnit 4 RM1vishal kumarNo ratings yet

- Receivables ManagementDocument30 pagesReceivables Managementjibinjohn140No ratings yet

- Chapter 28Document7 pagesChapter 28Mukul KadyanNo ratings yet

- Receivables ManagementDocument22 pagesReceivables Managementshayan.53260No ratings yet

- Receivables ManagementDocument37 pagesReceivables ManagementGaurav SharmaNo ratings yet

- Credit Collection Policy Procedures and PracticesDocument28 pagesCredit Collection Policy Procedures and Practicescheska.movestorageNo ratings yet

- Unit Vi: Receivables ManagementDocument18 pagesUnit Vi: Receivables ManagementDevyansh GuptaNo ratings yet

- Unit-5 Receivables ManagementDocument26 pagesUnit-5 Receivables ManagementSarthak MattaNo ratings yet

- Corporate FinanceDocument20 pagesCorporate FinanceMrs. Seema NazneenNo ratings yet

- Receivables ManagementDocument8 pagesReceivables Managementramteja_hbs14No ratings yet

- Receivables Management: Dr.K.P.Malathi ShiriDocument19 pagesReceivables Management: Dr.K.P.Malathi ShiriSruthy KrishnaNo ratings yet

- The Advantages & Disadvantages of Economic Order Quantity (EOQ)Document10 pagesThe Advantages & Disadvantages of Economic Order Quantity (EOQ)Don Baraka DanielNo ratings yet

- Receivable ManagementDocument14 pagesReceivable Managementbharath_skumar0% (1)

- Sai Kiran Print PDFDocument53 pagesSai Kiran Print PDFThanuja BhaskarNo ratings yet

- Unit 4 Receivables - ManagementDocument27 pagesUnit 4 Receivables - ManagementrehaarocksNo ratings yet

- Working Capital ManagementDocument14 pagesWorking Capital ManagementJoshua Naragdag ColladoNo ratings yet

- Account Receivable Management OverviewDocument21 pagesAccount Receivable Management OverviewLlyod Daniel Paulo0% (1)

- Receivables ManagementDocument18 pagesReceivables Managementnancy bhatiaNo ratings yet

- Unit 4 Reveivables ManagementDocument43 pagesUnit 4 Reveivables Managementvishal kumarNo ratings yet

- Receivables Management & FactoringDocument20 pagesReceivables Management & FactoringYusuf TakliwalaNo ratings yet

- Receivable Manage, EntDocument12 pagesReceivable Manage, Entajay.gole2325pNo ratings yet

- The Objectives of Accounts Receivable ManagementDocument14 pagesThe Objectives of Accounts Receivable ManagementAjay Kumar TakiarNo ratings yet

- Receivables ManagementDocument16 pagesReceivables ManagementDushyant SinhaNo ratings yet

- Development of Credit and Collection Policy PDFDocument35 pagesDevelopment of Credit and Collection Policy PDFJimuel Faigao100% (1)

- FM5.2 Receivable ManagementDocument15 pagesFM5.2 Receivable ManagementAbdulraqeeb AlareqiNo ratings yet

- Working Capital Management: Learning OutcomesDocument5 pagesWorking Capital Management: Learning Outcomesmanique_abeyratneNo ratings yet

- Receivables Management: Prepared by The FacultyDocument12 pagesReceivables Management: Prepared by The FacultyNoman SulemanNo ratings yet

- Receivabbles Management An OverviewDocument10 pagesReceivabbles Management An OverviewHonika PareekNo ratings yet

- Receivables ManagementDocument27 pagesReceivables Managementbhav08No ratings yet

- TOPIC 9 Chapter 19 Accounts Receivable and Inventory ManagementDocument17 pagesTOPIC 9 Chapter 19 Accounts Receivable and Inventory ManagementIrene Kim100% (1)

- I M Pandey Financial Management Chapter 28Document3 pagesI M Pandey Financial Management Chapter 28Rushabh VoraNo ratings yet

- Minimalist Business Report-WPS OfficeDocument21 pagesMinimalist Business Report-WPS Officewilhelmina romanNo ratings yet

- FGFGFGDocument16 pagesFGFGFGarjunroy15No ratings yet

- CH - 4 Receivable ManagementDocument11 pagesCH - 4 Receivable Managementsabage1723No ratings yet

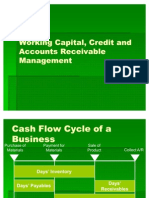

- Working Capital, Credit and Accounts Receivable ManagementDocument31 pagesWorking Capital, Credit and Accounts Receivable ManagementAnkit AgarwalNo ratings yet

- Strategies For Effective CollectionsDocument9 pagesStrategies For Effective CollectionszakiahmokhniNo ratings yet

- Accounts Receivable ManagementDocument21 pagesAccounts Receivable ManagementNeris SaturdayNo ratings yet

- (FM) HSBMS (F) - FM ProjectDocument13 pages(FM) HSBMS (F) - FM ProjectSiddh JainNo ratings yet

- Receivables and Payables ManagementDocument16 pagesReceivables and Payables ManagementDony ZachariasNo ratings yet

- Handout. WCM - Receivable ManagementDocument16 pagesHandout. WCM - Receivable ManagementNaia SNo ratings yet

- Receivables ManagementDocument12 pagesReceivables Managementinaya7568No ratings yet

- Receivables Management: Presented by Group 10Document10 pagesReceivables Management: Presented by Group 10Anonymous GuyNo ratings yet

- Unlocking Financial Opportunities: A Comprehensive Guide on How to Establish Business CreditFrom EverandUnlocking Financial Opportunities: A Comprehensive Guide on How to Establish Business CreditNo ratings yet

- Seven Tips For Surviving R: John Mount Win Vector LLC Bay Area R Users Meetup October 13, 2009 Based OnDocument15 pagesSeven Tips For Surviving R: John Mount Win Vector LLC Bay Area R Users Meetup October 13, 2009 Based OnMarco A SuqorNo ratings yet

- Making Tomorrow's Workforce Fit For The Future of Industry: Siemens Mechatronic Systems Certification Program (SMSCP)Document6 pagesMaking Tomorrow's Workforce Fit For The Future of Industry: Siemens Mechatronic Systems Certification Program (SMSCP)Shobanraj LetchumananNo ratings yet

- ABC - Suggested Answer - 0Document8 pagesABC - Suggested Answer - 0pam pamNo ratings yet

- Research Methods For Commerce Lab Practical File "BRM Lab" BBA (M1) - BBA 213Document67 pagesResearch Methods For Commerce Lab Practical File "BRM Lab" BBA (M1) - BBA 213Mankeerat Singh ChannaNo ratings yet

- Manual de Instalación - Tableros Centro de Carga - Marca GEDocument4 pagesManual de Instalación - Tableros Centro de Carga - Marca GEmariana0% (1)

- Amstar StaffingDocument14 pagesAmstar StaffingSunil SNo ratings yet

- Organic Solvent Solubility DataBookDocument130 pagesOrganic Solvent Solubility DataBookXimena RuizNo ratings yet

- Heat, Temperature, and Heat Transfer: Cornell Doodle Notes FREE SAMPLERDocument13 pagesHeat, Temperature, and Heat Transfer: Cornell Doodle Notes FREE SAMPLERShraddha PatelNo ratings yet

- Ulangan Harian Exposition TextDocument3 pagesUlangan Harian Exposition Textgrenninja949No ratings yet

- Group 1 Intro To TechnopreneurshipDocument22 pagesGroup 1 Intro To TechnopreneurshipMarshall james G. RamirezNo ratings yet

- Manual FSP150 GE114PRO FAM PDFDocument80 pagesManual FSP150 GE114PRO FAM PDFJanet Sabado CelzoNo ratings yet

- Essay Outline - Flaws in Our Education System Are Causing Some of Our Failures PDFDocument3 pagesEssay Outline - Flaws in Our Education System Are Causing Some of Our Failures PDFToufiq IbrahimNo ratings yet

- Specification - MechanicalDocument5 pagesSpecification - MechanicalEDEN FALCONINo ratings yet

- University of Michigan Dissertation ArchiveDocument6 pagesUniversity of Michigan Dissertation ArchiveBuyResumePaperUK100% (1)

- Kullie StrainGageManualDigitalDocument67 pagesKullie StrainGageManualDigitalDizzixxNo ratings yet

- Sample Pages: Pearson AustraliaDocument5 pagesSample Pages: Pearson AustraliaMin ZekNo ratings yet

- Answer To In-Class Problem-RijkdomDocument2 pagesAnswer To In-Class Problem-RijkdomnigusNo ratings yet

- Classroom Management and Student Motivation: Clare Heaney: Director of StudiesDocument28 pagesClassroom Management and Student Motivation: Clare Heaney: Director of StudiesRyan BantidingNo ratings yet

- 0810 Operation Manual250708Document117 pages0810 Operation Manual250708isaacaiyacNo ratings yet

- Automation of Nestle ProductsDocument41 pagesAutomation of Nestle ProductsRamesh KumarNo ratings yet

- American Heart Association PPT - AIHA Webinar - FinalDocument49 pagesAmerican Heart Association PPT - AIHA Webinar - FinalVina WineNo ratings yet

- N67 TM1X: 1/ GeneralDocument3 pagesN67 TM1X: 1/ General林哲弘No ratings yet

- SSC Gr10 ICT Q4 Module 2 WK 2 - v.01-CC-released-7June2021Document16 pagesSSC Gr10 ICT Q4 Module 2 WK 2 - v.01-CC-released-7June2021Vj AleserNo ratings yet

- Setting The Standard: For Electronic Theodolites WorldwideDocument2 pagesSetting The Standard: For Electronic Theodolites WorldwidePepenkNo ratings yet

- Classification of Common Musical InstrumentsDocument3 pagesClassification of Common Musical InstrumentsFabian FebianoNo ratings yet

- Et Annual Report 04 05Document48 pagesEt Annual Report 04 05Pavlo Andre AbiyNo ratings yet

- BeachesDocument32 pagesBeachesnympheasandhuNo ratings yet

- Tiger Grey Card CopyrightDocument2 pagesTiger Grey Card Copyrightsabo6181No ratings yet

- SSP Assignment Problems - FinalDocument2 pagesSSP Assignment Problems - FinalVadivelan AdaikkappanNo ratings yet

- Type X - Cityzen Park North - 291123-1Document3 pagesType X - Cityzen Park North - 291123-1Oky Arnol SunjayaNo ratings yet